ACCT 2301 Study Guide - Final Guide: Net Present Value, Outsourcing, Contribution Margin

Document Summary

Get access

Related Documents

Related Questions

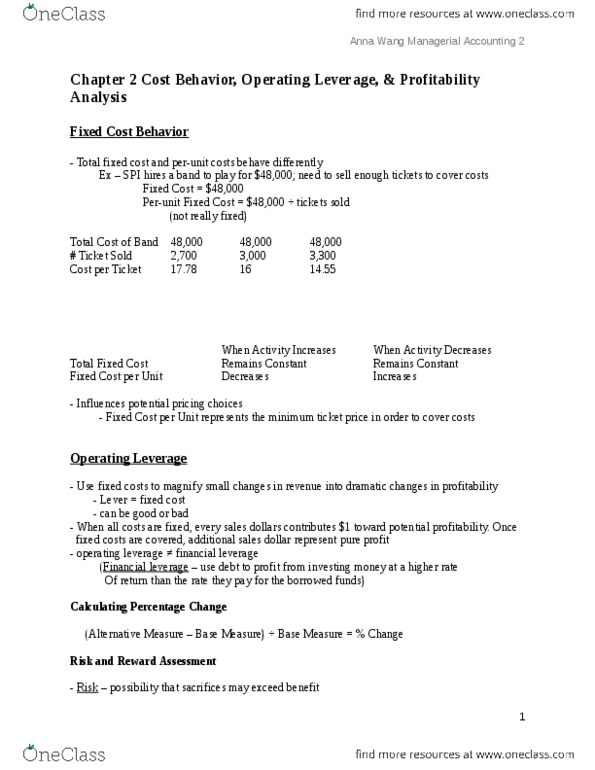

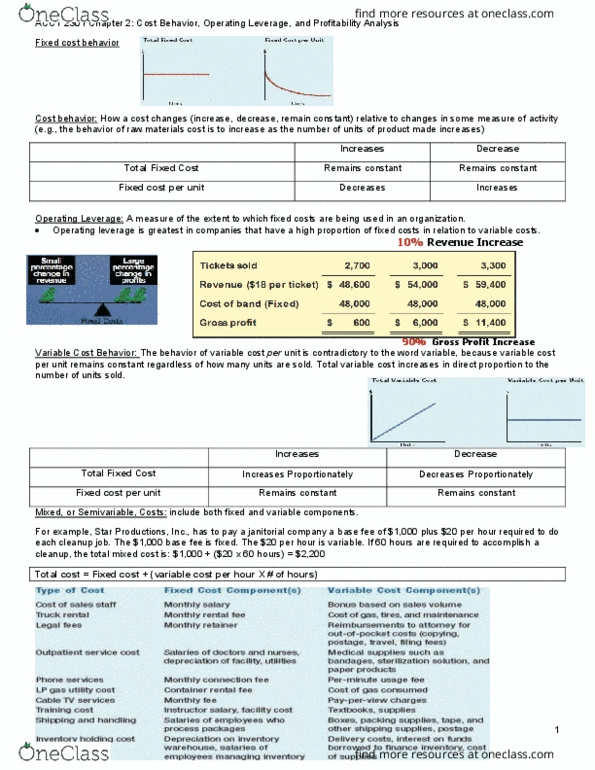

BW Manufacturing Company produced gas grills in three primarymodels (Grills A, B, and C). BW was a small player in the industry,but business had been good, and it was expecting another profitableyear. Draft of the companyâs operating budget is shown in Exhibit1. Stand costs for the three products are explained in Exhibit 3.Selling, general, and administrative (SG&A), other costs,interest income, and interest expense were likely to remain thesame no matter which product-line combinations the companyproduced.

Before calling it a day, the two owners asked their assistant,Justine Richardson, to determine the impact of several options onincome before tax. They agreed to meet the following day, andRichardson hurried off to look at what these latest ideas wouldmean. She had four questions to address and was asked to considereach option independent of all other options.

BW Manufacturing Company

1.Calculate the impact of dropping Grill A. Assume no otherchanges to the plan.

Should BW drop Grill A? The owners wanted to know the impact ofdropping Grill A from their line of products. Richardson was toldto assume that the volumes and selling prices of the other twoproducts would be the same whether or not the Grill A product linewas dropped.

Your response:

2.Calculate the impact of reducing Grill C price to $75, withthe expectation that the volume of that product will increase to220,000 units. Assume no other changes to the plan.

Your response:

3. Calculate the impact of a 10,000 unit decrease in Grill A and10,000 unit increase in Grill C volume due to the change in theadvertising focus. Assume no other changes to the plan.

