ACIS 2115 Chapter Notes - Chapter 2: Historical Cost, Financial Accounting Standards Board, Public Company Accounting Oversight Board

9 Feb 2016

School

Department

Course

Professor

Document Summary

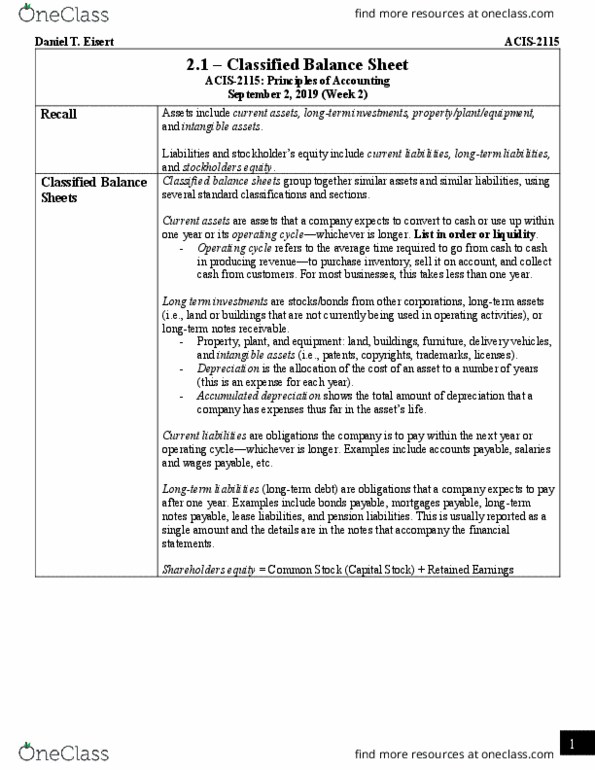

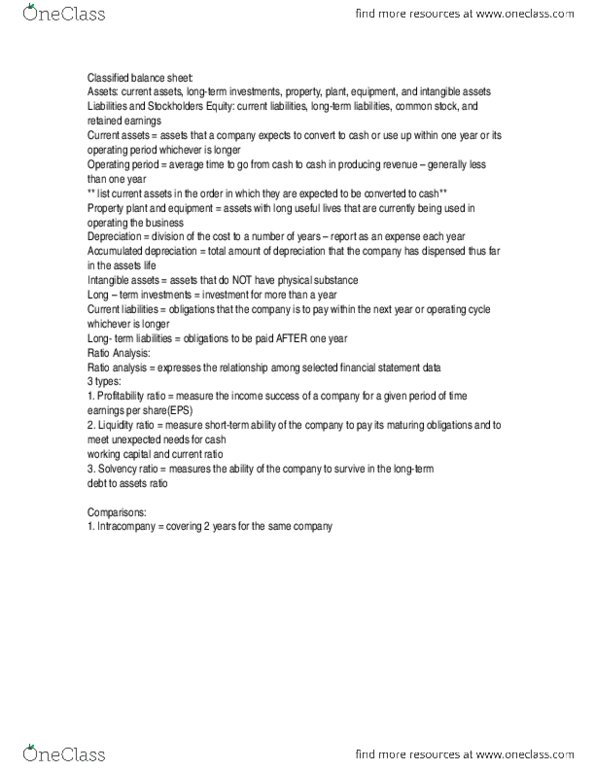

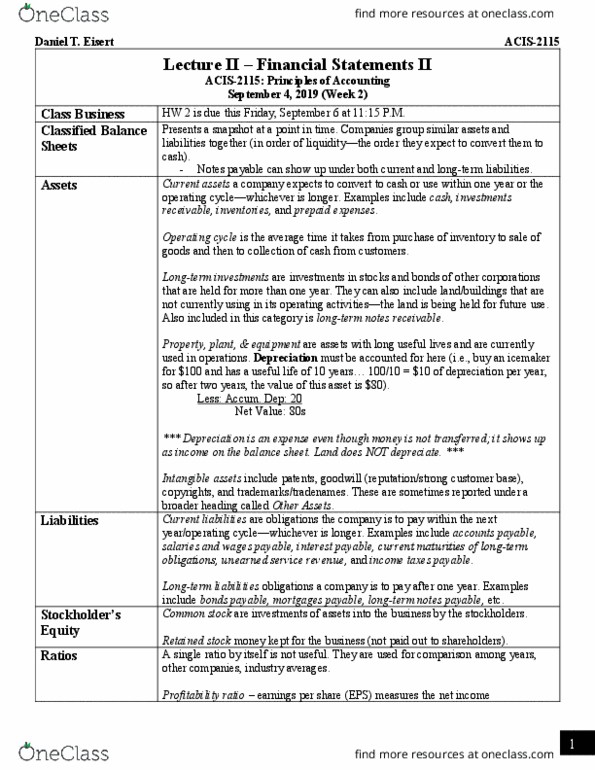

Chapter 2 outline: investments of assets into the business by stockholders, retained earnings. Ii: the income retained for the business. Evaluating profitability, liquidity, and solvency using ratios: ratio analysis, expresses the relationship between selected items of financial statement data, a ratio expresses the mathematical relationship between two quantities, types of comparisons, intracompany comparisons, industry-average comparisons. Compares the company to the average ratios for particular industries. Compares the company with one of its competitors in the industry c. The difference between the amounts of current assets and current liabilities. More dependable indicator of liquidity than working capital. Weakness: does not take into account the composition of the current assets. Assets can either be cash or inventory. Cash is more liquid than objects: solvency ratios. Chapter 2 outline: measures the ability of the company to survive ii. over a long period of time.