ECON 103 Chapter Notes - Chapter 3: Shortage, Overproduction, Opportunity Cost

9 Jan 2017

School

Department

Course

Professor

Document Summary

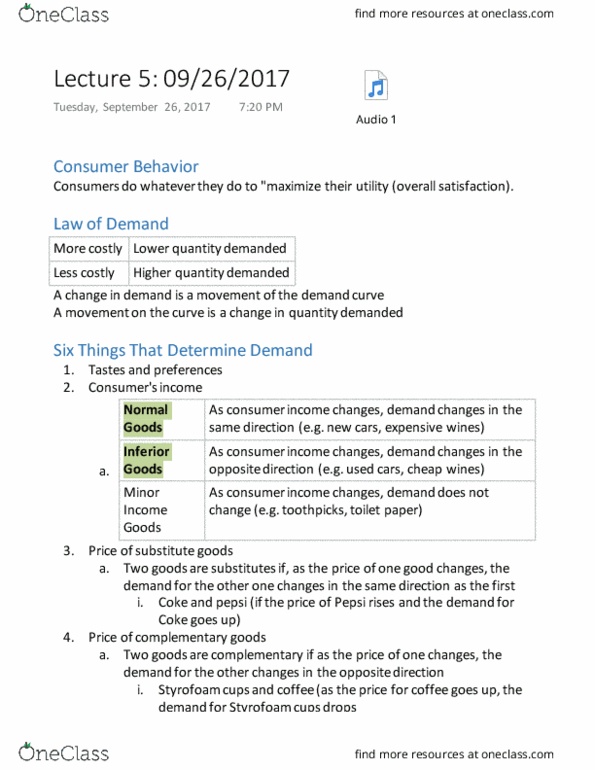

Chapter 3: demand, supply, and the market process. As the price of a good increases, we must give up more of other goods if we want to buy it. Thus, as the price of a good rises, its opportunity cost rises (in terms of goods foregone to purchase it) This principle underlies the law of demand: The law of demand states that there is an inverse (or negative) relationship between the price of a good or service and the quantity of it that consumers are willing to purchase. Price and quantity move in opposite directions - as price increases, buyers are willing to buy less of a given good, and as price decreases, consumers buy more. The availability of substitutes - goods that perform similar functions - helps explain this relationship. No good is absolutely essential - when the price of a good rises, consumers buy less of it and turn to substitutes.