L11 Econ 1011 Chapter Notes - Chapter 8: Monopolistic Competition, Substitute Good, Perfect Competition

16 May 2018

School

Department

Course

Professor

Chapter 8 Monopoly, Oligopoly, and Monopolistic Competition

Imperfect Competition

• Price setter – a firm with at least some latitude to set its own price

• Pure monopoly – the only supplier of a unique product with no close substitutes

• Monopolistic competition – an industry structure in which a large number of firms

produce slightly differentiated products that are reasonably close substitutes for one

another

o Ex: gas stations, convenience stores – differ in location and what they offer, but

similar

o Entry and exit causes a 0 economic profit (like a perfectly competitive firm) in the

long run

o They can charge a slightly higher price than other firms and not lose all its

customers

• Oligopoly – an industry structure in which a small number of large firms produce

products that are either close or perfect substitutes

o A consequence of cost advantages that prevent small firms from being able to

compete effectively

o Some sell undifferentiated products

o Ex: mobile phone carriers sell basically the same thing

o Pricing and advertising are important strategic decisions for firms

o No presumption that entry and exit will push economic profit to zero

o No guarantee that an oligopolist will earn a positive economic profit

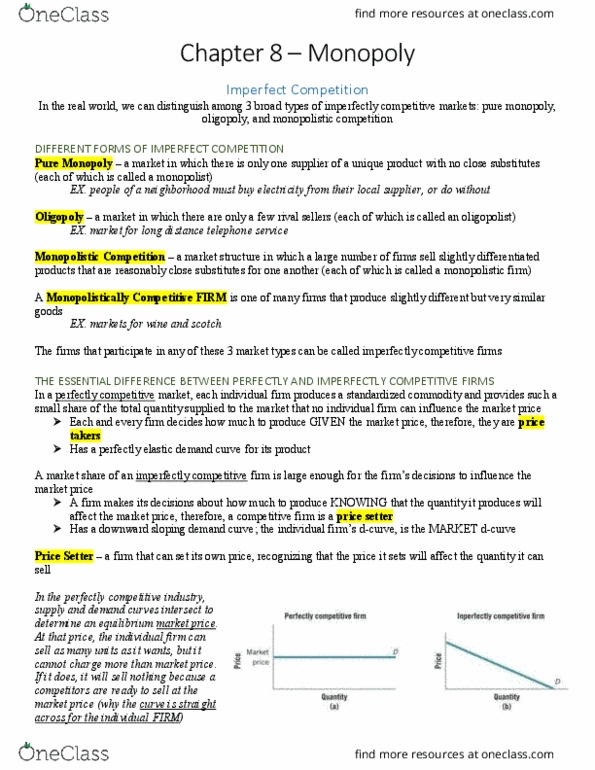

• Perfectly competitive firms face a perfectly elastic demand curve for its product,

o a horizontal line at the market price

• Imperfectly competitive firms face a downward-sloping demand curve

o A negatively sloped demand curve

5 Sources of Market Power

• Market power – a firm’s ability to raise the price of a good without losing all its sales

o only can pick a price-quantity combination on its demand curve

o if a firm chooses to raise its price, it must settle for reduced sales

• Exclusive Control Over Important Inputs – if a single firm controls an input essential to

the production of a given product, that firm will have market power

• Patents and Copyrights – patents give the inventors or developers of new products the

exclusive rights to sell those products for a specified period of time

o By insulating sellers from competition for an interval, patents enable innovators to

charge higher prices to recoup their product’s development costs

• Government Licenses or Franchises

o Ex: Yosemite Concession Services Corporation has an exclusive license to run the

lodging and concession operations at Yosemite

▪ Their goal is to preserve the wilderness as much as possible

• Economies of Scale and Natural Monopolies

o Constant returns to scale – a production process is said to have constant returns

to scale if, when all inputs are changed by a given proportion, output changes by

the same proportion

find more resources at oneclass.com

find more resources at oneclass.com

▪ If output exactly doubles

o Increasing returns to scale (economies of scale) – a production process is said

to have increasing returns to scale if, when all inputs are changed by a given

proportion, output changes by more than that proportion

▪ If output more than doubles

▪ The average cost of production declines as the number of units produced

increases

o Natural monopoly – a monopoly that results from economies of scale (increasing

returns to scale)

▪ Ex: generators of electricity have only a few sellers

• Network Economies - when network economies are of value to the consumer, a product’s

quality increases as the number of users increases, so we can say that any given quality

level can be produced at lower cost as sales volumes increases

o can be viewed as just another form of economies of scale in production

o Ex: Microsoft’s Windows operating system has a sales advantage, is in most

computers

• For a firm whose total cost curve of producing Q units of output per year is

TC = F + M*Q, total cost rises at a constant rate as output grows, while ATC declines

o ATC is always higher than MC cost of this firm, but the difference becomes less

significant at high output levels because the firm is spreading out its fixed cost

over an extremely large volume output

o F = fixed cost, M = marginal cost, Q = level of output produced

o Variable cost = M*Q

o ATC = TC/Q = F/Q + M

▪ As Q increases, average cost declines steadily because the fixed costs are

spread out over more and more units of output

• For products with large fixed costs, marginal cost is lower, often substantially, than ATC,

and ATC declines, often sharply, as output grows

o This explains why many industries are dominated by either a single firm or a

small number of firms

Profit Maximization for the Monopolist

• Marginal revenue – the change in a firm’s total revenues that results from a one-unit

change in output

o In a perfectly competitive firm, marginal revenue is exactly equal to the market

price of the product

▪ Ex: if the price is $6, then the marginal benefit of selling an extra unit is

exactly $6

• To a monopolist, the marginal benefit of selling an additional unit is strictly less than the

market price

o Ex: a monopolist receives $12 per week in total revenue by selling 2 units per

week at a price of $6 each

▪ This monopolist could earn $15/week by selling 3 units per week at a

price of $5 each

find more resources at oneclass.com

find more resources at oneclass.com