MGMT 1A Chapter Notes - Chapter 8: Income Statement

Document Summary

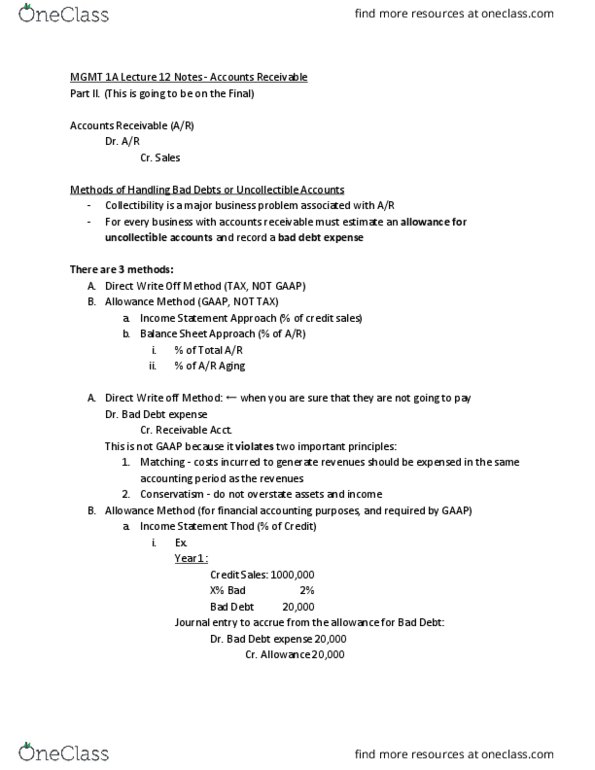

Methods of handling bad debts or uncollectible accounts. % of credit sales: balance sheet approach. Violates principles of gaap: overstates assets and income (revenue) Debit bad debt expense (used for tax purposes and not gaap) Violates gaap b/c of: matching and conservatism principles. Debit allowance for doubtful accounts (used for gaap b/c is accruing for expenses when writing down revenue; matching) Look at sales to get bad debt expense. Credit sales * _% bad = bad debt. Look at a/r to get bad debt expense. A/r * _% bad = total allowance for current year. Previous year allowance + (bad debt for this year) = current year allowance: bad debt = current year allowance previous year allowance. Different percentages of bad debt for different a/rs that have not yet been collected: depends on time, longer it stays as a/r, higher the percentage of bad debt. A/r subtract allowance for doubtful accounts = cash/net realizable value.