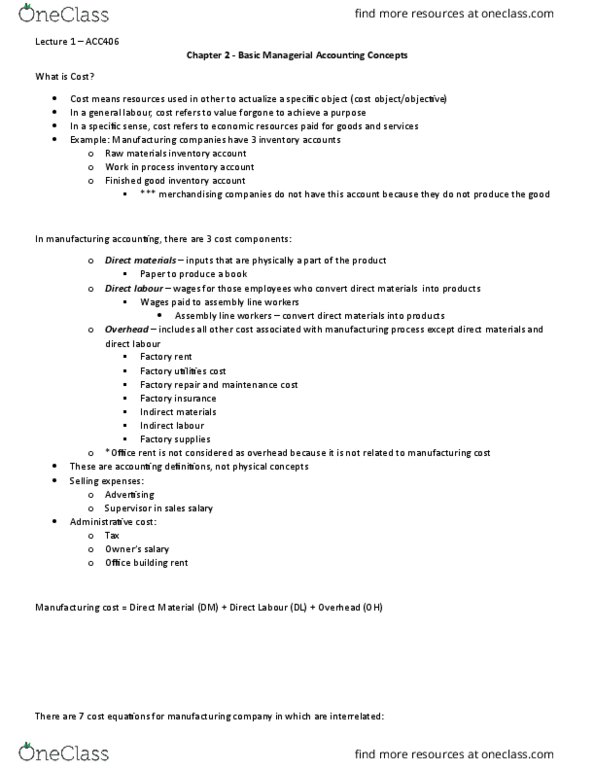

ACC 406 Final: HOW ANSWER ANY QUESTION in ACC406 - Crash course Review

Document Summary

Get access

Related Documents

Related Questions

Looking to achieve the highest grade possible, please see below. Please indicate if this answer is correct. IF I have left a calcuation out, please include.

Thank you,

| The Big Bus Company manufactures two products, Product 1 and Product 2. Product 2 was developed as an attempt to enter a market closely related to that of Product 1. Product 2 is the more complex of the two products, requiring three hours of direct labour time per unit to manufacture compared to one and one-half hours of direct labour time for Product 1. Product 2 is produced on an automated production line. Overhead is currently assigned to the products on the basis of direct labour-hours. The company estimated it would incur a total of $396,000 in manufacturing overhead costs and produce 5,500 units of Product 2 and 22,000 units of Product 1 during the current year. Unit costs for materials and direct labour are: | ||||||||||||

| Product 1 | Product 2 | |||||||||||

| Direct Labour | $7 | $15 | ||||||||||

| Direct material | $9 | $20 | ||||||||||

| Required: | ||||||||||||

| a. Compute the predetermined overhead rate under the current method of allocation and determine the unit product cost of each product for the current year. (5 marks) | ||||||||||||

| Product 1 | Product 2 | Total | Allocation | |||||||||

| Direct Labour hour / unit | 1.5 | 3 | 396,000 / 49,500 | |||||||||

| units produced | 22,000 | 5,500 | 8 | |||||||||

| total labour hour | 33,000 | 16,500 | 49,500 | |||||||||

| overhead/unit | 12 | 24 | overhead/unit is calculated by direct LH x 8 | |||||||||

| Product 1 | Product 2 | |||||||||||

| Direct material | 9 | 20 | ||||||||||

| Direct labour | 7 | 15 | ||||||||||

| overhead/unit | 16 | 35 | ||||||||||

| cost/unit | 32 | 70 | ||||||||||

| b. The company's overhead costs can be attributed to four major activities. These activities and the amount of overhead cost attributable to each for the current year are given below: (5 marks) | ||||||||||||

| Expected Activity | ||||||||||||

| Activity Costs Pools | Estimated Overhead Costs | Product 1 | Product 2 | Total | ||||||||

| Machine set-ups required | $170,000 | 700 | 1,000 | 1,700 | ||||||||

| Purchase orders issued | 37,000 | 300 | 200 | 500 | ||||||||

| Machine-hours required | 91,000 | 4,000 | 9,000 | 13,000 | ||||||||

| Maintenance requests issued | 98,000 | 400 | 600 | 1,000 | ||||||||

| $396,000 | ||||||||||||

| Using the data above and an activity-based costing approach, determine the unit product cost of each product for the current year. | ||||||||||||

| Total Cost | Product A | Product B | ||||||||||

| Machine Setups | 170,000 | 70,000 | 100,000 | |||||||||

| purchase order | 37,000 | 22,200 | 14,800 | |||||||||

| machine hours | 91,000 | 28,000 | 63,000 | |||||||||

| maintenance requests | 98,000 | 39,200 | 58,800 | |||||||||

| Total | 396,000 | 159,400 | 236,600 | |||||||||

| 22,000 | 5,500 | |||||||||||

| overhead /cost | 7..25 | 43..02 | ||||||||||

| product 1 | product 2 | |||||||||||

| Direct Labour | 9 | 20 | ||||||||||

| direct material | 7 | 15 | ||||||||||

| overhead / unit | 7..25 | 43.02. | ||||||||||

| Unit/ cost | 23..25 | 78.020. | ||||||||||

Show your work

Preparing a Comprehensive Budget

Ginnie Springs Company has been bottling and selling water since1940. The companyâs current owner would like to know how a newproduct would affect the companyâs rent income in the comingyear.

