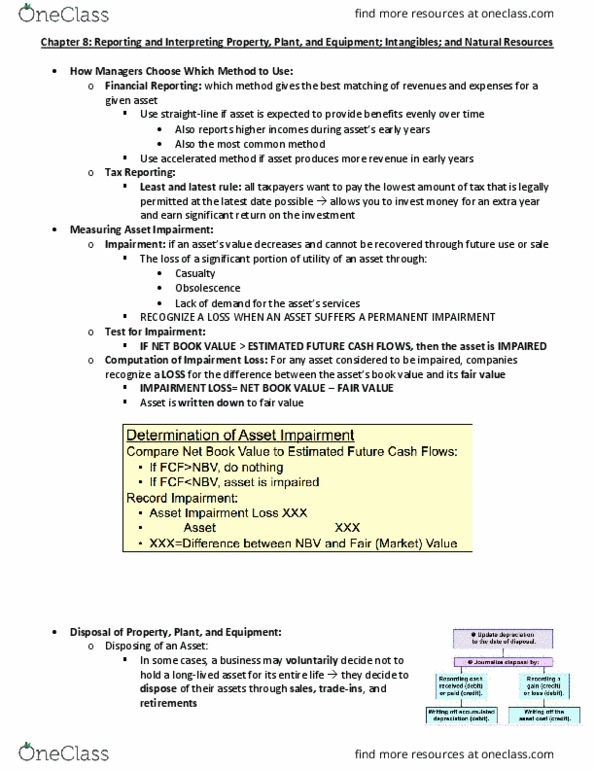

Accounting ACCT 2610 Lecture Notes - Lecture 8: Web Development, Intangible Asset, Spose

Document Summary

Get access

Related Documents

Related Questions

| . Make all 16 adjustments to journal entries. Remember to include a description under each journal entry. |

| 1 | On March 1, ABC purchased a one-year liability insurance policy for $98,400. | ||||||||

| Upon purchase, the following journal entry was made: | |||||||||

| Dr Prepaid insurance | 98,400 | ||||||||

| Cr Cash | 98,400 | ||||||||

| The expired portion of insurance must be recorded as of 12/31/14. | |||||||||

| Notice that the expired portion from March through November has been recorded already. | |||||||||

| Make sure that the Prepaid Insurance balance after the adjusting entry is correct. | |||||||||

| 2 | Depreciation expense must be recorded for the month of December. | ||||||||

| The building was purchased with cash on February 1, 2014, for $150,000 with a remaining useful life of 30 years and a salvage value of $6,000. | |||||||||

| The method of depreciation for the building is straight-line. | |||||||||

| The equipment was purchased with cash on February 1, 2014, for $60,000 with a remaining useful life of 5 years and a salvage value of $3,000. | |||||||||

| The method of depreciation for the equipment is double-declining balance. | |||||||||

| Depreciation has been recorded for the building and equipment for months February through November. | |||||||||

| 3 | On December 1, XYZ Co. agreed to rent space in ABC's building for $12,000 per month, | ||||||||

| and XYZ paid ABC on December 1 in advance for the first three months' rent. | |||||||||

| The entry made on December 1 was as follows: | |||||||||

| Dr Cash | 36,000 | ||||||||

| Cr Unearned rent revenue | 36,000 | ||||||||

| The unearned revenue account must be adjusted to reflect the amount earned as of 12/31/14. | |||||||||

| 4 | Per timecards, from the last payroll date through December 31, 2014, ABC's employees have worked a total of 250 hours. | ||||||||

| Including payroll taxes, ABC's wage expense averages about $51 per hour. The next payroll date is January 5, 2015. | |||||||||

| The liability for wages payable must be recorded as of 12/31/14. | |||||||||

| 5 | On November 30, 2014, ABC borrowed $235,000 from American National Bank by issuing an interest-bearing note payable. | ||||||||

| This loan is to be repaid in three months (on February 28, 2015), along with interest computed at an annual rate of 6%. | |||||||||

| The entry made on November 30 to record the borrowing was: (for Statement of Cash Flow purposes, consider a financing item) | |||||||||

| Dr Cash | 235,000 | ||||||||

| Cr Notes payable | 235,000 | ||||||||

| On February 28, 2015 ABC must pay the bank the amount borrowed plus interest. | |||||||||

| Assume the beginning balance for Notes Payable is correct. | |||||||||

| Interest through 12/31/14 must be accrued on the $235,000 note. | |||||||||

| 6 | ABC uses a periodic inventory system, and the ending inventory for each year is determined by taking a complete | ||||||||

| physical inventory at year-end. A physical count was taken on December 31, 2014, and the inventory on-hand at | |||||||||

| that time totaled $75,000, which reflects historical cost. | |||||||||

| Record the 2014 Cost of Goods Sold and the 12/31/14 Inventory adjustment. | |||||||||

| Additionally, ABC adheres to GAAP by recording ending inventory at the lower of cost and net realizable value at a total inventory level. | |||||||||

| A review of inventory data further indicated that the current retail sales value of the ending inventory is $110,000 and estimated costs of | |||||||||

| completion and shipping is 15% of retail. Be sure to make an additional adjustment, if necessary, to properly value ending inventory | |||||||||

| using the Loss and Allowance methodology. For Income Statement presentation purposes, be sure to use the Loss Method for accounting | |||||||||

| for adjustments of inventory to market value. | |||||||||

| 7 | It would be unusual for a company to have an asset impairment in Year 1, but for the sake of this example, ABC realized | ||||||||

| that their intangible asset might be impaired on December 31, 2014. Record the impairment if any. | |||||||||

| The expected future net cash flows for this intangible asset totals $30,000, and the fair value of the asset is $27,500. | |||||||||

| 8 | On 7/1/14, ABC purchased 7,000 shares of its own stock from existing stockholders as treasury stock. The cost of the treasury | ||||||||

| stock was $7 per share, or $49,000 in total. The effects of this transaction are already shown in the unadjusted trial balance. On 12/31/14, | |||||||||

| ABC reissued these 7,000 shares of treasury stock at $10 per share. Record the journal entry required for the reissuance of the treasury stock. | |||||||||

| 9 | On 12/31/14, ABC issued 5,000 shares of $3 par value common stock at the closing market price of $7 per share. Prepare ABC's journal entry | ||||||||

| to reflect the issuance of the stock on 12/31/14. | |||||||||

| 10 | On 7/1/14, ABC sold 12% bonds having a maturity value of $800,000 for $861,771, resulting in an effective yield of 10%. The bonds are | ||||||||

| dated 7/1/14, and mature 7/1/19. Interest is payable semiannually on July 1 and January 1. ABC uses the effective interest method of | |||||||||

| amortization for bond premium or discount. Record the adjusting entry for the accrual of interest and the related amortization on 12/31/14. | |||||||||

| Hint: Develop an abbreviated amortization schedule to accurately determine the interest expense. | |||||||||

| 11 | The following information is available for ABC Corporation at 12/31/14 regarding its investments in stocks of other companies. | ||||||||

| Securities | Cost | Fair Value | |||||||

| 2,200 shares of Toyota Corporation Common Stock | $ 100,000 | $ 125,000 | |||||||

| 1,100 shares of G.M. Corporation Common Stock | $ 67,000 | $ 34,000 | |||||||

| $ 167,000 | $ 159,000 | ||||||||

| Prepare the adjusting entry (if any) for 2014, assuming the securities are classified as trading. | |||||||||

| 12 | On 1/1/14, ABC Corporation purchased, as a held-to-maturity investment, $200,000 of the 8%, 5-year bonds of Intuit Corporation for $177,824, | ||||||||

| which provides an 11% return. Prepare ABC's 12/31/14 journal entry to reflect the receipt of annual interest and discount amortization. | |||||||||

| Assume the bond investment pays interest annually on 12/31 each year and that effective interest amortization is used. | |||||||||

| Note: Notice that a discount account is not used for this investment. Therefore, for purposes of this adjusting entry, amortize the discount directly to the | |||||||||

| investment account. | |||||||||

| 13 | ABC Corporation prepares an aging schedule on 12/31/14 that estimates total uncollectible accounts at $25,000. Assuming that the allowance method is used, | ||||||||

| prepare the entry to record bad debt expense. | |||||||||

| 14 | On 1/1/14, ABC Corporation signed a 5-year noncancelable lease for a delivery vehicle. The terms of the lease called for ABC to Corporation to make | ||||||||

| annual payments of $10,503 at the beginning of each year, starting January 1, 2014. The delivery vehicle has an estimated useful life of 6 years and a $7,000 | |||||||||

| unguaranteed residual value. The delivery vehicle reverts back to the lessor at the end of the lease term. ABC Corporation uses the straight-line method | |||||||||

