FINA 470 Chapter Notes - Chapter 2: Kpmg, Credit Risk, Financial Statement

24 Jan 2017

Department

Course

Professor

Document Summary

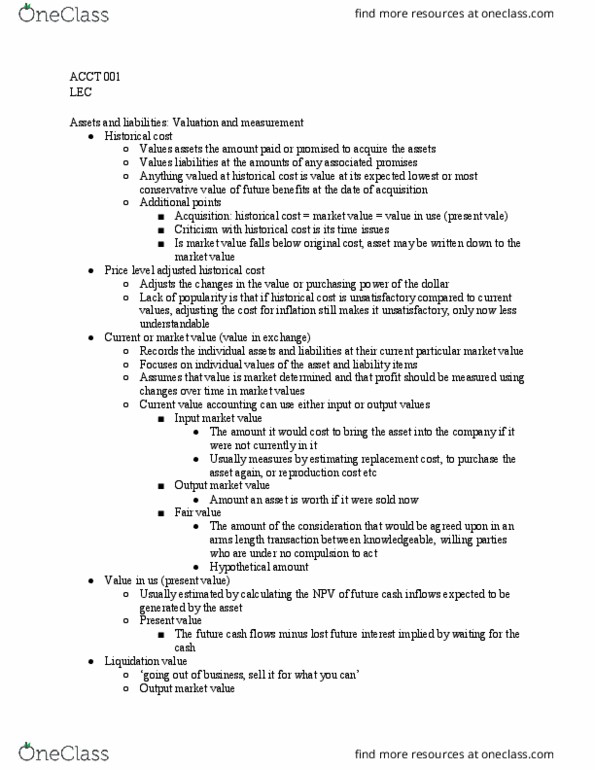

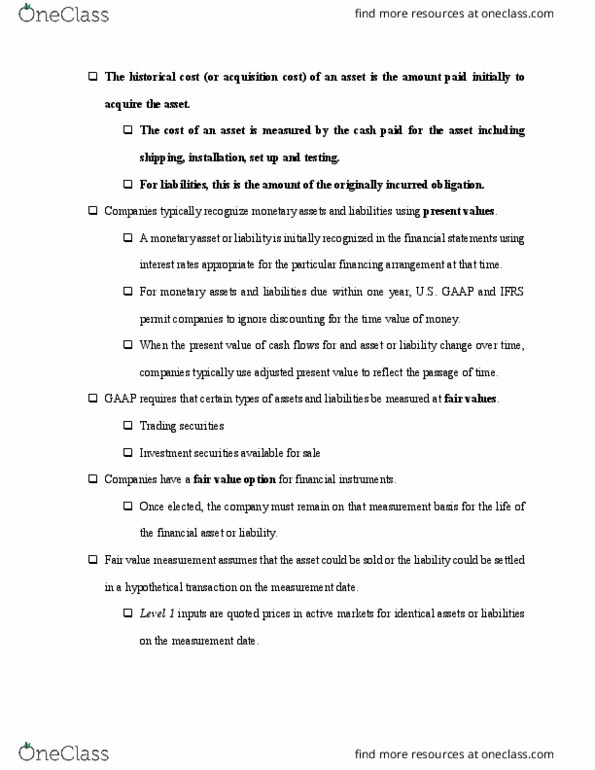

2-11 explain historical cost and fair value models of accounting. Under the historical cost model, asset and liability values are determined on the basis of prices obtained from actual transactions that have occurred in the past. Under the fair value accounting model, asset and liability values are determined on the basis of their fair values (typically market prices) on the measurement date (i. e. , approximately the date of the financial statements). Because of this the historical cost model has come under a lot of criticism for various quarters, resulting in the move toward fair value accounting. 2-15 describe at least four major limitations of financial statement information. First, financial statements are released well after the end of the quarter and/or fiscal year. Second, they are only released on a quarterly basis. Investors often have a need for information more often than just on a quarterly basis. Thus, financial statements are limited by the relative infrequency of their release.