Should BW change its advertising focus?

Your response:

4. Calculate the impact of a $5 decrease in Grill Câs price anda change in advertising focus leading to a 10,000 unit decrease inGrill Aâs volume and a 30,000 unit increase in Grill Câs volume.Assume no other changes to the plan.

Should BW lower the price of Grill C and change its advertisingfocus?

Your response:

| Table 1. Actual2009 volumes | |||||||||

| Grill | Volume (# in units) | ||||||||

| A | 115,000 | ||||||||

| B | 110,000 | ||||||||

| C | 225,000 | ||||||||

| Richardson began to wonder ifthe bottom line was as high as it should have been | |||||||||

| Exhibit 1 | |||||||||

| BW Manufacturing Company | |||||||||

| Operating Budget 2009: Draft12/18/2008 | |||||||||

| Sales | $41,200,000 | ||||||||

| Less: costs of products sold | $22,800,000 | ||||||||

| Gross margin | $18,400,000 | ||||||||

| SG&A | $9,350,000 | ||||||||

| Other costs | $2,100,000 | ||||||||

| Operating income | $6,950,000 | ||||||||

| Less: Interest expense | $420,000 | ||||||||

| Plus: Interest income | $150,000 | ||||||||

| Income before tax | $6,680,000 | ||||||||

| Income taxes | $2,338,000 | ||||||||

| Net income | $4,342,000 | ||||||||

| Exhibit 2 | |||||||||

| Standard Costs | |||||||||

| Grill A | Grill B | Grill C | |||||||

| Planned Volume (units) | 80,000 | 120,000 | 200,000 | ||||||

| Per Unit: | |||||||||

| Sales price | $150 | $110 | $80 | ||||||

| Direct Costs: | |||||||||

| Materials | 17 | 10 | 7 | directly related to production volume | |||||

| Labor | 21 | 16 | 4 | directly related to production volume | |||||

| Subtotal | $38 | $26 | $11 | ||||||

| Indirect costs: | |||||||||

| Supplies | 7 | 2 | 1 | directly related to production volume | |||||

| Labor | 10 | 8 | 4 | one-half varies with direct labor; the rest isfixed | |||||

| Supervision | 8 | 3 | 1 | unrelated to production volume | |||||

| Energy | 12 | 6 | 4 | one-half varies with direct labor; the rest isfixed | |||||

| Depreciation | 22 | 7 | 5 | unrelated to production volume | |||||

| Head office support | 12 | 6 | 3 | corporate office allocation* | |||||

| All other | 11 | 2 | 1 | unrelated to production volume | |||||

| Subtotal | $82 | $34 | $19 | ||||||

| Total product cost | $120 | $60 | $30 | ||||||

| Product-line profitability | $30 | $50 | $50 | ||||||

| *This category comprisesaccounting, IT, human resources, legal, and other supporting theproduction of these products. | |||||||||

| Allocations were made usingmultiple drivers. Corporate office budgets are unrelated toproduction levels. | |||||||||

| Exhibit 3 | |||||||||

| 2009 Operating Results: Draft1/19/2010 | |||||||||

| Revenue | $46,225,000 | ||||||||

| Variable costs: | |||||||||

| Materials | 4,800,000 | ||||||||

| Direct labor | 5,200,000 | ||||||||

| Supplies | 1,300,000 | ||||||||

| Indirect labor | 1,500,000 | ||||||||

| Energy | 1,600,000 | ||||||||

| Total variable cost | $14,400,000 | ||||||||

| Fixed costs: | |||||||||

| Indirect labor | 1,300,000 | ||||||||

| Supervision | 1,200,000 | ||||||||

| Energy | 1,350,000 | ||||||||

| Depreciation | 3,660,000 | ||||||||

| Head office | 2,300,000 | ||||||||

| All other | 1,380,000 | ||||||||

| Total fixed cost | $11,190,000 | ||||||||

| Total cost | $25,590,000 | ||||||||

| Gross margin | $20,635,000 | ||||||||

| SG&A | 9,350,000 | ||||||||

| Other costs | 2,100,000 | ||||||||

| Operating income | $9,185,000 | ||||||||

| Less: interest expense | 420,000 | ||||||||

| Plus: interest income | 150,000 | ||||||||

| Income before tax | $8,915,000 | ||||||||

| Income taxes | $3,120,250 | ||||||||

| Net income | $5,794,750 | ||||||||

Hi, please help!!!

