COMM 122 Study Guide - Final Guide: Net Present Value, Tender Offer, Put Option

30 Apr 2016

School

Department

Course

Professor

Document Summary

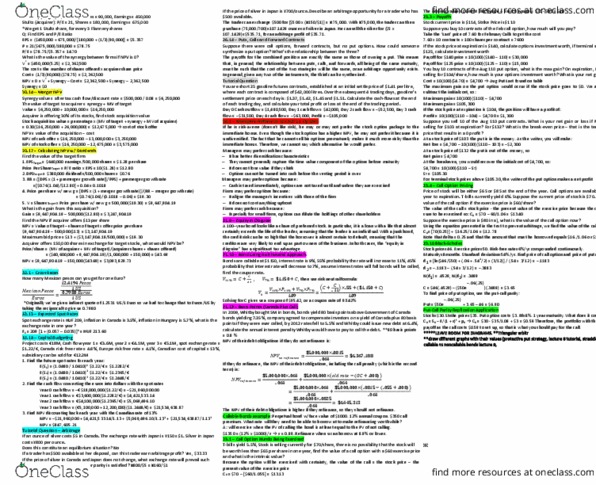

C0= value of call at time t=0 r=rf rate continuously compounded d1 = ln(s/e)+(r+ 2/2)t/ t d2=d1- t. Payoff = # of shares*(strike price - current price) Max payoff = # of shares * strike price - price paid. V of package = price of buying price of selling. Selling gain = cost shares(strike current) Call option: holder has right to buy asset. Put option: holder has right to sell asset. Delta: sensitivity of value of option to changes in price of underlying stock (call: +, put: -) Exec stock options: call option on employer"s shares grants at-the-money are not taxable. Long term debt r , p - no call, p1 = c + c/r r , p - call , p1 = call price + c. Call provision = v non-callable v callable. Negative covenants: limited dividends payments, cannot sell debt, cannot buy other company"s bonds, cannot refund bond issue with new bond with lower rates.