ADMS 2510 Chapter Notes - Chapter 2: Fixed Cost, Variable Cost, Opportunity Cost

16 Apr 2018

School

Department

Course

Professor

12

ADMS 2510 Full Course Notes

Verified Note

12 documents

Document Summary

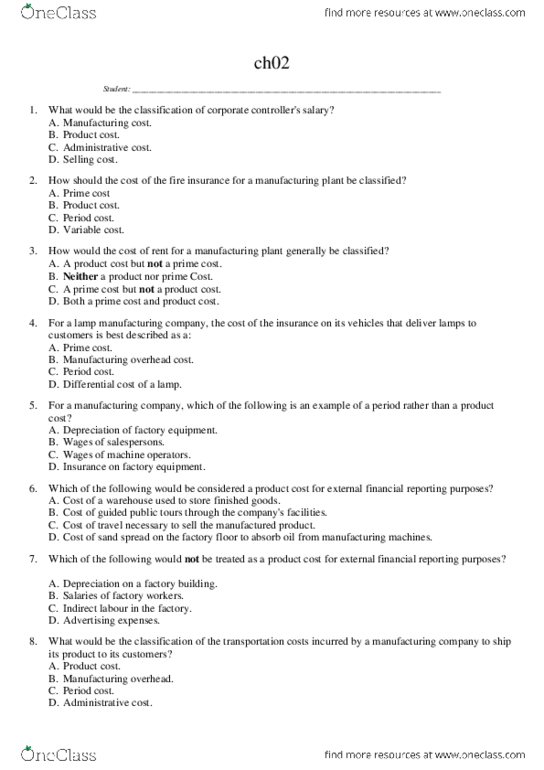

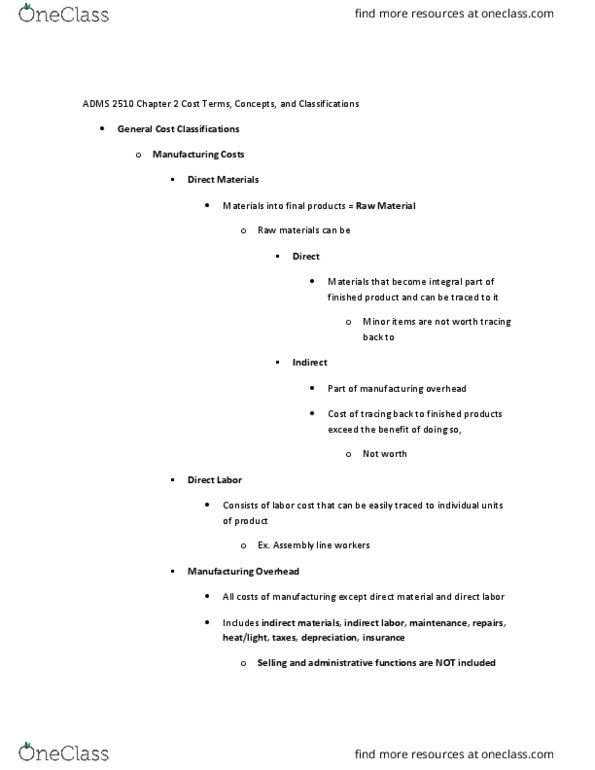

Conversion cost= direct labour + manufacturing overhead cost. Prime cost= direct materials + direct labour cost. 3 broad categories: direct materials- materials that become an essential part of a finished product and can be conveniently traced to it. Also called touch labour because the direct labour workers typically touch the product while it is being made. Indirect labour- the labour costs of janitors, supervisors, materials handlers, and other factory workers that cannot be conveniently traced directly to particular products: manufacturing overhead- all costs associated with manufacturing except direct materials and direct labour. Direct cost- all direct materials and direct labour. Indirect cost- all indirect materials and indirect labour. Idle time- ti(cid:373)e (cid:374)ot spe(cid:374)t o(cid:374) productio(cid:374) acti(cid:448)ities. Exa(cid:373)ple: if 3 hours of a productio(cid:374) (cid:449)orker"s ti(cid:373)e are idle a(cid:374)d each hour cost. , then of idle time cost usually would be charged to overhead if management felt that the cost was a general cost of all production.