COMM 221 Study Guide - Final Guide: Risk Premium, Arbitrage, Sharpe Ratio

Document Summary

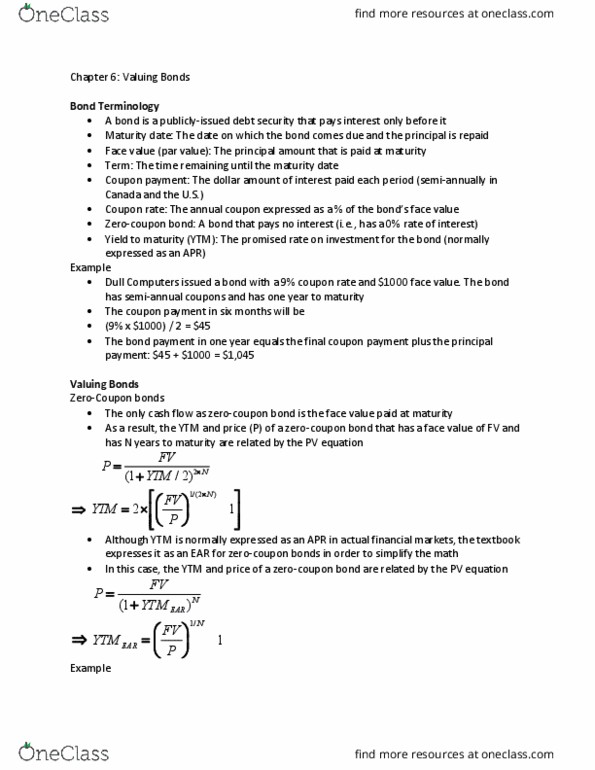

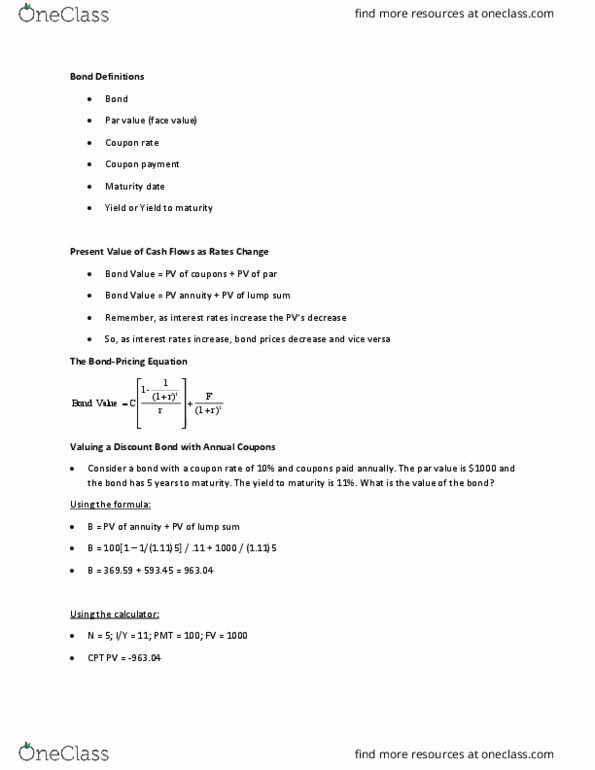

Cost = loss x current items sold. Value of stock = #shares x $/share. Attractive r pv x ( 1+r ) Cash value today = cash + npv. = er rf rs=rf + risk prem . Pv of amount earned on sabbatical : find edr where n = # of compounding periods, 2) pv of annuity where r = rs, and n = # of n in part 1. To find n, 1) pv, solve for n, 2) = 0. 5(er of mp) 0. 5( rf : half as a variable = half risk premium of. P when y is x p when y is y. Taking advantage of an arbitrage opportunity : find p by finding ytm for all years through. , if less than offer, there is arbitrage. Face value x ( 1 d )+ d x r ( 1+ y )n. Ytm expressed as ear is not ^1/n, just^ n where n is periods of pmts in a year.