Required

Calculate Ginnie Springs net income for the new product in thecoming year by completing the operating budgets and budgeted incomestatement that follow. Assume that the selling price will remainconstant.

Sales budget

Ginnie Springs Company

Sales Budget

Forthe year Ended December 31

Quarter

1 | 2 | 3 | 4 | Year | |

Sales in Units | 40,000 | 30,000 | 50,000 | 55,000 | 175,000 |

Selling price per unit | X $1 | X ? | X ? | X ? | X ? |

Totals Sales | 40,000 | $ ? | X ? | X ? | X ? |

2. Production Budget:

Ginnie SpringsCompany

ProductionBudget

For the year Ended December31_____________

Quarter

1 | 2 | 3 | 4 | Year | |

Sales in Units | 40,000 | ? | ? | ? | ? |

Plus desired units of ending finished goods inventory* | 30,000 | ? | ? | 6000 | 6000 |

Desired total Units | 43000 | ? | ? | ? | ? |

Less desired units of ending finished goods inventory* | 4000 | ? | ? | ? | 4000 |

Total Production units | 39,000 | ? | ? | ? | ? |

*Desired units of ending finished goods inventory = 10% of nextquarterâs budgeted production needs in ounces. Desired ounces ofbeginning direct materials inventory = 20% of current quartersbudgeted production needs in ounces.

3.DirectMaterials Purchases budget

Ginnie SpringsCompany

Direct Materials PurchaseBudget

For the year Ended December31_____________

Quarter

1 | 2 | 3 | 4 | Year | |

Total production units | 39,000 | 32,000 | 50,500 | 55,500 | ? |

Ounces per unit | X 20 | X 20 | X 20 | X 20 | X 20 |

Total production needs in ounces | 780,000 | ? | ? | ? | ? |

Plus desired ounces of ending direct materials inventory* | 128,000 908,000 | ? ? | ? ? | 240,000 ? | 240,000 ? |

Less desired ounces of ending direct materials inventory* | 156,000 | ? | ? | ? | 156,000 |

Total ounces of direct material to be purchased | 752,000 | ? | ? | ? | ? |

Cost per ounce | X $0.01 | X ? | X ? | X ? | X ? |

Total cost of direct materials purchases | $7520 | ? | ? | ? | ? |

Desired ounces of ending direct material inventory =20% of nextquarters budgeted production needs in ounces.

Desired ounces of beginning direct materials inventory = 20% ofcurrent quarters budgeted production needs in ounces.

4.Directlabor budget:

Ginnie SpringsCompany

Direct LaborBudget

For the year EndedDecember 31_____________

Quarter

1 | 2 | 3 | 4 | Year | |

Total production units | 39,000 | ? | ? | ? | ? |

Direct labor hours per units | X 0.001 | X ? | X ? | X ? | X ? |

Total direct labor hours | 39.0 | ? | ? | ? | ? |

Direct labor cost per hour | X $8 | X ? | X ? | X ? | X ? |

Total direct labor cost | $312 | $ ? | $ ? | $ ? | $ ? |

5.Overheadbudget

Ginnie SpringsCompany

Overhead Budget

For the year EndedDecember 31_____________

Quarter

1 | 2 | 3 | 4 | Year | |

Variable overhead costs: | |||||

Factory supplies ($0.01) | $ 390 | $ ? | $ ? | $ ? | $ ? |

Employee benefits ($0.05) | 1,950 | ? | ? | ? | ? |

Inspection ($0.01) | 390 | ? | ? | ? | ? |

Maintenance and repairs($0.02) | 780 | ? | ? | ? | ? |

Utilities ($0.01) | 390 | ? | ? | ? | ? |

Total Variable overheadcosts | $3900 | $ ? | $ ? | $ ? | $ ? |

Total fixed overhead costs | 1416 | ? | ? | ? | ? |

Total overhead costs | $5,316 | $ ? | $ ? | $ ? | $ ? |

Note: The figures in parentheses are variable costs perunit.

