ACCT20100 Chapter Notes - Chapter 8: Income Statement

Document Summary

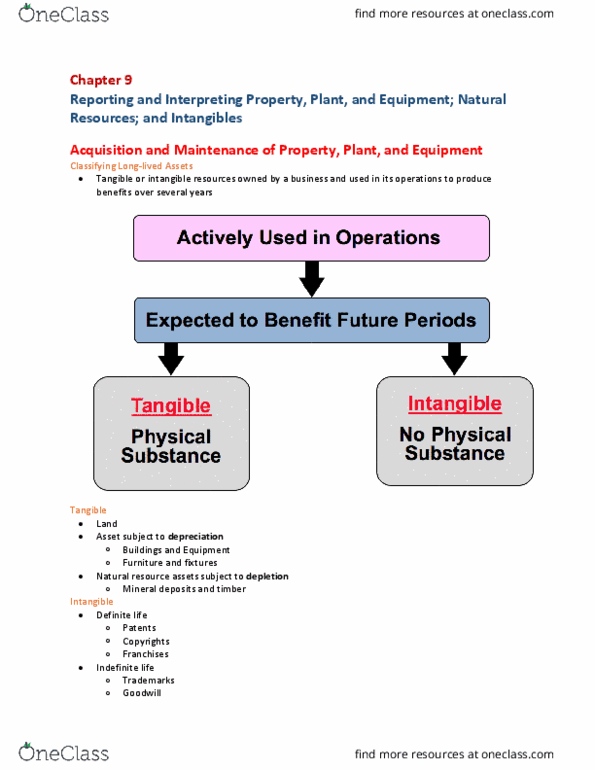

Chapter 8: reporting and interpreting property, plant, and equipment; intangibles; and natural resources. How managers choose which method to use: financial reporting: which method gives the best matching of revenues and expenses for a given asset. Use straight-line if asset is expected to provide benefits evenly over time. Also (cid:396)epo(cid:396)ts highe(cid:396) i(cid:374)(cid:272)o(cid:373)es du(cid:396)i(cid:374)g asset"s ea(cid:396)ly yea(cid:396)s. Use accelerated method if asset produces more revenue in early years: tax reporting: Impairment: if a(cid:374) asset"s value decreases and cannot be recovered through future use or sale. The loss of a significant portion of utility of an asset through: La(cid:272)k of de(cid:373)a(cid:374)d fo(cid:396) the asset"s se(cid:396)(cid:448)i(cid:272)es. Recognize a loss when an asset suffers a permanent impairment: test for impairment: Impairment loss= net book value fair value. Asset is written down to fair value. Disposal of property, plant, and equipment: disposing of an asset: