BU127 Chapter Notes - Chapter 5: National Beverage, Book Value, Inventory Turnover

6

BU127 Full Course Notes

Verified Note

6 documents

Document Summary

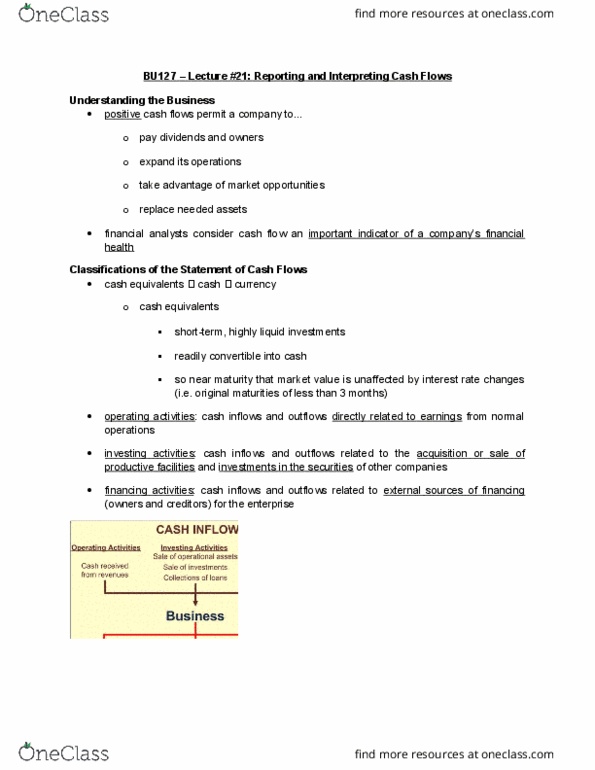

Bu127 chapter 5: reporting and interpreting cash flows. Cash equivalent: short-term, highly liquid investment with an original maturity of less than 3 months. Readily convertible to known amounts of cash. So near their maturity that there is little risk that their value will change if interest rates change. E. g. treasury bills (form of short-term gov. debt), money market funds, commercial paper (short-term notes payable issued by large corporations) Statement of cash flows reports cash inflows and outflows based on 3 categories: operating activities. Cash flows from operating activities: cash inflows and outflows directly related to earnings from normal operations. Not affected by accruals, deferrals, and allocations that result from timing of revenue and expense recognition. Direct method: reports components of cash flows from operating activities as gross receipts and gross payments. Net cash inflow (outflow) from operating activities: difference between inflows and outflows. Direct method is more expensive to implement than indirect.