6.Sellingand administrative expenses budget:

Ginnie SpringsCompany

Selling and Administrative Expenses Budget

For the year EndedDecember 31_____________

Quarter

1 | 2 | 3 | 4 | Year | |

Variable Selling and Administrative expenses | |||||

Delivery expenses ($0.01) | $ 400 | $ ? | $ ? | $ ? | $ ? |

Sales Commission ($0.02) | 800 | ? | ? | ? | ? |

Accounting ($0.01) | 400 | ? | ? | ? | ? |

Other administrative expenses($0.01) | 400 | ? | ? | ? | ? |

Total Variable selling and administrative exp. | $2,000 | $ ? | $ ? | $? | $? |

Total fixed selling and administrative exp. | 5000 | ? | ? | $? | ? |

Total selling and administrative expenses | $ 7,000 | $ ? | $ ? | $ ? | $ ? |

Note: The figures in parentheses arevariable costs per unit

7. Cost of goods manufactured budget:

Ginnie SpringsCompany

Cost of Goods Manufactured Budget

For the year EndedDecember 31_____________

Direct Material Used:

Direct Material Inventory,Beginning

Purchases

Cost of Direct materials available foruse

Less: Direct materials Inventory,ending

Cost of Direct Materialsused

Direct laborcosts:

Overhead costs:

Total manufacturing costs

Work in Process Inventory,beginning*

Less: work in process inventory,ending*

Cost of Goods Manufactured

Units produced

Manufactured cost perunit

It is the companyâs policy to have no units in process at theend of theyear.

8. Budgeted income statement

Ginnie Springs Company

Selling and Administrative Expenses Budget

For the year EndedDecember 31_____________

Sales

Cost of goods sold

Finished goods inventory beginning

Cost of goods manufactured

Cost of Goods available for sale

Less finished goods inventory, ending

Cost of good sold

Gross margin

Selling and administrative expenses

Income from operations

Income taxes expenses (30% tax rate)

Net Income

Wallis Company manufactures only one product and uses a standard cost system. The company uses a predetermined plantwide overhead rate that relies on direct labor-hours as the allocation base. All of the company's manufacturing overhead costs are fixedâit does not incur any variable manufacturing overhead costs. The predetermined overhead rate is based on a cost formula that estimated $2,899,000 of fixed manufacturing overhead for an estimated allocation base of 289,900 direct labor-hours. Wallis does not maintain any beginning or ending work in process inventory.

The companyâs beginning balance sheet is as follows:

| Wallis Company | ||

| Balance Sheet | ||

| 1/1/XX | ||

| (dollars in thousands) | ||

| Assets | ||

| Cash | $ | 850 |

| Raw materials inventory | 300 | |

| Finished goods inventory | 420 | |

| Property, plant, and equipment, net | 10,000 | |

| Total assets | $ | 11,570 |

| Liabilities and Equity | ||

| Retained earnings | $ | 11,570 |

| Total liabilities and equity | $ | 11,570 |

The companyâs standard cost card for its only product is as follows:

| Inputs | (1) Standard Quantity or Hours | (2) Standard Price or Rate | Standard Cost (1) Ã (2) | ||||

| Direct materials | 2 pounds | $ | 33.00 | per pound | $ | 66.00 | |

| Direct labor | 3.00 hours | $ | 15.00 | per hour | 45.00 | ||

| Fixed manufacturing overhead | 3.00 hours | $ | 10.00 | per hour | 30.00 | ||

| Total standard cost per unit | $ | 141.00 | |||||

During the year Wallis completed the following transactions:

Purchased (with cash) 237,500 pounds of raw material at a price of $31.00 per pound.

Added 218,750 pounds of raw material to work in process to produce 96,500 units.

Assigned direct labor costs to work in process. The direct laborers (who were paid in cash) worked 248,000 hours at an average cost of $16.00 per hour to manufacture 96,500 units.

Applied fixed overhead to work in process inventory using the predetermined overhead rate multiplied by the number of direct labor-hours allowed to manufacture 96,500 units. Actual fixed overhead costs for the year were $2,747,500. Of this total, $1,355,000 related to items such as insurance, utilities, and salaried indirect laborers that were all paid in cash and $1,392,500 related to depreciation of equipment.

Transferred 96,500 units from work in process to finished goods.

Sold (for cash) 93,500 units to customers at a price of $170 per unit.

Transferred the standard cost associated with the 93,500 units sold from finished goods to cost of goods sold.

Paid $2,127,500 of selling and administrative expenses.

Closed all standard cost variances to cost of goods sold.

Required:

1. Compute all direct materials, direct labor, and fixed overhead variances for the year.

2. Record transactions a through i for Wallis Company.

3. Compute the ending balances for Wallis Companyâs balance sheet.

4. Prepare Wallis Companyâs income statement for the year.

Compute all direct materials, direct labor, and fixed overhead variances for the year. (Indicate the effect of each variance by selecting "F" for favorable, "U" for unfavorable, and "None" for no effect (i.e., zero variance). Input all amounts as positive values.)

| ||||||||||||||||||||||

Record transactions a through i for Wallis Company.

Compute the ending balances for Wallis Companyâs balance sheet.

(Unfavorable variances and decreases in balance sheet accounts should be entered with a minus sign. Enter your dollars in thousands.)

Show less

| |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Prepare Wallis Companyâs income statement for the year. (Enter your dollars in thousands. Round your answers to the nearest whole dollar amount.)

| ||||||||||||||||||||||||||||||||||