ACCT I S 211 Study Guide - Midterm Guide: Coq, Southwest Airlines, Finished Good

13 Oct 2016

School

Department

Course

Professor

Document Summary

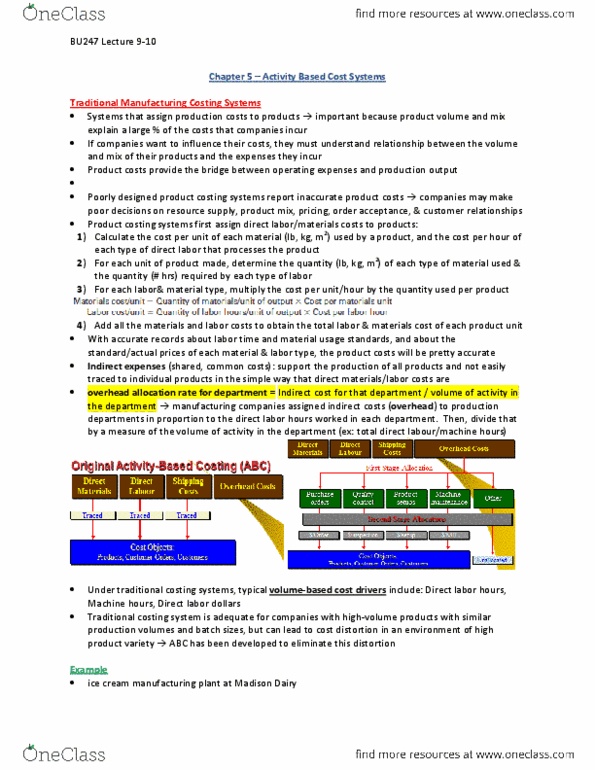

Assignment of indirect costs based only on (cid:498)unit-level(cid:499) or unit volume drivers: may have multiple overhead rate based on different cost drivers, but the cost drivers will typically be unit-level. Ex: direct labor hours, direct labor cost, machine hours, direct. Because of this focus on unit volume drivers, traditional cost systems often: underestimate the cost of resources required for specialty, low volume products, overestimate the cost of resources for high volume, standard products. These have been developed to eliminate cost distortions. Activity-based cost (abc) assigns resource expenses to activities on the basis of how much of the resource each activity uses. Especially useful when: large cost pool- manufacturing support, customer support, etc, diversity- diversity of resource usage by products, services or customers. Unit related: proportional to number of units produced: direct labor hours, machine hours. Batch related: not unit related, related to number of batches run: machine setups, 1st item inspection.