ACCT 211 Chapter 4: Chapter 4: Accrual Accounting and Adjusting Entries

15 Mar 2017

School

Department

Course

Professor

Document Summary

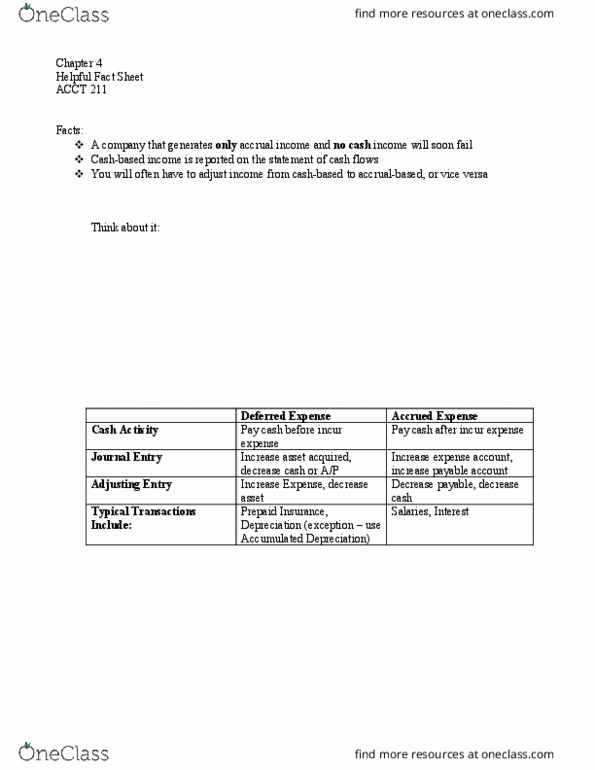

Application of the revenue recognition and matching principles: revenues such as job wages are recorded when earned, regardless of when payment is received. Ii. cash based income is normal greater than accrual based income. Adjusting journal entries: made in the general journal to record revenues that have been earned but not recorded and expenses that have been incurred but not recorded. The company has no yet provided the promised service and therefore can"t record a revenue in its accounting system. Instead, it must record a liability: subscription revenue an example of deferred revenue adjustment is a company that sells 12-month subscriptions to its monthly magazine. On oct 1, the company receives a total of. When a company receives cash before it provides a service, the company should always increase a liability account for the amount received as the company provides the service, the liability account decreases and the related revenue account increases.