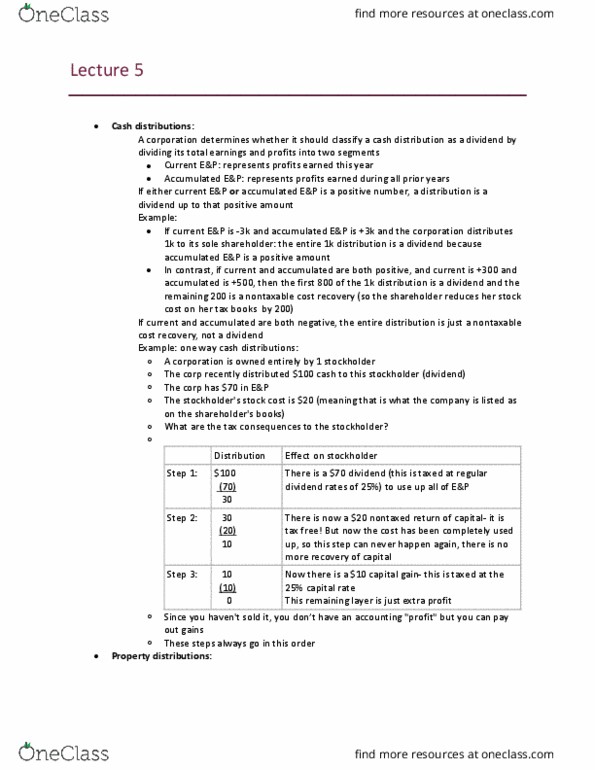

MGMT 127B Chapter Notes - Chapter 5: Qualified Dividend, Accelerated Depreciation, Macrs

Document Summary

Chapter 5: corporations earnings and profits and dividend. In the most common situation, a distribution triggers div income to the shareholder and provides no deduction to the paying corporation which results in a double tax (at the corporate and shareholder level) The corp distributes 20k to its sole shareholder whose stock basis is 4k. In this situation, the sole shareholder recognizes income of 15k (the amount of. Of the remaining 5k distributed, 4k reduces her stock basis to 0 and the sole shareholder recognizes a taxable gain of 1k. To calculate current e&p, it is necessary to add all previously excluded income items back to taxable income. Included among these are interest on municipal bonds, excluded life insurance proceeds (in excess of cash surrender value) and federal income tax refunds from tax paid in prior years. A corporation collects 100k on a key employee life insurance policy (so the corp is the owner and beneficiary of the policy)