ACCT20100 Chapter Notes - Chapter 8: Ddb Worldwide

Document Summary

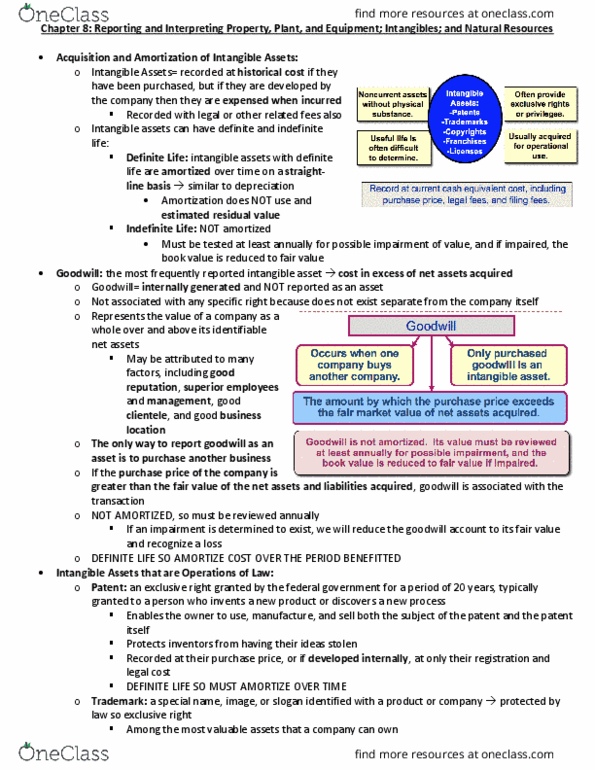

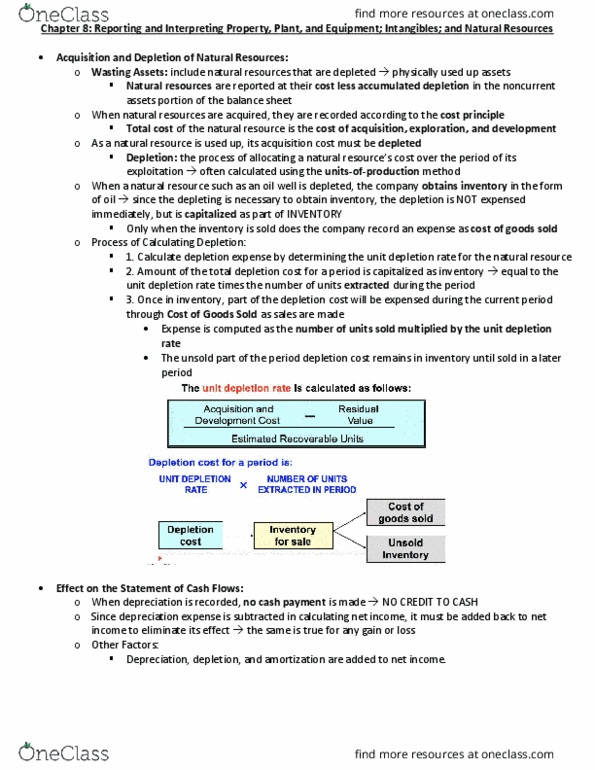

Chapter 8: reporting and interpreting property, plant, and equipment; intangibles; and natural resources. Straight-line method most common (98% of companies use this: 2. Depreciation expense is constant amount each year. Accumulated depreciation increases by an equal amount each year. Net book value decreases by the same amount each year until it equals the estimated residual value. As a result, also known as accelerated depreciation: two-step process: Calculate the double-declining-balance depreciation rate by dividing 2 by the useful life in years. Determine depreciation expense by multiplying the double-declining-(cid:271)ala(cid:374)(cid:272)e (cid:396)ate ti(cid:373)es the asset"s beginning-of-the-period book value: rate= two times the straight-line rate and is termed the double-declining balance rate. If straight-line rate= 10% for 10 year estimated life, then the declining-balance rate is 20%. Equation includes accumulated depreciation, not residual value. Net book value should not be depreciated below the residual value.