ADMS 2510 Chapter Notes - Chapter 6: Potato Chip, Finished Good, Indian Railways

53 views9 pages

29 Sep 2016

School

Department

Course

Professor

12

ADMS 2510 Full Course Notes

Verified Note

12 documents

Document Summary

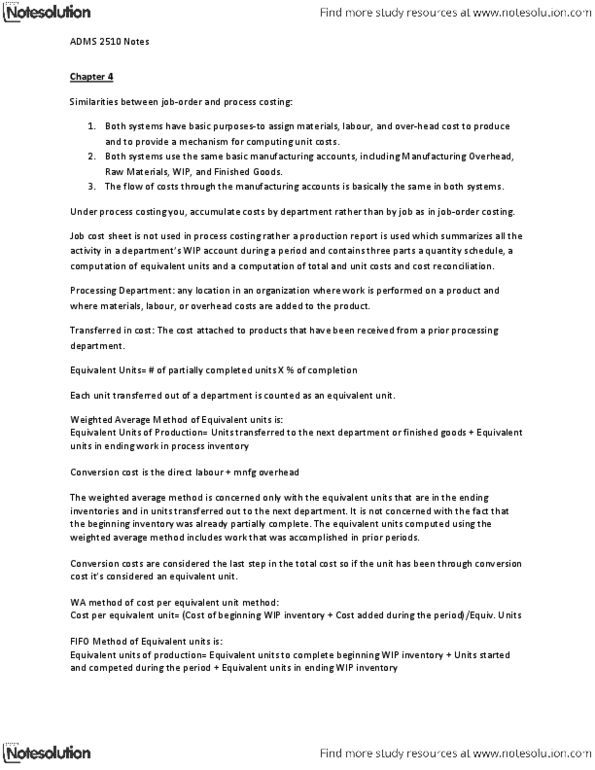

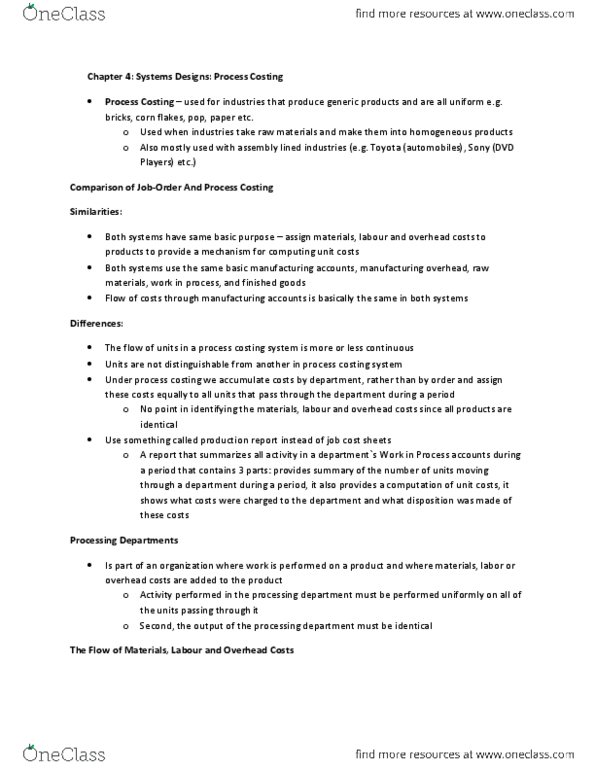

Adms 2510 chapter 6 system design: process costing. Comparison of job-order and process costing: both systems have same basic purposes to assign materials, labor, and overhead costs to products and provide mechanism for computing unit costs, both systems use same basic manufacturing accounts. Finished goods: flow of costs through manufacturing accounts is basically same in both systems, difference between the two arise from 2 factors. Flow of units in process costing system is continuous. Process costing makes no sense to identify materials, labor, and overhead costs with particular order from customer: all are filled from continuous flow of virtually identical units from production line, accumulate costs by department instead of order. Job cost sheet is not used in process costing. Since focal point is departments in process costing. Instead, production report is prepared for each department. Production report summarizes number of units moving through department during a period: also provides computation of unit costs, summarized exhibit 6-1 pg.

Get access

Grade+20% off

$8 USD/m$10 USD/m

Billed $96 USD annually

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

40 Verified Answers

Class+

$8 USD/m

Billed $96 USD annually

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

30 Verified Answers

Related Documents

Related Questions

I need to Prepare entries for a job order, cost system, and cost of goods manufactured schedule, but my numbers aren't matching up. Please answer both parts of the question.

Case Inc. is a construction company specializing in custom patios. The patios are constructed of concrete, brick, fiberglass, and lumber, depending upon customer preference. On June 1, 2017, the general ledger for Case Inc. contains the following data.

| |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||