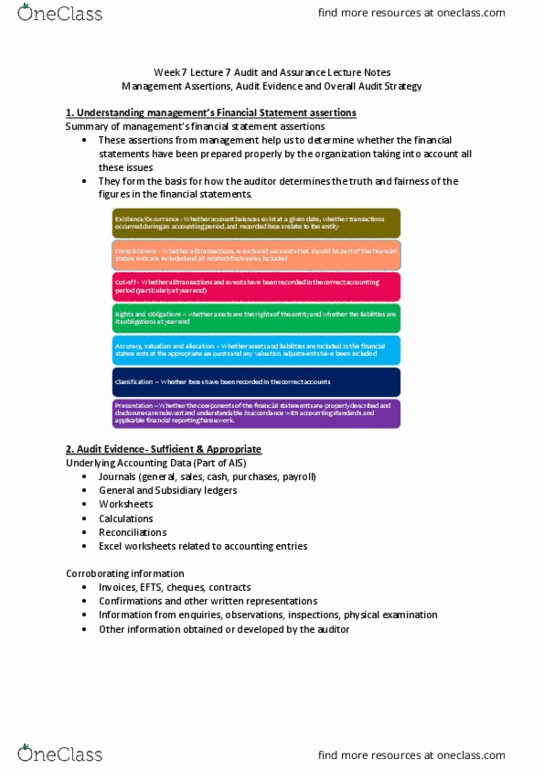

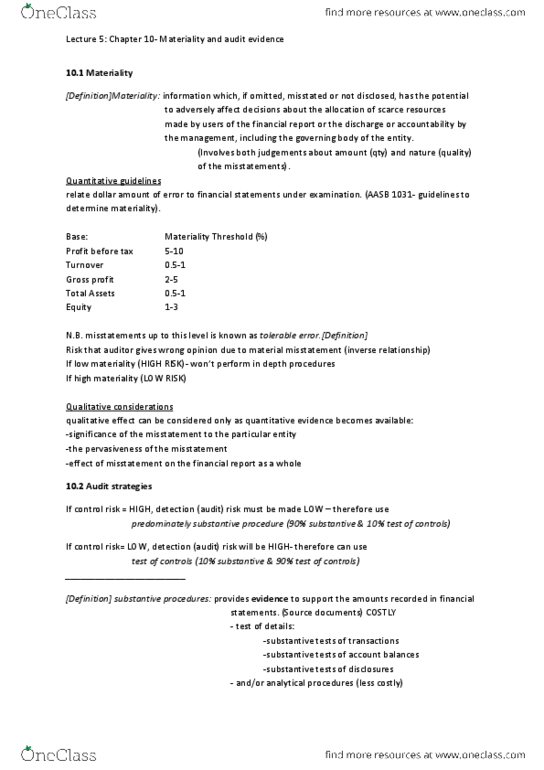

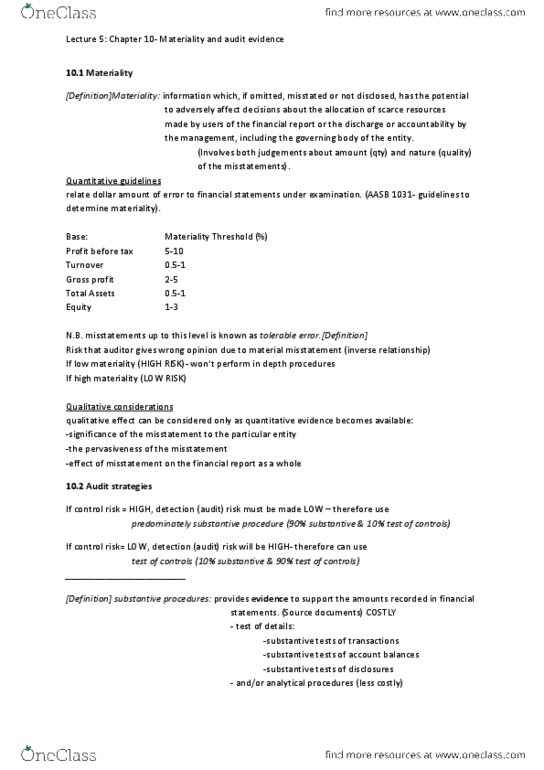

ACCG340 Study Guide - Final Guide: Audit Evidence, Direct Bank, Audit Risk

19 Jun 2018

School

Department

Course

Professor

1"

"

WK 5

Audit evidence – ASA500

1. Audit evidence is a fundamental concept in auditing by which the auditor achieves

the objective of reasonable assurance that none of management’s assertions is

materially misstated, and consists of:

Underlying accounting data

All available corroborating information

Books of original entry

Documents e.g. cheques, authorisations for

direct bank transfers, invoices,

contracts, etc.

