BU127 Lecture Notes - Lecture 21: Common Rule, Capital Structure, Cash Flow Statement

6

BU127 Full Course Notes

Verified Note

6 documents

Document Summary

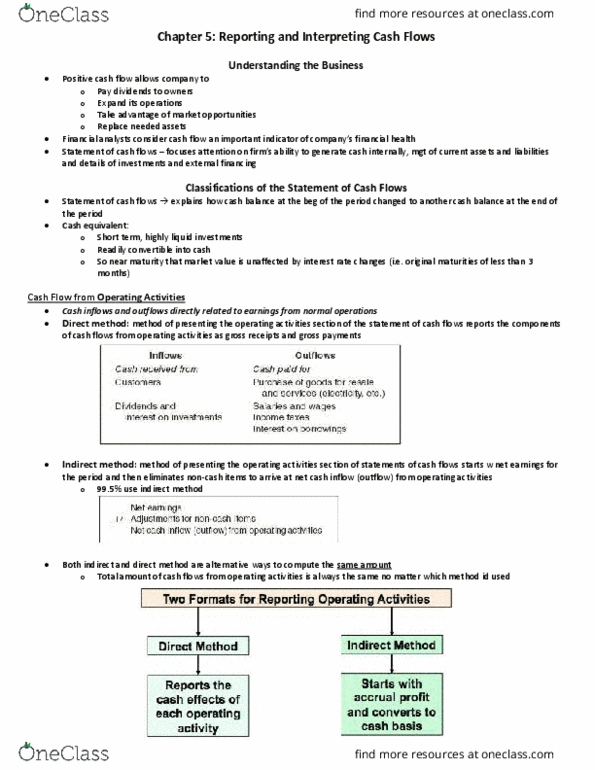

Bu127 lecture #21: reporting and interpreting cash flows. Understanding the business positive cash flows permit a company to : pay dividends and owners, expand its operations, take advantage of market opportunities, replace needed assets financial analysts consider cash flow an important indicator of a company"s financial health. 2. indirect method: starts with accrual profit and converts to cash basis note that no matter which format is used, the same amount of net cash flows from operating activities is generated. Cash flows from investing activities inflows cash received from: sale or disposal of property, plant, and equipment, sale or maturity of investments in securities outflows cash paid for, purchase of property, plant, and equipment, purchase of investments in securities. Relationships to the statement of financial position and the statement of earnings. Cash flows from operating activities indirect method (slides 16-17 are very important) + non-cash expenses such as depreciation and amortization cash flows from operating activities (indirect method)