BUS 108 Chapter Notes - Chapter 4: Contribution Margin, Unit Price, Fixed Cost

Document Summary

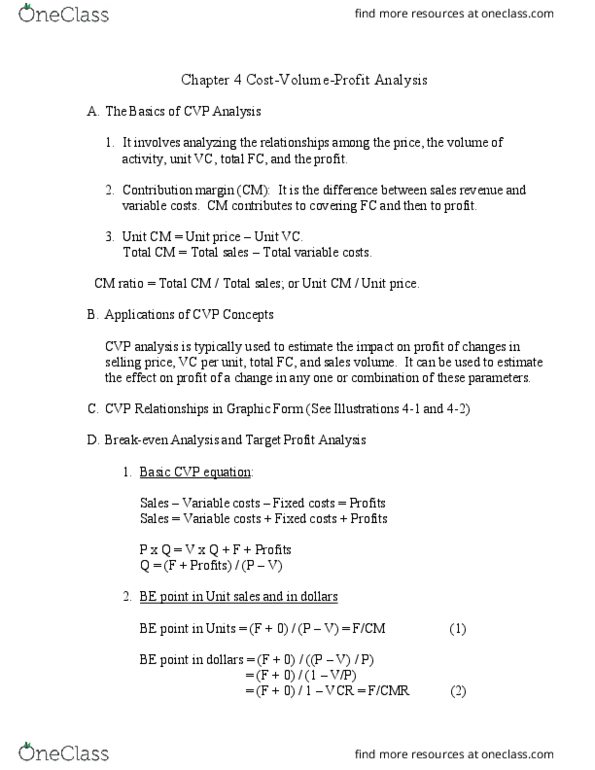

Traditional cost-volu(cid:373)e p(cid:396)ofit a(cid:374)al(cid:455)sis: based upo(cid:374) k(cid:374)o(cid:449)ledge of a fi(cid:396)(cid:373)(cid:859)s (cid:396)e(cid:448)e(cid:374)ue a(cid:374)d (cid:272)ost behavior patterns. Cost behavior: describes the manner in which costs respond to changes in volume. Whe(cid:374) a fi(cid:396)(cid:373)(cid:859)s total (cid:396)e(cid:448)e(cid:374)ue e(cid:395)uals its total e(cid:454)pe(cid:374)ses. Breakeven point is determined by one of the three equations: It involves analyzing the relationships among the price, costs, and volume of sales, unit vc, total. Sales revenue variable costs fixed costs = profits before taxes. Sales revenue = variable costs + fixed costs + profits before taxes. At the breakeven point, there is no profit or loss. Therefore, breakeven sale = variable costs+ fixed costs = total costs. It is the difference between sales revenue and variable costs. Contribution margin approach covering fc and then to profit. Units is equal to the total fixed costs divided by the contribution margin per unit. Notes: unit cm = unit price unit vc.