General and subsidiary

ledgers

Confirmations and other written

representations

Worksheets, schedules,

calculations, etc.

Information from inquiry, observations,

inspection and physical examination

Related accounting manuals

All other information obtained or

developed by the auditor

2. The auditor is required to design and perform audit procedures to

obtain

sufficient

appropriate audit

evidence

to be able to

draw reasonable conclusions

on which to

base the auditor’s opinion.

Audit evidence is obtained from performance of the 3 audit procedures:

3. Sufficient & Appropriate Audit Evidence - ASA500.5

a)

Sufficient

= measure of

quantity

(concern with sample and the nature of

target)

b)

Appropriate

= measure of

quality

(MORE important; i.e. relevance and

reliability)

Both are a

function of the assessment of risk

of material misstatement and are

interrelated

4. 5 Types/forms of audit evidence

a) oral

b) visual observations

c) physical

d) electronic

e) documentary:

i. accounting records &

supporting/source

documentation

ii. minutes of meetings

iii. confirmations

iv. written representations

v. analytical procedures results

5. Sources of audit evidence - ASA500.A1 & A7-A9

a) Evidence can be:

find more resources at oneclass.com

find more resources at oneclass.com

2"

"

1. Created by external parties and transmitted directly to auditor

2. Created by external parties and held by client

3. Created and held by client

4. Electronic documents

b) The nature and source of the evidence

affect the level of assurance

the auditor

derives from the information

6. Reliability of audit evidence

Audit procedures in response to assessed risks - ASA500.A14-A25

1. 7 TYPES of Audit procedures (

methods and techniques

used to obtain audit evidence):

1. Enquiry

2. Inspection (includes tracing and vouching)

3. Observation

4. External confirmation

5. Re-calculation

6. Re-performance

7. Analytical procedures

These may be used as risk assessment procedures, tests of controls or substantive

procedures, depending on the context in which they are applied by the auditor

(ASA500.A11)

find more resources at oneclass.com

find more resources at oneclass.com

3"

"

Many of these procedures can be performed or facilitated through the use of

generalized audit software

(GAS)

2. Audit procedures: Enquiry à test of control & test of details

a) Consists of seeking information of

knowledgeable persons

, both financial &

non-financial, within or outside the entity.

b)

Evaluating responses

to enquiries is integral part of enquiry process

i. e.g. Enquire of sales personnel concerning possible excess or obsolete

inventory items to identify slow-moving, excess, defective or obsolete

items included in inventory

3. Audit procedures: Inspection and Observation

a) Inspection à test of control & test of details

i. Involves

examining records

or documents, whether internal or external, in

paper form, electronic form, or other media, or a physical examination of

an asset.

ii. e.g. Select a sample of inventory lines and compare with suppliers’ invoices

to ensure inventories are properly stated at cost

b) Observation à test of control

i. Consists of

looking at a process

or procedure being performed by others

(limited to specific point in time)

ii. e.g. Observe inventory test counts by entity’s personnel

4. Audit procedures: External confirmation à test of details

a) Represents audit evidence obtained as a

direct written response

to the auditor

from a

3rd party

, in paper form, or by electronic or other medium

b) Often performed in addressing/verifying account balances

c) Confirmations often OBTAINED:

Information

Source

Cash at bank

Bank/s

Accounts receivables

Customer/s

Owned inventory on consignment

/ external warehouses

Consignee / Warehouse

Accounts payable

Creditor

Other loans/payables

Lender/financier

5. Audit procedures: Re-calculation and Re-performance

a) Re-calculationà test of details

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Audit evidence asa500: audit evidence is a fundamental concept in auditing by which the auditor achieves the objective of reasonable assurance that none of management"s assertions is materially misstated, and consists of: Documents e. g. cheques, authorisations for direct bank transfers, invoices, contracts, etc. Information from inquiry, observations, calculations, etc. inspection and physical examination. Audit procedures in response to assessed risks - asa500. a14-a25: 7 types of audit procedures (methods and techniques used to obtain audit evidence), enquiry, inspection (includes tracing and vouching, observation, external confirmation, re-calculation, re-performance, analytical procedures. These may be used as risk assessment procedures, tests of controls or substantive procedures, depending on the context in which they are applied by the auditor (asa500. a11) Lender/financier: audit procedures: re-calculation and re-performance, re-calculation test of details. Consists of checking the mathematical accuracy of documents or records (manually or electronically) e. g. multiplying inventory on hand by inventory cost price to check inventory valuation: re-performance test of control.