FIN111 Lecture 9: Week 9 – Share Valuation

Week 9 – Share Valuation

Shares

• Equity instrument giving the holder ownership rights in a firm

• Shareholders have the right to vote for the mangers of the firm and to receive profits

the firm makes

• There is no guarantee that the shares will increase in value (capital gain) or that

dividends will be paid.

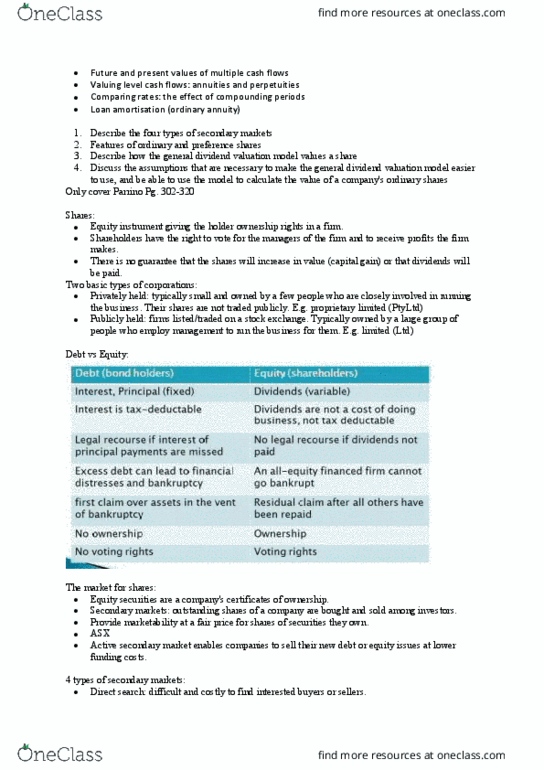

Debt vs Equity

Debt (bond holders)

Equity (shareholders)

Interest, Principal (fixed) → interest earned is a

coupon

Dividends (variable)

Interest is tax-deductable

Dividends are not a cost of doing business, not tax

deductable

Legal recourse if interest of principal payments are

missed

No legal recourse if dividends not paid

Excess debt can lead to financial distresses and

bankruptcy

An all-equity financed firm cannot go bankrupt

First claim over assets in the vent of bankruptcy

Residual claim after all others have been repaid

No ownership

Ownership

No voting rights

Voting rights

The Market for Shares

• Equity securities are a compas etifiates of oeship

• Equities are the most visible securities on the financial landscape – more than $1.6

trillion public equity shares outstanding in Aus. at the end of June 2015

Secondary Markets

• Outstanding shares of a company are bought and sold among investors

• Any trade of a security after its primary offering is said to be a secondary market

transaction.

• Investors will pay a higher price for primary securities that have an active secondary

market because of the marketability

• Companies on the secondary market can sell new debt/equity issues at lower

funding costs

• Fo iestos pespetie, it poides marketability at a fair price for shares of

securities they own

• Almost all secondary equity market transactions take place on the Australian

Securities Exchange (ASX)

find more resources at oneclass.com

find more resources at oneclass.com

• Markets are efficient when current market prices of securities traded reflect all

available information relevant to the security.

Four Types of Secondary Markets (in order of increasing market efficiency):

1. Direct Search

- Buyers/sellers seek each other out directly

- Sellers often rely on word-of-mouth communication to find buyers

- Difficult and costly

2. Broker

- Brokers bring buyers and sellers together to earn a fee, called a commission

- To provide investors with an incentive to hire them, brokers may charge a

commission that is less than the cost of a direct search.

- Aggressively seek out buyers and sellers and try to negotiate

- Increases market efficiency because brokers are in frequent contact with market

participants and are likel to ko hat ostitutes a fai pie

3. Dealer

- Provide this service by holding inventories of securities which they own

- Then buy new securities and sell from inventory to earn a profit

- They have capital risk – difference between bid price and offer price

4. Auction

- Buyers and sellers confront each other directly and bargain over price

Reading the Share Market Readings

• Most financial press, The Australian Financial Review, Wall Street Journal, The New

York Times provide share listings for major share exchanges, such as NYSE and

relevant regional exchanges

• Franking

- f – dividend is 100% franked – company has fully paid tax on the dividend

- p – the dividend is partly franked

- lak spae i the f o p olu idiates the diided is unfranked (no tax)

• Offer basic security market information:

- Price: bid, ask, last, high, low

- Dividend: last dividend, franked, partial

- Return: P/E, dividend yield

• 52 wk high/low → companies highest and lowest price in 52 weeks

• last sale → last price before closing

• + or - → changes

• quote buy/quote sell → highest bid price/highest ask price

• div c per share → annual dividend pay

• div times covered → the number of times the company profits cover latest dividend

• NTA → net tangible asset per share ratio

• Div Yld % → dividend yield. Annual div payout over current share price

• P/E ratio → current price per share over current earnings per share

find more resources at oneclass.com

find more resources at oneclass.com

Ordinary and Preference Shares

Ordinary Shares

• Ordinary shares represent a basic ownership claim in a company

• Vote on all important matters that affect life of company, such as vote to elect board

of directors, capital budget, or proposed merger or acquisition

• Not guaranteed any dividend payments

• Loest pioit lai o opas assets i eet of isole

• Limited liability → losses limited to the amount of their investment

• Perpetuities in the sense that they have no maturity

• Can be retired only if management buys them in the open market from investors or

if the company is liquidated

Preference Shares

• Preference share owners are given priority over ordinary share owners with respect

to diideds paets ad lais agaist opas assets i eent of insolvency or

liquidation

• Preference share dividends are declared by the board of directors, and if a dividend

is not paid the lack of payment is not legally viewed as a default

• Legally a form of equity and paid by the issuer with after-tax dollars

• Even though preference shares are equity, owners have no voting privileges

• Most preference shares are not true perpetuities because their share contracts often

contain call provisions and can even include sinking fund provisions, which require

management to retire a certain percentage of the share issue annually until the

entire issue is retired.

• Dividends

- egadless of fis earnings

- stated percentage

- Dividend payments are paid with after-ta dollas sujet to taatio

Preference shares: debt or equity?

• Legally, preference shares are equity because they are the ownership of the

company

• Strong case that preference shares are a special type of bond because:

- They confer no voting rights

- Shaeholdes eeie a fied diided, egadless of opas eaigs

- If liquidated, shareholders receive a stated value (usually par) and not a residual

value.

- Preference shares often have edit atigs that ae siila i atue to those

issued to bonds

- Preference shares are some- times convertible into ordinary shares

- Most preference share issues are not true perpetuities

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Interest, principal (fixed) interest earned is a coupon. Dividends are not a cost of doing business, not tax deductable. Legal recourse if interest of principal payments are missed. Excess debt can lead to financial distresses and bankruptcy. First claim over assets in the vent of bankruptcy. Residual claim after all others have been repaid. Voting rights: equity securities are a compa(cid:374)(cid:455)(cid:859)s (cid:272)e(cid:396)tifi(cid:272)ates of o(cid:449)(cid:374)e(cid:396)ship, equities are the most visible securities on the financial landscape more than . 6 trillion public equity shares outstanding in aus. at the end of june 2015. Secondary markets: outstanding shares of a company are bought and sold among investors, any trade of a security after its primary offering is said to be a secondary market transaction. Securities exchange (asx: markets are efficient when current market prices of securities traded reflect all available information relevant to the security. Four types of secondary markets (in order of increasing market efficiency): direct search.