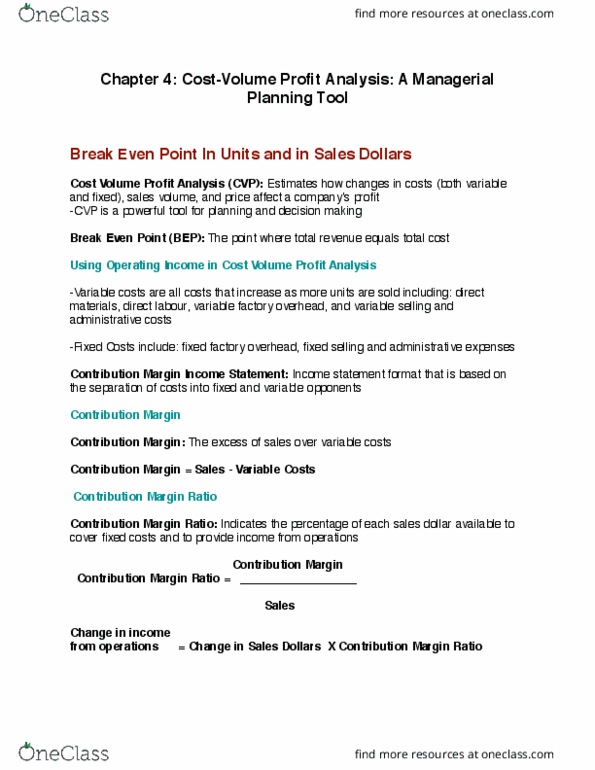

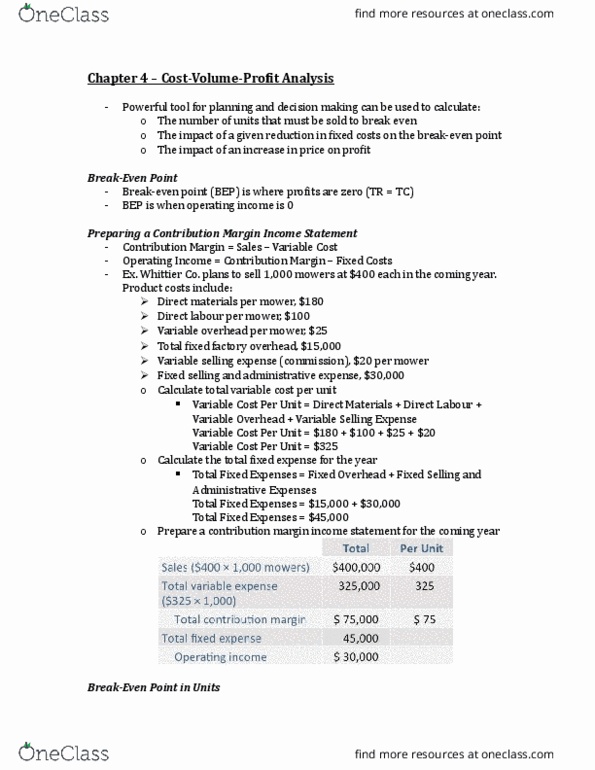

ACC 406 Study Guide - Final Guide: Contribution Margin, Variable Cost, Earnings Before Interest And Taxes

Get access

Related Documents

Related Questions

The Hampshire Company manufactures umbrellas that sell for$12.50 each. In 2014, the company made and sold 60,000 umbrellas.The company had fixed manufacturing costs of $216,000. It also hadfixed costs for administration of $79,525. The per-unit costs ofeach umbrella are as follows:

Direct Materials: $3.00

Direct Labor: $1.50

Variable Manufacturing Overhead: $0.40

Variable Selling Expenses: $1.10

Using the information above, perform a cost-volume-profit (CVP)analysis by completing the steps below.

1. Compute net income before tax.

2. Compute the unit contribution margin in dollars and thecontribution margin ratio for one umbrella.

3. Calculate the break-even point in units and dollars ofrevenue.

4. Calculate the margin of safety:

In units

In sales dollars

As a percentage

5. Calculate the degree of operating leverage.

6. Assume that sales will increase by 20% in 2015. Calculate thepercentage of before-tax income for this increase. Providecalculations to prove that your percentage increase is correctbased on the operating leverage calculated in step 5.

7. Compute the number of umbrellas that Hampshire is required tosell if it plans to earn $150,000 in income before taxes by usingthe target income formula. Proof your calculation.

8. A company that specializes in tours in England has offered topurchase 5,000 umbrellas at $11 each from Hampshire. The variableselling costs of these additional units will be $1.30 as opposed to$1.10 per unit. Also, this production activity will incur another$15,000 of fixed administrative costs. Should Hampshire agree tosell these additional 5,000 umbrellas to the touring business?Provide calculations to support your decision.

