BUS-F 446 Chapter Notes - Chapter 11: Weighted Arithmetic Mean, Expected Return, Credit Risk

Document Summary

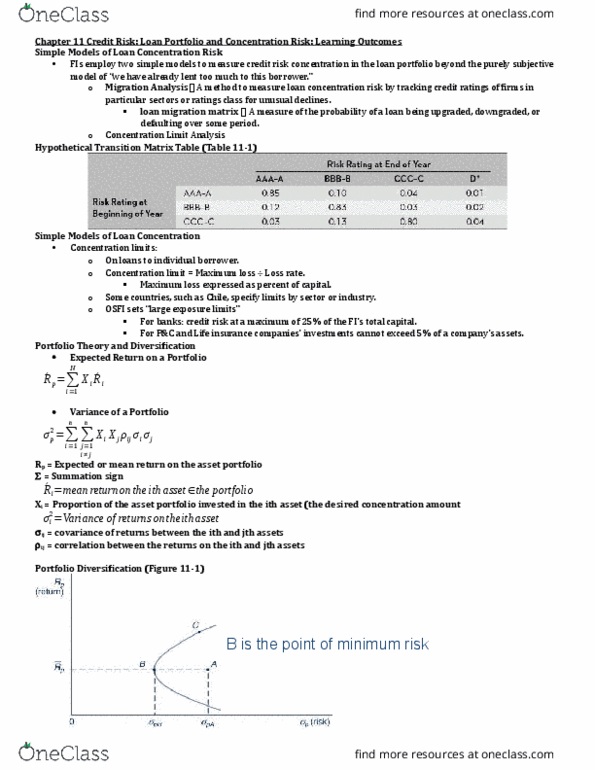

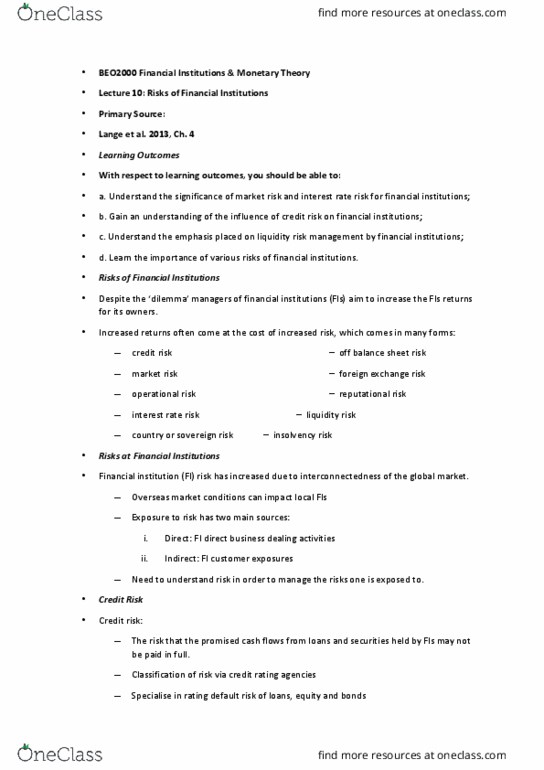

This chapter looks at credit risk from a portfolio perspective. Three concepts will be covered; they"re new innovations in the field. Integral part of credit metrics, developed by jp morgan, it"s a risk management package that"s the most common. Uses probability transition matrices showing the risk grade at the beginning and end of the year, and what value is used for a default. Banks are concerned about too much concentration of loans in a certain industry, etc. Banks have restrictions on the amount of loans that can be made to a certain sector, etc. Concentration limit: equals the maximum loss over the loss rate. The remainder would go into t-bills or something like that. Predicting loss rates per sector or as a whole: %loss in sector = b0 + b1 (%loss in total loans) Correlation between them: return will be the weighted average of the original returns, must sum up to 1, standard deviation: