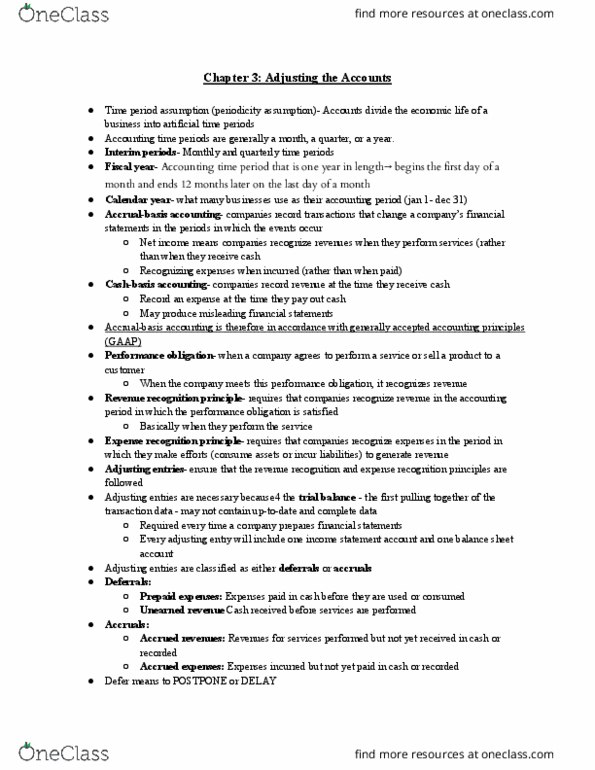

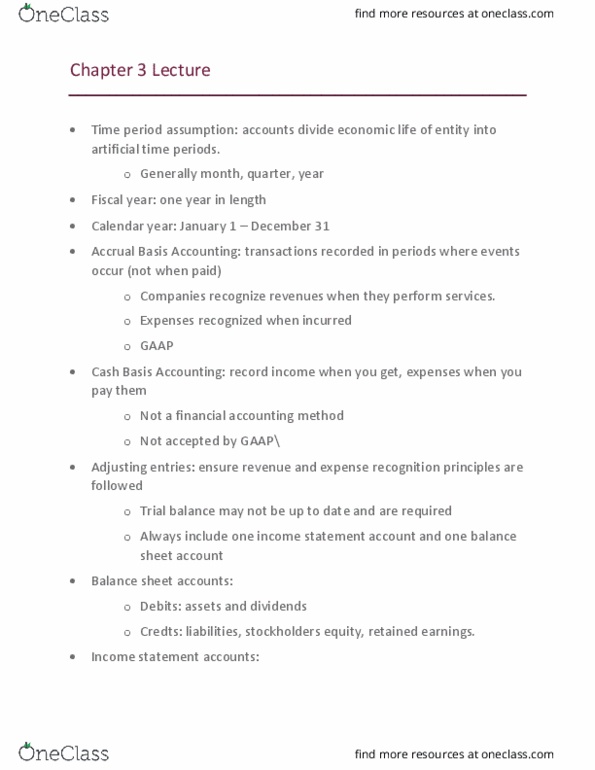

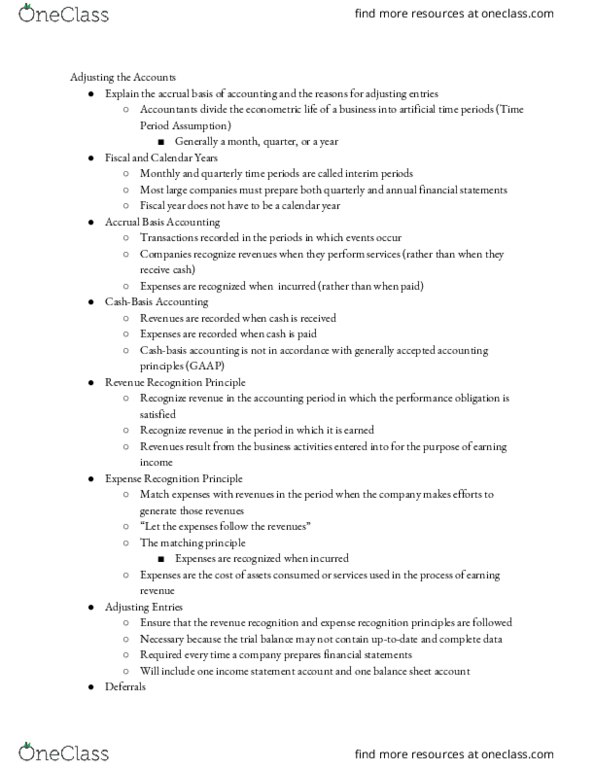

The following is a transcript of a video

This video explores the vital role of accounting in one of the world's largest firms. Aon is a reinsurance broker, insurance broker, and employee benefits consultant operating in more than 120 countries. Its goal of being the world's most responsive and client-focused insurance company means it must integrate thousands of professionals in hundreds of disciplines in many countries.

