ACCT 2101 Chapter 13: 13_Planning for Capital Investments

Document Summary

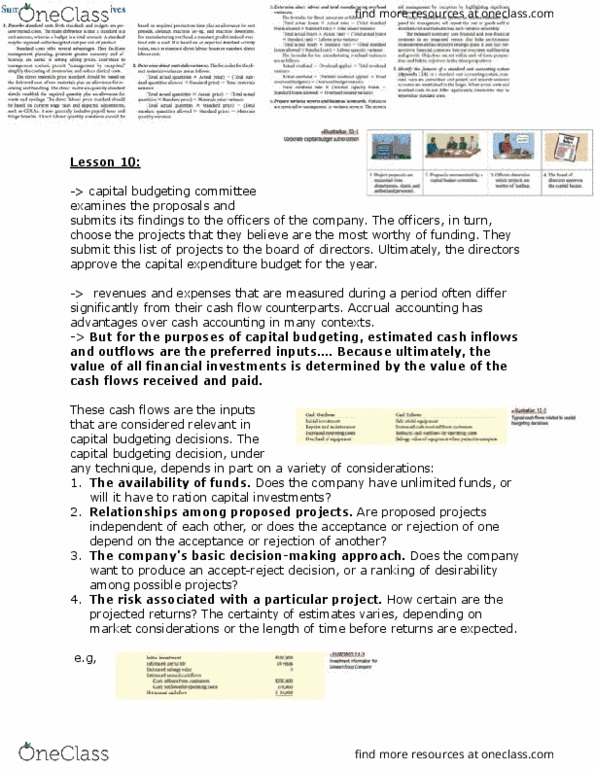

Module 13 covers chapter 12 of the textbook. While accrual accounting has advantages over cash accounting in many contexts, for purposes of capital budgeting, estimated cash inflows and outflows are preferred for inputs into the capital budgeting decision tools. Sometimes cash flow information is not available, in which case adjustments can be made to accrual accounting numbers to estimate cash flows. The capital budgeting decision, under any technique, depends in part on a variety of considerations. For example, the availability of funds, relationships among proposed projects, the company"s basic decision-making approach, and the risk associated with a particular project. The cash payback technique identifies the time period required to recover the cost of the capital investment from the net annual cash inflow produced by the investment. The formula for computing the cash payback period is: Cost of capital investment net annual cash flow* = cash payback period.