Pacific Rim Industries is a diversified company whose productsare marketed both domestically and internationally. The companyâsmajor product lines are furniture, sports equipment, and householdappliances. At a recent meeting of Pacific Rimâs board ofdirectors, there was a lengthy discussion on ways to improveoverall corporate profitability. The members of the board decidedthat they required additional financial information aboutindividual corporate operations in order to target areas forimprovement. |

Danielle Murphy, the controller,has been asked to provide additional data that would assist theboard in its investigation. Murphy believes that income statements,prepared along both product lines and geographic areas, wouldprovide the directors with the required insight into corporateoperations. Murphy had several discussions with the divisionmanagers for each product line and compiled the followinginformation from these meetings. |

| Product Lines | ||||||||||||

| Furniture | Sports | Appliances | Total | |||||||||

| Production and sales in units | 160,000 | 180,000 | 160,000 | 500,000 | ||||||||

| Average selling price per unit | $ | 9.00 | $ | 21.00 | $ | 14.00 | ||||||

| Average variable manufacturing cost per unit | 5.00 | 9.60 | 8.26 | |||||||||

| Average variable selling expense per unit | 2.00 | 2.20 | 2.25 | |||||||||

| Fixed manufacturing overhead, excluding depreciation | $ | 512,000 | ||||||||||

| Depreciation of plant and equipment | 412,000 | |||||||||||

| Administrative and selling expense | 1,190,000 | |||||||||||

| 1. | The division managers concluded that Murphy should allocatefixed manufacturing overhead to both product lines and geographicareas on the basis of the ratio of the variable costs expended tototal variable costs. |

| 2. | Each of the division managers agreed that a reasonable basis forthe allocation of depreciation on plant and equipment would be theratio of units produced per product line (or per geographical area)to the total number of units produced. |

| 3. | There was little agreement on the allocation of administrativeand selling expenses, so Murphy decided to allocate only thoseexpenses that were traceable directly to a segment. For example,manufacturing staff salaries would be allocated to product lines,and sales staff salaries would be allocated to geographic areas.Murphy used the following data for this allocation. |

| Manufacturing Staff | Sales Staff | ||||||

| Furniture | $ | 121,000 | United States | $ | 61,000 | ||

| Sports | 141,000 | Canada | 101,000 | ||||

| Appliances | 81,000 | Asia | 251,000 | ||||

| 4. | The division managers were able to provide reliable salespercentages for their product lines by geographical area. |

| Percentage of Unit Sales | ||||||

| United States | Canada | Asia | ||||

| Furniture | 30 | % | 20 | % | 50 | % |

| Sports | 30 | % | 30 | % | 40 | % |

| Appliances | 20 | % | 20 | % | 60 | % |

| Murphy preparedthe following product-line income statement based on the datapresented above. |

| PACIFIC RIM INDUSTRIES | |||||||||||||||

| Segmented Income Statement by Product Lines | |||||||||||||||

| For the Fiscal Year Ended April 30, 20x0 | |||||||||||||||

| Product Lines | |||||||||||||||

| Furniture | Sports | Appliances | Unallocated | Total | |||||||||||

| Sales in units | 160,000 | 180,000 | 160,000 | ||||||||||||

| Sales | $ | 1,440,000 | $ | 3,780,000 | $ | 2,240,000 | â | $ | 7,460,000 | ||||||

| Variable manufacturing and selling costs | 1,120,000 | 2,124,000 | 1,681,600 | â | $ | 4,925,600 | |||||||||

| Contribution margin | $ | 320,000 | $ | 1,656,000 | $ | 558,400 | â | $ | 2,534,400 | ||||||

| Fixed costs: | |||||||||||||||

| Fixed manufacturing overhead | $ | 100,000 | $ | 225,000 | $ | 187,000 | $ | â | $ | 512,000 | |||||

| Depreciation | 131,000 | 147,000 | 134,000 | â | 412,000 | ||||||||||

| Administrative and selling expenses | 121,000 | 143,000 | 82,000 | 844,000 | 1,190,000 | ||||||||||

| Total fixedcosts | $ | 352,000 | $ | 515,000 | $ | 403,000 | $ | 844,000 | $ | 2,114,000 | |||||

| Operating income (loss) | $ | (32,000 | ) | $ | 1,141,000 | $ | 155,400 | $ | (844,000 | ) | $ | 420,400 | |||

| Required: | |

| 1. | Prepare a segmented income statement for Pacific Rim Industriesbased on the company's geographical areas. (Input allamounts as positive values except losses which should be indicatedby minus sign. Do not round intermediate calculations and roundfinal answers to the nearest dollar amount. Omit the "$" sign inyour response.) |