Many view accounting as a primary business language. It is of little use, however, unless you know how to "speak" it. Fortunately, the fundamentalsâthe accounting equation and the double-entry bookkeeping systemâare not difficult to learn.

0:01Clearly, in the financial world,

0:03if you want to be an effective accountant,

0:05you just can't be a numbers person.

0:07You also have to understand people.

0:09You need to know how to debate and hold your

0:11position on the arguments that you take.

0:14âªâª

0:34-Narr: You might not have heard of Aon.

0:36They've brokered deals between clients

0:38and more famous insurance companies.

0:40They often even insure

0:42those insurance companies.

0:45In fact, the only building taller than the

0:47Aon building in Chicago is the Sears Tower.

0:50With over 550 offices in 130 countries,

0:55there's a lot of money involved

0:56and a lot of numbers to keep straight.

0:58So who does all that math?

1:00Well, that's easy.

1:01The pencil pushers, the number crunchers,

1:03bean counters, right?

1:05Accountants are traditionally thought of as

1:07humorless people who type into

1:09pocket calculators all day.

1:11Nothing could be farther from the truth.

1:13Accountants are actually some of the most

1:15important and influential people in business,

1:18and Joe Prochaska is probably

1:20the most important accountant at Aon.

1:23Accounting is the process of recording,

1:25categorizing and interpreting financial

1:28transactions, but there are more creative

1:30aspects to accounting than mere bookkeeping.

1:32That's why Joe is usually smiling.

1:35-Oh, yeah, and my staff is learning to smile.

1:37It's very rarely that they see

1:39me frown, okay, but there are

1:40different kinds of smiles.

1:42-At Aon, managerial accountants interpret

1:46financial data for a company's internal use.

1:49Financial accountants such as CPAs summarize

1:52that information for outside parties

1:54like potential investors.

1:56At the end of the year, Joe uses

1:58a tax accountant to assure that

2:00Aon is in full compliance with

2:02changing tax laws, and to assure that Aon is

2:05taking advantage of the best tax strategies.

2:08But Joe gets the lion's share of the duties

2:10when it comes to Aon's financial information.

2:13-The role I play in the process of handling

2:16all these inputs is reviewing all the reports

2:20that come in so that when our management

2:22takes a look at those financial statements,

2:24they can have some assurance that they're

2:26looking at this as our shareholders will be

2:30looking at it when we

2:31present the information.

2:34-Did you know that every book

2:35you've ever read,

2:36every comic strip, poem and Web page,

2:39has its roots in accounting?

2:40That's because the earliest

2:42written languages were created

2:44to keep track of financial transactions.

2:46Every world culture engages

2:48in some form of trade,

2:49and Aon operates in most of those places.

2:53-The information we get

2:54on a monthly and a quarterly basis

2:56from our different operations around the globe

2:59is stated in a variety of currencies,

3:01yet Aon is a U.S.-based company that publishes

3:05its financials in U.S. dollars.

3:07There's a requirement for some assurance from

3:11a party outside the management

3:12of the company that you've done

3:15a fair job in presenting your financials,

3:17that they've been presented reasonably

3:20and in a consistent manner.

3:23-That's why the

3:24Financial Accounting Standards Board created

3:26the Generally Accepted Accounting Principles,

3:29to help everyone get on the same page

3:31with their accountant.

3:32The Generally Accepted Accounting Principles

3:34and the interpretation are one

3:36of my key functions at Aon.

3:38The Securities and Exchange Commission makes

3:41sure that companies stay on that page.

3:44-In its most adverse reaction,

3:46the SEC also is capable of doing

3:49what they would call an enforcement action.

3:52Many of you have heard of Enron,

3:53okay, and WorldCom.

3:56-The core of those principles is

3:58the six-step accountant cycle.

4:00Pretend you're on Joe's staff for a moment.

4:02First, a hundred different people

4:04send you transaction records

4:06from a dozen different departments.

4:08You collect and organize that pile of

4:10receipts, invoices, bank statements and

4:12purchase orders, account by account,

4:15into a book called a journal.

4:17Now divide all those

4:18transactions into purchases, sales,

4:21investments and so on, in a ledger.

4:24When that's done, do a trial balance

4:26to check your work.

4:28If it's off, go back and find the error.

4:31If it's okay, you can now begin

4:33the real task of accounting,

4:35reporting and analysis.

4:36-The mechanics of doing the accounting,

4:39that doesn't excite me too much.

4:41But going through the philosophy

4:42of what you're trying to accomplish

4:44and how you match revenue and expenses,

4:47which is really the underlying philosophy behind

4:50Generally Accepted Accounting Principles,

4:52to make sure when you recognize the revenue,

4:54you recognize the proportion of the expense.

4:57There's a lot of judgment and

4:58interpretation of what goes into

4:59an individual company in doing that.

