FIN111 Lecture Notes - Lecture 7: Opportunity Cost, Credit Risk, 6 Years

Week 7 – Bond Valuation and the Structure of Interest Rates

Corporate Bonds

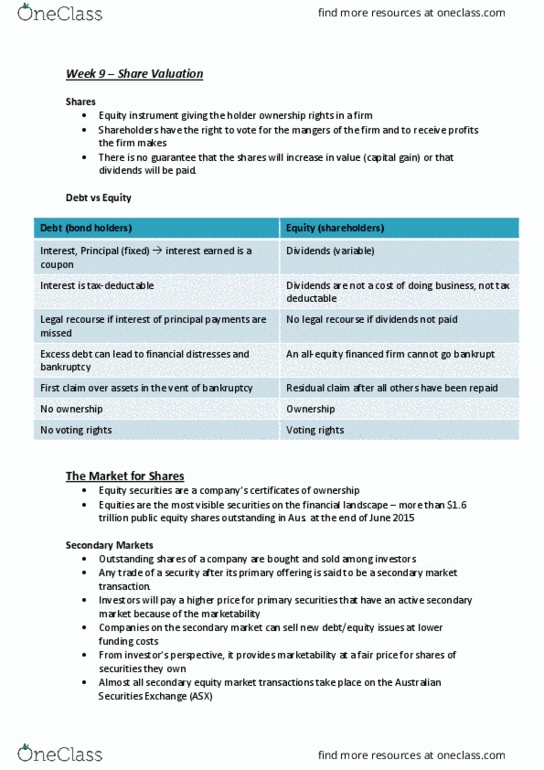

Market for Corporate Bonds

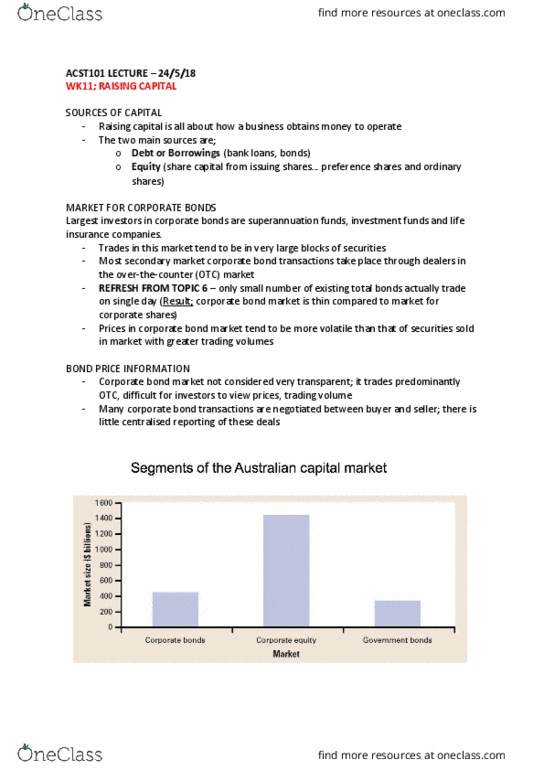

• June 2011 – value of bonds outstanding in Aus. was $447 billion → second largest

portion of the Australian capital market

• Largest investors in corporate bonds are superannuation fund, investment funds and

life insurance companies

• Trades in this market tend to be in very large blocks of securities

• Most secondary market corporate bond transactions take place through dealers in

the over-the-counter (OTC) market

- NOT trading in the stock exchange – using phones or online

• Despite the large overall trading volume, only a small number of existing total bonds

actually trade on single day

- Result: corporate bond market is thin compared to market for money market

securities or corporate shares

- Thin = not as liquid, not much trading, infrequent

• Corporate bonds less marketable than securities with higher daily trading volumes