| PACIFIC RIM INDUSTRIES | |||||

| SEGMENTED INCOME STATEMENT BY GEOGRAPHIC AREAS | |||||

| FOR THE FISCAL YEAR ENDED APRIL 30, 20x0 | |||||

| Geographic Areas | |||||

| UnitedStates | Canada | Asia | Unallocated | Total | |

| Sales in units | |||||

| Furniture | |||||

| Sports | |||||

| Appliances | |||||

| Total unitsales | |||||

| Revenue | |||||

| Furniture | $ | $ | $ | $ | |

| Sports | |||||

| Appliances | |||||

| Totalrevenue | $ | $ | $ | $ | |

| Variable costs | |||||

| Furniture | $ | $ | $ | $ | |

| Sports | |||||

| Appliances | |||||

| Totalvariable costs | $ | $ | $ | $ | |

| Contribution margin | $ | $ | $ | $ | |

| Fixed costs | |||||

| Manufacturing | |||||

| overhead | $ | $ | $ | $ | |

| Depreciation | |||||

| Administrative and sellingexpenses | $ | ||||

| Total fixedcosts | $ | $ | $ | $ | $ |

| Operating income (loss) | $ | $ | $ | $ | $ |

***The last person who answered, did not answer the questions in format. Please provide the answers for the required fields on the chart. Label the answers please or list them in a chart like the ones provided in the question.***

*CHECK NUMBERS; PLEASE PROVIDE AN EXPLAINATION FOR EACH AND ANSWER EACH PART FOR QUESTIONS #1-#3 WITH FORMULAS*

Tami Tyler opened Tamiâs Creations, Inc., a small manufacturing company, at the beginning of the year. Getting the company through its first quarter of operations placed a considerable strain on Ms. Tylerâs personal finances. The following income statement for the first quarter was prepared by a friend who has just completed a course in managerial accounting at State University.

| Tamiâs Creations, Inc. Income Statement For the Quarter Ended March 31 | |||||||

| Sales (22,000 units) | $ | 798,600 | |||||

| Variable expenses: | |||||||

| Variable cost of goods sold | $ | 257,400 | |||||

| Variable selling and administrative expenses | 176,000 | 433,400 | |||||

| Contribution margin | 365,200 | ||||||

| Fixed expenses: | |||||||

| Fixed manufacturing overhead | 202,500 | ||||||

| Fixed selling and administrative expenses | 218,000 | 420,500 | |||||

| Net operating loss | $ | ( 55,300 | ) | ||||

Ms. Tyler is discouraged over the loss shown for the quarter, particularly because she had planned to use the statement as support for a bank loan. Another friend, a CPA, insists that the company should be using absorption costing rather than variable costing and argues that if absorption costing had been used the company probably would have reported at least some profit for the quarter.

At this point, Ms. Tyler is manufacturing only one product, a swimsuit. Production and cost data relating to the swimsuit for the first quarter follow:

| Units produced | 25,000 | ||

| Units sold | 22,000 | ||

| Variable costs per unit: | |||

| Direct materials | $ | 7.20 | |

| Direct labor | $ | 2.70 | |

| Variable manufacturing overhead | $ | 1.80 | |

| Variable selling and administrative | $ | 8.00 | |

Required:

1. Complete the following:

a. Compute the unit product cost under absorption costing. (Round your intermediate and final answers to 2 decimal places.)

Unit Product Cost:_______________

b. Redo the companyâs income statement for the quarter using absorption costing. (Round your intermediate calculations to 2 decimal places.)

| |||||||||||||||||||

+

c. Reconcile the variable and absorption costing net operating income (loss) figures. (Round your intermediate calculations to 2 decimal places.)

| ||||||||||

+

3. During the second quarter of operations, the company again produced 25,000 units but sold 28,000 units. (Assume no change in total fixed costs.)

a. Prepare a contribution format income statement for the quarter using variable costing. (Round your intermediate calculations to 2 decimal places.)

| ||||||||||||||||||||||||||||||||||||||||||||||||||

+

b. Prepare an income statement for the quarter using absorption costing. (Round your intermediate calculations to 2 decimal places.)

| |||||||||||||||||||

+

c. Reconcile the variable costing and absorption costing net operating incomes. (Round your intermediate calculations to 2 decimal places.)

| Reconciliation of Variable Costing and Absorption Costing Net Operating Incomes (Losses) | ||

| Variable costing net operating income (loss) | ||

| Absorption costing net operating income (loss) | ||