5:05The two most basic reports you'll do are the

5:07balance sheet and income statement.

5:10The balance sheet contains the

5:12fundamental accounting equation.

5:14Assets are all the things Aon owns,

5:16like furniture and investments.

5:18Liabilities are how much the company owes

5:21others in the form of loans,

5:22bonds or unpaid bills.

5:24Equity is a little trickier to understand.

5:27Say that Aon owns $100,000, although we can

5:30pretty much guarantee they made a lot more.

5:33If they owe $70,000 in bills and loans to

5:36run the business, the $30,000 difference

5:39is called owners' equity.

5:42That's the amount of actual value

5:43that Aon's stockholders divide up

5:45between them to see how much their

5:47investment is worth at the moment.

5:49The income statement covers a specific period

5:52such as a quarter or year.

5:53It starts with revenue, which is all

5:56of Aon's earnings for the period,

5:58including sales, licensing fees

6:00and gains on investments.

6:02By subtracting the cost of goods sold,

6:04which is the amount of money applied

6:06to producing and distributing a product,

6:09you come up with a gross margin,

6:11or the profit and loss for the period.

6:18Okay, we've been throwing a lot of terms

6:20around, so let's take a break and learn a

6:22little bit more about what Aon does.

6:25One particularly interesting service

6:27has to do with extreme weather.

6:28-For instance, we do catastrophe modeling

6:32for hurricanes so that some of our insurance

6:35clients that may insure a whole lot

6:36of homes along the Gulf Coast to Florida

6:39what happens if a certain hurricane comes?

6:41What type of insurance or reinsurance

6:43protections do they need to make sure

6:46that they're still financially solvent

6:47if a big wind blows and takes out a

6:49lot of their clients' homes?

6:53In addition to that,

6:54one of the things that we innovated,

6:55we were one of the first people

6:56to provide a terrorism model.

7:00And you may be aware that Aon lost

7:02its major operations in New York,

7:04and we lost 175 of our associates

7:06in the World Trade Center disaster.

7:08That certainly spurred us into taking a look

7:11at what can we do to help companies manage

7:14and monitor their exposure to terrorism acts,

7:18and we've done a - have a strategic

7:20partnership with Rudy Giuliani and his group

7:23to try and help companies

7:25prevent and prepare for

7:27if a disaster like that would ever occur again.

7:34Okay, back to the income statement.

7:37Subtract the operating expenses of the company

7:39- that's salaries, electricity and stuff -

7:42from the gross margin to reveal

7:44net income before taxes.

7:46Then, obviously, subtract the taxes,

7:48and you get Aon's net income or net loss.

7:52That figure is what's known as

7:53the bottom line.

7:54If these two reports seem similar,

7:58just remember that the balance sheet is

8:00like a snapshot of the business at any

8:02particular moment, while the income statement

8:05is more like a movie of the company's

8:07performance over a certain period of time.

8:09Now you're at the final and most important

8:12step of the accounting cycle, analysis.

8:15A good example of analysis is budgeting,

8:18which looks at Aon's history to

8:19find ideas for the future.

8:22The budgeting and the planning process

8:23help us analyze and understand that

8:25and create a consensus among management

8:28of what are reasonable expectations

8:30for the coming years,

8:32and it also helps us to give some guidance to

8:34our shareholders on what they should expect

8:36for earnings from our company, which then

8:39I think also helps give people guidance

8:41on what reasonable valuations of our

8:43companies are for our shares.

8:45There are a host of other analyses

8:47you can do, financial ratios

8:49and activity ratios and liquidity tests.

8:52Of course, you don't have to do

8:53all of this math in your head; these days,

8:56most of it can be done by computer software.

8:58I can't think of anybody in our

9:01financial shop that doesn't have a computer

9:03on their desk, and I'm probably one of the

9:04biggest dinosaurs in that I can read all these

9:07financial reports and I can manipulate them,

9:09but I'm too far away from them

9:11to actually create them anymore.

9:13But clearly, the analysis and

9:15the financial reporting is definitely enhanced

9:18by the reporting tools that exist in computers.

9:22Well, your first day as an

9:23accountant went pretty well.

9:25You made a few decisions and learned a little

9:27about how Aon functions financially.

9:29If you're interested in learning more about

9:31accounting as a career,

9:32talk to your instructor.

9:34On the other hand, if accounting isn't for you,

9:36don't worry; your day hasn't been wasted.

9:39Understanding and applying the

9:41basic fundamentals of accounting is a skill that

9:43will help you in almost any

9:45business endeavor you pursue.

9:47Clearly, if you want to do

9:48anything in business - and I am biased,

9:51but there is no better foundation than

9:53having an accounting background,

9:55because that's how businesses are

9:57measured at the end of the day, and the

10:00intrepretation of those numbers are critical.

Question:

The value of the owners' interests is the same as

short-term liabilities.

equity.

revenue minus costs.

liabilities minus assets.

profits plus revenue.