ACIS 2115 Chapter Notes - Chapter 8: Financial Statement, Income Statement, Ge Capital

21 Mar 2016

School

Department

Course

Professor

Document Summary

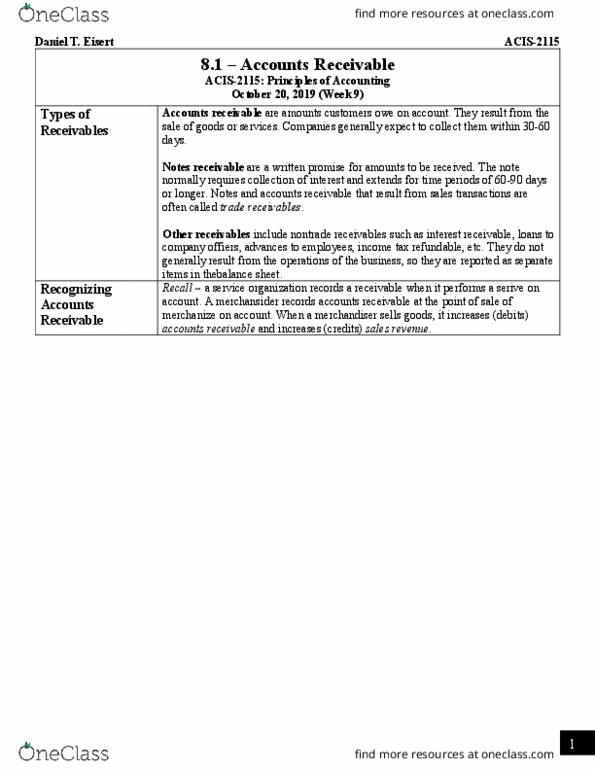

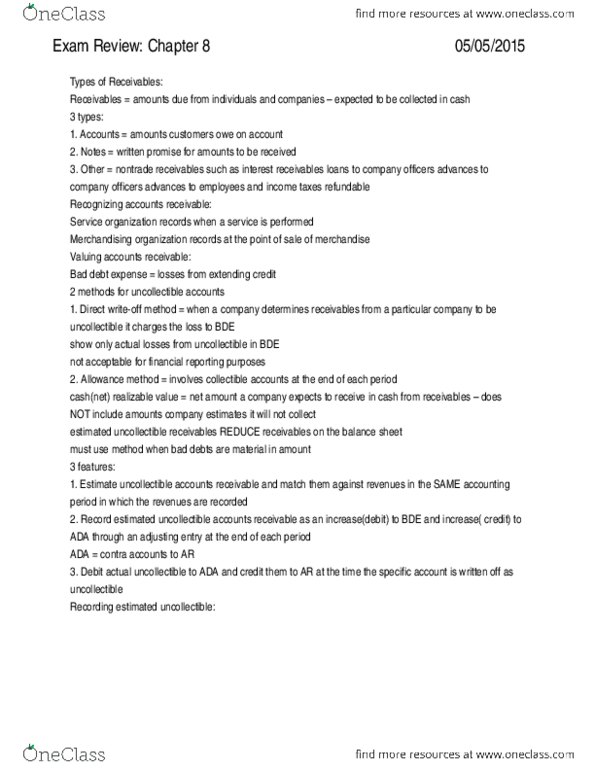

Credit sales revenue: sellers may encourage early payment by ofering sales discounts, sales returns reduce receivables as well d. Journal entries: to record sales on accounts. Credit sales revenue: to record merchandise returned. Credit accounts receivable: to record collecion of accounts receivable. Credit accounts receivable: for companies like jc penny that issue their own credit cards, to record sales on account. Credit sales revenue: to record interest on amount due. Credit accounts receivable: bad debt expense will show only actual losses from uncollecibles. Accounts receivable is reported at its gross amount there is no adjustment for any esimated losses for bad debts: this method can reduce the efeciveness of the income statement and the balance sheet. Under the direct write-of method, companies oten record bad debt expense in a period diferent from the period in which they recorded the revenue. Bad debt expense and sales revenue are not matched. Provides beter matching of expenses with revenues on the income statement.