ADMS 3595 Chapter Notes - Chapter 17: Dividend, Shares Outstanding, Capital Structure

10 Mar 2018

School

Department

Course

Professor

Document Summary

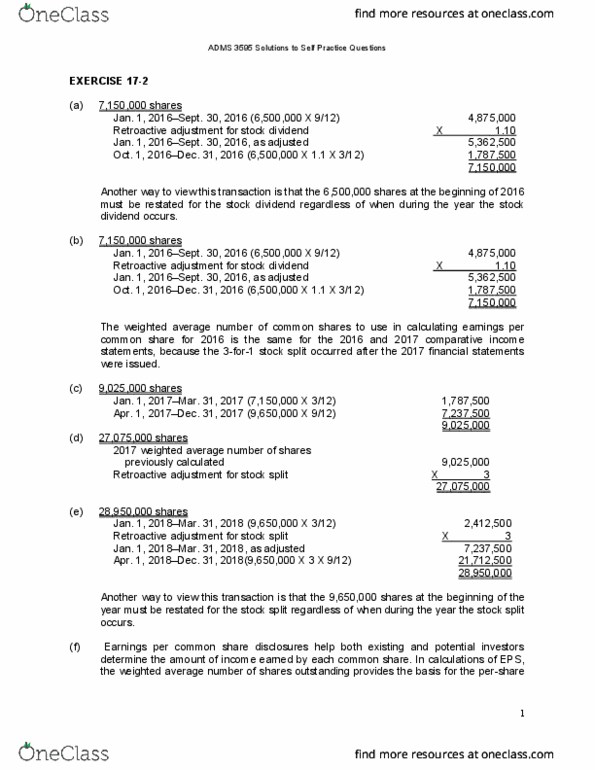

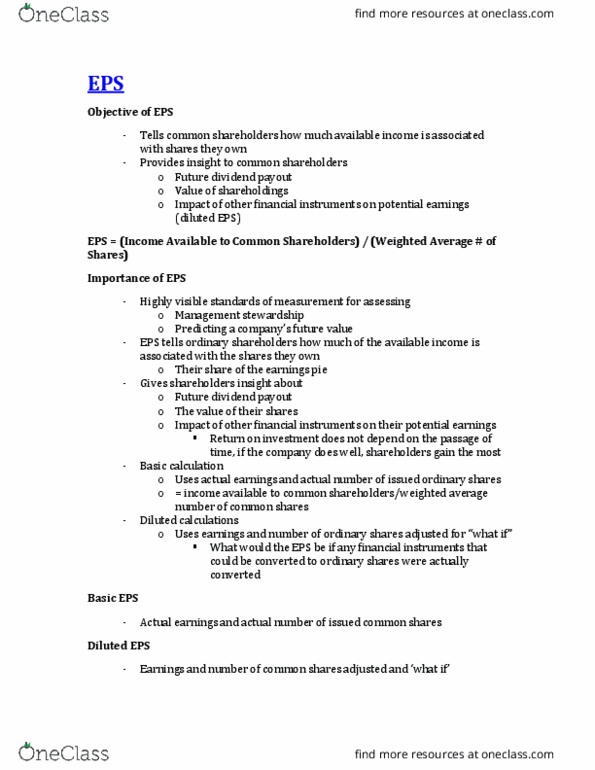

If there is discontinued operation display eps for: continued operations/ discontinued operations/ net income. Illustration 17-2 p. 1046: eps for discontinued presented on face of fs or notes, help understand impact of income from continuing operations on eps if capital structure complex, eps include both basic & diluted eps. Ifrs requires: eps amounts shown for all periods presented. If stock dividend/split all per share amounts of prior period earnings restated using new # of outstanding shares. Income available to common shareholders ni less amounts set aside to cover obligations (preferred shares, rank higher than common) In reporting eps arrive at income available to cs by subtracting pd(preferred) from. If preferred dividends declared & net loss occurs preferred dividend increases the loss in calculating loss per share. If cumulative dividends in arrears included in previous, not current: ex. P. 1050-1051: shares outstanding before stock dividend restated, so that on same basis as shares issued after stock dividend.