| of depreciation for the delivery vehicle. ABC Corporation's incremental borrowing rate is 10%, and the Lessor's implicit rate is unknown. No entries have yet | |||||||||

| been made concerning this lease arrangement. After determining the type of lease arrangement (capital or operating), prepare the necessary multiple-part journal | |||||||||

| entry for 2014 for ABC Corporation. (Hints: You will need to compute the present value of the minimum lease payments and 4 separate sub-entries for | |||||||||

| this lease transaction. Also, for Statement of Cash Flow purposes, the principal portion of lease payments are correctly categorized as a financing activity.) | |||||||||

| 15 | ABC Corporation provides a defined benefit pension plan for its employees. A combination adjusting entry should be made to correctly account for this type of pension | ||||||||

| plan given the following items of information for the 2014 plan year, including the recording of pension expense and the employer's contribution to the pension plan in 2014. | |||||||||

| Note: Use the summary entry method as demonstrated and discussed in the chapter lectures on pension accounting to prepare the adjusting entry. | |||||||||

| Pension asset/liability (January 1) | $0 | ||||||||

| Actual return on plan assets | $40,000 | ||||||||

| Expected return on plan assets | $20,000 | ||||||||

| Contributions (funding) in 2014 | $37,000 | ||||||||

| Fair value of plan assets (December 31) | $75,000 | ||||||||

| Settlement rate | 10% | ||||||||

| Projected benefit obligation (January 1) | $0 | ||||||||

| Service cost | $60,000 | ||||||||

| Benefits paid in 2014 | $0 | ||||||||

| *For purposes of financial statement presentation, consider Pension Expense as an operating item and any resulting Pension Asset/Liability as long-term in nature. | |||||||||

| 16 | On December 31, 2014, ABC Corporation issued 1,000 shares of restricted stock to its Chief Financial Officer. ABC stock had a fair value (closing market price) of | ||||||||

| $10 per share on December 31, 2014. Additional information is as follows: | |||||||||

| a. The service period related to the restricted stock is 2 years. | |||||||||

| b. Vesting occurs if the CFO stays with the company for a two-year period. | |||||||||

| c. The par value of the common stock is $3 per share. | |||||||||

| Make the appropriate accounting entry as of the grant date, 12/31/14. Note: use the alternative method as described in your textbook for deferred compensation. | |||||||||

| Do this step after preparing the Income Statement except for the Income taxes line: (You need to calculate Income Before Income Taxes in order to calcualte total Income Tax Expense) | |||||||||

| 17 | Corporate taxes are due in four estimated quarterly payments on April 15, June 15, September 15, and December 15. | ||||||||

| However, for the purposes of this ABC illustration, we will assume that estimates are not paid, and that the tax is paid in full | |||||||||

| on the return's March 15, 2015 due date. | |||||||||

| ABC's income tax rate is 40%. The entire year's income tax expense was estimated at the beginning of 2014 to be $69,600, | |||||||||

| so January through November income tax expense recognized amounts to $63,800 (11/12 months). | |||||||||

| Since we are assuming estimates are not made during the year, the balance in Income taxes payable represents | |||||||||

| tax accrued for January through November. Assume no deferred tax assets or deferred tax liabilities. | |||||||||

| Based on the income before income taxes figure from the income statement, record December's income tax expense | |||||||||

| so that the entire year's total tax expense is correct. | |||||||||

Professional judgmentframework

Property, Plant and Equipment: Impairment

Background

Toyda, Inc. (Toyda) is one of the worldâs leading carmanufacturers. They sell cars exclusively in the US. In recentyears, Toyda has begun producing electric cars, as well asspecialized equipment that is used to charge electric cars.Management of Toyda had been very optimistic about this recentventure. For internal purposes, Toyda projected a growth rate of40% for the electric car production and for the production of thespecialized equipment. Management believes that these estimateswere conservative. Currently, Toyda is the only carmaker in the USthat is producing electric cars.

In December 2012, a number of oil reserves were discovered inAlaska. These oil reserves are much more significant than anyreserves that currently exist. Consumers in the US are euphoricover these discoveries. Accordingly, many automobile manufacturingcompanies and industry and government analysts believe that thedemand for electric cars will decrease substantially.