| Requirement 1 | ||||

| Units | Price | Totals | ||

| Sales | X | $ | $ | |

| Variable Costs | X | $ | $ | |

| Fixed Costs | $ | |||

| Net Income | $ | |||

| Requirement 2 | ||||

| Contribution Margin per Unitin Dollars = Selling Price â Variable Costs | ||||

| Selling Price | Variable Costs | Contribution Margin per Unit | ||

| Contribution Margin Ratio =Contribution Margin/Selling Price | ||||

| Contribution Margin | Selling Price | Contribution Margin Ratio | ||

| Requirement 3 | ||||

| Break-Even Point = Fixed Costs/ Contribution Margin | ||||

| Fixed Costs | Contribution Margin | Break-Even Point in Units (Rounded) | ||

| Break-Even Point in Units XSelling Price per Unit = Break-Even Point Sales | ||||

| Break-Even Point in Units | Selling Price per Unit | Break-Even Point in Sales (Rounded) | ||

| Requirement 4A | ||||

| Margin of Safety in Units =Current Unit Sales â Break-Even Point in Unit Sales | ||||

| Current Unit Sales | Break-Even Point in Sales | Margin of Safety in Units | ||

| Requirement 4B | ||||

| Margin of Safety in Dollars =Current Sales in Dollars â Break-Even Point Sales in Dollars | ||||

| Current Sales in Dollars | Break-Even Point in Dollars | Margin of Safety in Dollars | ||

| Requirement 4C | ||||

| Margin of Safety as aPercentage = Margin of Sales in Units / Current Unit Sales | ||||

| Margin of Safety in Units | Current Unit Sales | Margin of Safety Percentage | ||

| Requirement 5 | ||||

| Degree of Operating Leverage =Contribution Margin / Operating Income | ||||

| Contribution Margin | Operating Income | Operating Leverage | ||

| Requirement 6 | ||||

| Units | $ Per Unit | Totals | ||

| Sales | X | $ | $ | |

| Variable Costs | X | $ | $ | |

| Fixed Costs | $ | |||

| Net Income | $ | |||

| Operating Leverage | Times % Increase | Increase would be XX% | ||

| Prior Income | $ | From Part 1 | ||

| Increase | $ | Prior Income X XX% Above | ||

| Total | $ | |||

| Requirement 7 | ||||

| Targeted Income = (Fixed Costs+ Target Income) / Contribution Margin | ||||

| Fixed Costs + Target Income | Divided by Contribution Margin | # of Units (Rounded) | ||

| Fixed Costs | $ | |||

| Target Income | $ | |||

| Total | $ | $ | X | |

| # of Units Above X $ Per Unit | ||||

| Proof | Revenue | XX,XXX X $XX.XX | $ | |

| Variable Costs | XX,XXX X $X.XX | $ | ||

| Contribution Margin | $ | |||

| Fixed Costs | $ | |||

| Net Income | $ | |||

| Requirement 8 | ||||

| Sales Mix | ||||

| Current | Specialty | Total | ||

| Expected Sales Units | X | X | ||

| Revenue = Sales X Price | $ | $ | $ | |

| Variable Costs X Units | $ | $ | $ | |

| Contribution Margin | $ | $ | $ | |

| Fixed Costs | $ | $ | $ | |

| Operating Income | $ | |||

| Prior Net Income FromRequirement 1 | $ | |||

| Additional Operating Income | (Operating Income Above Less Prior Income) | $ | ||

| Decision With Explanation | ||||

| Data P5-1: | |||||

| Due to erratic sales of itsproduct--a high-capacity battery for laptop computers--PEM Inc,,has been | |||||

| experiencing difficulty forsome time. The company's contribution format income statement forthe most | |||||

| recent month is given belowalong with other information. | |||||

| PEM, INC. | |||||

| Information from recent month's incomestatement: | |||||

| Sales | $585,000 | ||||

| Units sold | 19,500 | ||||

| Sales price per unit | $30 | ||||

| Less variable expenses | 409,500 | ||||

| Contribution margin | 175,500 | ||||

| Less fixed expenses | 180,000 | ||||

| Net operating loss | ($4,500) | ||||

| Information for Part 2: | |||||

| Increase in monthly advertisingbudget | $16,000 | ||||

| Increase in monthly sales | $80,000 | ||||

| Information for Part 3: | |||||

| Reduction in selling price | 10% | ||||

| Increase in monthly advertisingbudget | $60,000 | ||||

| Increase in monthly unit sales | 100% | ||||

| Information for Part 4: | |||||

| Increase in packaging cost per unit | $0.75 | ||||

| Targeted profit each month | $9,750 | ||||

| Information for Part 5: | |||||

| Reduction in variable costs per unit | $3 | ||||

| Increase in monthly fixed costs | $72,000 | ||||

| Expected sales in units | 26,000 | ||||

| Required: | |||||

| 1. Compute the company's CMratio and its break-even point in both units and dollars. | |||||

| 2. The president believes thata $16,000 increase in the monthly advertising budget, combined withan | |||||

| intensified effort by the sales staff, will result in an $80,000increase in monthly sales. If the president | |||||

| isright, what will be the effect on the company's monthly netoperating income or loss? (Use the | |||||

| incrementalapproach in preparing your answer.) | |||||

| 3. Refer to the original data.The sales manager is convinced that a 10% reduction in the sellingprice, | |||||

| combined with an increase of $60,000 in the monthly advertisingbudget, will cause unit sales to | |||||

| double. What will the new contribution format income statement looklike if these changes are adopted? | |||||

| 4. Refer to the original data.The Marketing Department thinks that a fancy new package for thelaptop | |||||

| computer battery would help sales. The new package would increasepackaging costs by 75 cents per | |||||

| unit.Assuming no other changes, how many units would have to be soldeach month to earn a profit of | |||||

| $9,750? | |||||

| 5. Refer to the original data.By automating certain operations, the company could reduce variablecosts by | |||||

| $3 per unit.However, fixed costs would increase by $72,000 eachmonth. | |||||

| a.Compute the new CM ratio and the new break-even point in both unitsand dollars. | |||||

| b.Assume that the company expects to sell 26,000 units next month.Prepare two contribution format | |||||

| incomestatements, one assuming that operations are not automated and oneassuming that they are. | |||||

| (Show dataon a per unit and percentage basis, as well as in total for eachalternative.) | |||||

| c.Would you recommend that the company automate its operations?Explain. | |||||