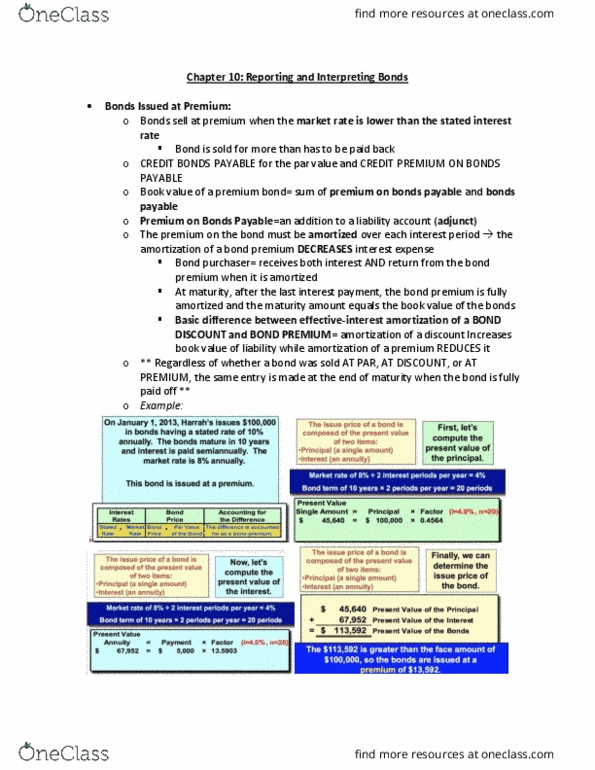

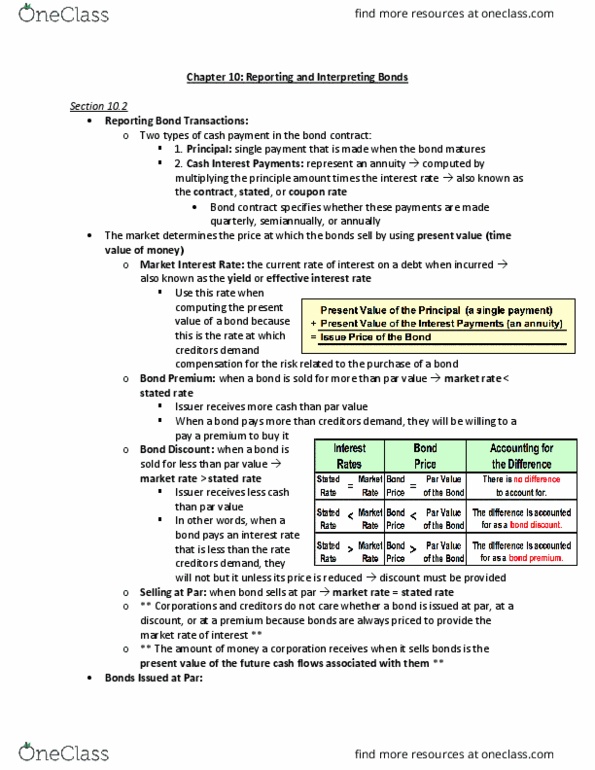

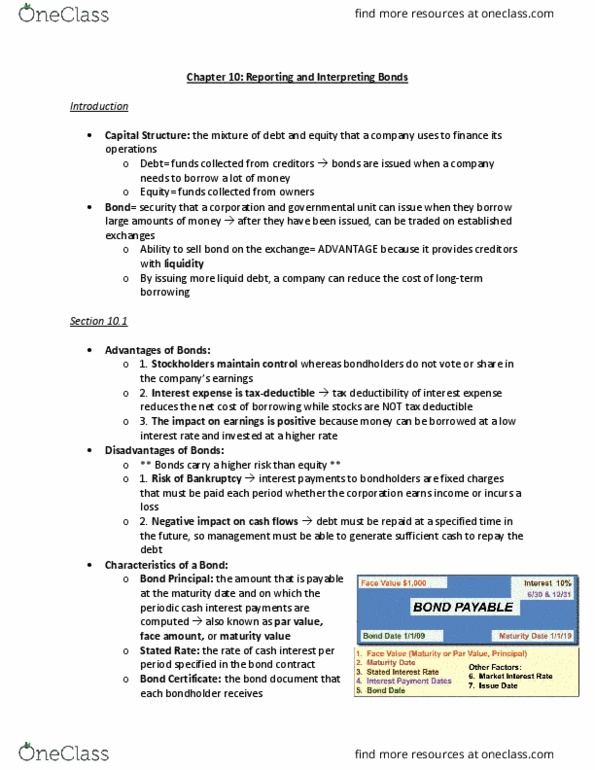

ACCT20100 Chapter Notes - Chapter 10.1: Balance Sheet

Document Summary

Bonds issued at discount: bonds sell at a discount when the market rate is higher than the stated rate of interest, when a bond is sold at a discount: Debit discount on bonds payable contra-liability account. Extra cash that must be paid = adjustment of interest expense to ensure that creditors earn market rate. To adjust interest expense, the borrower amortizes the bond discount to each interest period as an increase in interest expense. Credit bond discount and cash: example, amortization methods used: Straight line: easier, but cannot be used under gaap. A simplified method of amortizing a bond discount or premium that allocates an equal dollar amount to each interest period. Have the same journal entry for the specified time period until the balance of the discount gets to 0. Effective interest: at any point in time, calculate interest based on the book value of the bond.