ACG-2071 Chapter 3: Chapter 3

Document Summary

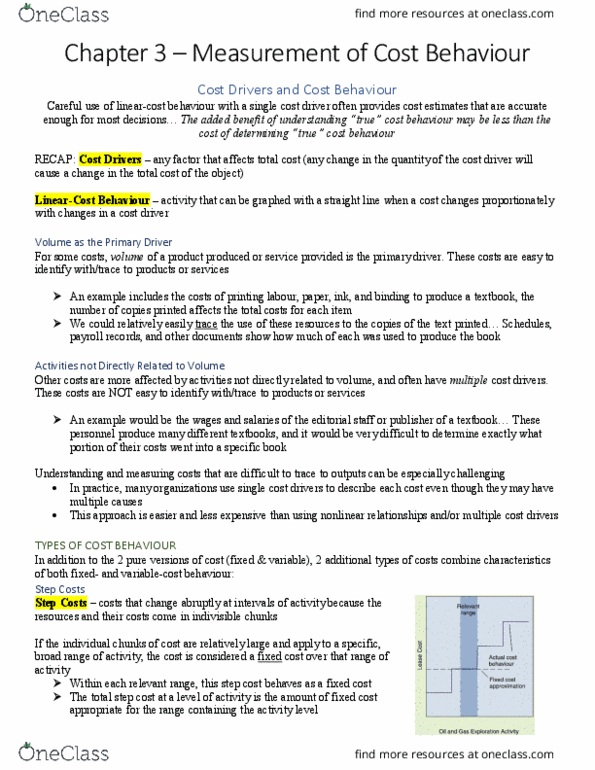

Chapter 3: measurement of cost behavior1/24/2011 11:21:00 pm. Understanding and quantifying how activities of an organization affect levels of costs. Mixed costs: mixed costs contain elements of both fixed and variable-cost behavior. The fixed-cost element is unchanged over a range of cost-driver activity. Managers influence cost behavior through choices of: process and product design, quality levels. The fixed costs of being able to achieve a desired level of production or to provided a desired level of service while maintaining product or service attributes, such as quality. Usually arise from the possession of facilities, equipment, and a basic organization. They have no obvious relationship to levels of output activity but are determined as part of periodic planning process. Examples: advertising and promotion, employee training, research and development, management salaries. First step: measure cost behavior as a function of appropriate cost drivers. Second step: figure the estimated cost driver activity.