While the CEO is exceedingly worried about this new turn ofevents, she is not really worried about the financial statementsfor the December 31, 2012 year-end. Because Toyda is still in theearly stages of producing and selling electric cars, most of thecompanyâs current net income is attributable to traditional cars.The current consensus analyst forecast for net income per share is$10.25, which equates to $30.0 million ofnet income. Although Toyda has not yet finalized theirfinancial statements for 2012, the draft income statement providedto the CEO on February 1, 2013, showed net income of $35million, an effective tax rate of 20% and total assets of $500.0million. Toyda is audited annually.

The CFO at Toyda has been consulting with external valuationspecialists since early December to determine if there is a need toimpair one or both production facilities. Toyda is notconsidering a potential sale or an alternative use of itsproduction facilities. The valuation specialists have extensiveexperience with the global automotive industry, including theelectronic car industry in Europe. The valuation specialists issuedtheir report on February 3, 2013. The report included an analysisof expected growth rates based on available market data, industrytrends, historical results and other pertinent data. The reportindicated that Toyda will be able to maintain their expected growthrates for two more years, until the newly discovered oil reservesare ready to begin production. Beginning in 2015, they would expectgrowth rates between 15% and 19% for the specialized equipmentfacility and the car production facility. They anticipate thatToyda will be able to dispose of the production facility forelectric cars in 20 years, with proceeds of $500,000. Likewise, theproduction facility for the specialized equipment could be disposedof in 10 years with proceeds of $10,000. The valuation specialistsalso believe that the highest and best use of the facility is itscurrent use and an expected present value technique (i.e., expectedcash flows) would be the most appropriate method to make a fairvalue determination. The CFO has been heavy involved in thepreparation and review of the valuation specialistsâ report and shebelieves it is a balanced and fair assessment.

The table below provides data on the two facilities.

Asset group: production facilities | Carrying value December 31, 2012 | Remaining life in years | Actual data | |||||

Operating cash flows | Operating income | |||||||

2010 | 2011 | 2012 | 2010 | 2011 | 2012 | |||

Electric cars | $25,000,000 | 20 | $45,000 | $77,000 | $98,000 | $32,000 | $43,000 | $57,000 |

Electric car chargers | $4,000,000 | 10 | $5,000 | $19,000 | $25,000 | ($8,000) | ($15,000) | ($12,000) |

The following table provides the annual yield on the risk-freerate expected over the next 20 years obtained from the U.S.Department of the Treasury. The CFO has engaged in discussions withinvestment bankers to determine what the appropriate risk premiumwould be for these facilities (analyzed and supported based onmarket data available for comparable companies). Based on thesediscussions, she believes that a risk premium of 8% to 12% shouldbe added to the risk-free rate to reflect a current discountrate.

Year | Yield* |

1 | 0.12% |

2 | 0.27% |

3 | 0.40% |

4 | 0.62% |

5 | 0.89% |

6 | 1.12% |

7 | 1.41% |

8 | 1.67% |

9 | 1.81% |

10 | 1.97% |

11 | 2.05% |

12 | 2.11% |

13 | 2.25% |

14 | 2.32% |

15 | 2.45% |

16 | 2.50% |

17 | 2.59% |

18 | 2.62% |

19 | 2.65% |

20 | 2.67% |

*This represents the annual yield to maturity for each timeperiod. Thus, for example, an investment held for 10 years wouldyield a 1.97% return per year.

As the junior accountant, the CFO has asked you to provide heran analysis of the need for an impairment of the productionfacilities and the amount of impairment loss to be recorded, ifany.

Required

⺠Reference the professional judgmentframework handout and application template separately provided.

⺠For December 31, 2012, using your judgment,perform an analysis of the need for an impairment of the productionfacilities and the amount of impairment loss to be recorded, ifany. Using the professional judgment framework, complete theapplication template for all process steps and provide theappropriate information in the documentation column.

â In performing youranalysis, you should use an Excel spreadsheet to support anycalculations.

⺠Using the information you documentedregarding the overarching considerations and the specificconsiderations for each process step in the framework, prepare amemorandum that you will provide to the CFO (not to exceed threepages). Be sure to include specific references to the applicableguidance and quote the applicable guidance. Also attach your excelspread sheet with your calculations. Upon completing yourdocumentation, make certain that you are able to answer thefollowing considerations:

â Is the documentationsufficient to support your judgment?

â Can another professionalunderstand how you reached your conclusion (including whyreasonable outcomes and possible alternatives identified were notselected)?