- Moeet ist that geat opaed ith shaes, oeet is uite stale

• Prices in corporate bond market also tend to be more volatile than that of securities

sold in market with greater trading volumes

• Ifoatio ot efleted i pies as effiietl ad the aket ist as effiiet as

those for shares or money market instruments

Bond Price Information

• Corporate bond market not considered very transparent; it trades predominantly

OTC, difficult for investors to view prices, trading volume

- If you are buying shares you can see how many people are buying and selling

every second

- Hard to trace

• Also, many corporate bond transactions are negotiated between buyer and seller;

there is little centralized reporting of these deals

• Information on individual bonds not widely published

find more resources at oneclass.com

find more resources at oneclass.com

Types of Corporate Bonds

• Corporate bonds are long-term IOUs that represent clais agaist a opas

assets

- i.e. I can claim the money used to purchase later on

• Debt instruments where the interest income paid to investors is fixed for the life of

the contract are called fixed-income securities

• Steady income because the amount you will receive is fixed

• Three types of corporate bonds are – coupon bonds, zero coupon bonds, and

convertible bonds

• NOTE: not equity

Coupon Bonds

• Called coupon bonds because the coupon is attached to the bond. In the past

(before electronics) all bonds came with a piece of paper and at the bottom it had a

coupon to present to the company to claim interest

• These bonds have coupon payments fixed for life of bond, and at maturity, principal

is paid and bonds are retired

• Coupon bonds have no special provisions; provisions they do have are conventional

and common to most bonds, e.g., a call provision

• Coupon payment are the interest payments made to the bondholder

• Payments usually made annually or semiannually

• Sometimes called vanilla bond → plain and simple

Zero Coupon Bonds

• Companies sometimes issue bonds with no coupon payments, only offering one

payment at maturity

• Interest is the difference between the price paid for the bond and the face amount

received at maturity

• Zero coupon bonds sell well below their face value (at deep discount) because they

offer no coupons

• Not frequently issued in Australia

Convertible Bonds

• Bonds that can be converted into ordinary shares at pre-determined ratio at

discretion of bondholder

• Coetile featue allos odholdes to shae opas good fotues if the

opas shares rise above certain level

• Coesio atio is set so opas shae pie ust appeiate 5%-20% before it

is profitable to convert bonds into equity:

- To secure this advantage, bondholders willing to pay a premium

find more resources at oneclass.com

find more resources at oneclass.com

Bond Valuation

A Bond

• Is a contract between the issuer (borrower) and the investor (lender) stipulating the

issues oligatios to ake speified paets o speified futue dates

• Has a value equal to the present value of all cash flows associated with holding the

bond

• Cash flos osist of peiodi iteest paets ad the epaet of the fae

value upon maturity

• Yield to maturity → required rate of return, or discount rate for a bond is the market

interest rate

• To alulate ods pie, follo sae poess as to alue a fiaial asset:

1. Estimate expected future cash flows – coupons and the principal of the bond

2. Deteie ods euied ate of return, or discount rate

3. Calculate current value, or price of a bond (PB) by calculating the present value

of ods epeted ash flos

Bond Terminology

Principal

The amount of money on which interest is paid

Maturity date

The date he a ods life eds ad the ooe ust make the final interest

payment and repay the principal

Par Value

The face value of a bond, which the borrower repays at maturity

Coupon

A fixed amount of interest that a bond promises to pay investors

Coupon rate

The ate deied diidig the ods annual coupon payment by its par value

Coupon yield

The aout otaied diidig the ods oupo its uet aket pie

(which does not always equal its par value). Also called current yield

Yield to Maturity

The market required rate of return for bonds of similar risk and maturity

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Week 7 bond valuation and the structure of interest rates. Not trading in the stock exchange using phones or online: despite the large overall trading volume, only a small number of existing total bonds actually trade on single day. Result: corporate bond market is thin compared to market for money market securities or corporate shares. Thin = not as liquid, not much trading, infrequent: corporate bonds less marketable than securities with higher daily trading volumes. Mo(cid:448)e(cid:373)e(cid:374)t is(cid:374)(cid:859)t that g(cid:396)eat (cid:272)o(cid:373)pa(cid:396)ed (cid:449)ith sha(cid:396)es, (cid:373)o(cid:448)e(cid:373)e(cid:374)t is (cid:395)uite sta(cid:271)le: prices in corporate bond market also tend to be more volatile than that of securities sold in market with greater trading volumes. I(cid:374)fo(cid:396)(cid:373)atio(cid:374) (cid:374)ot (cid:396)efle(cid:272)ted i(cid:374) p(cid:396)i(cid:272)es as effi(cid:272)ie(cid:374)tl(cid:455) a(cid:374)d the (cid:373)a(cid:396)ket is(cid:374)(cid:859)t as effi(cid:272)ie(cid:374)t as those for shares or money market instruments. Bond price information: corporate bond market not considered very transparent; it trades predominantly. Otc, difficult for investors to view prices, trading volume.