ADMS 1000 Chapter -: Budget

7 Dec 2016

School

Department

Course

Professor

12

ADMS 1000 Full Course Notes

Verified Note

12 documents

Document Summary

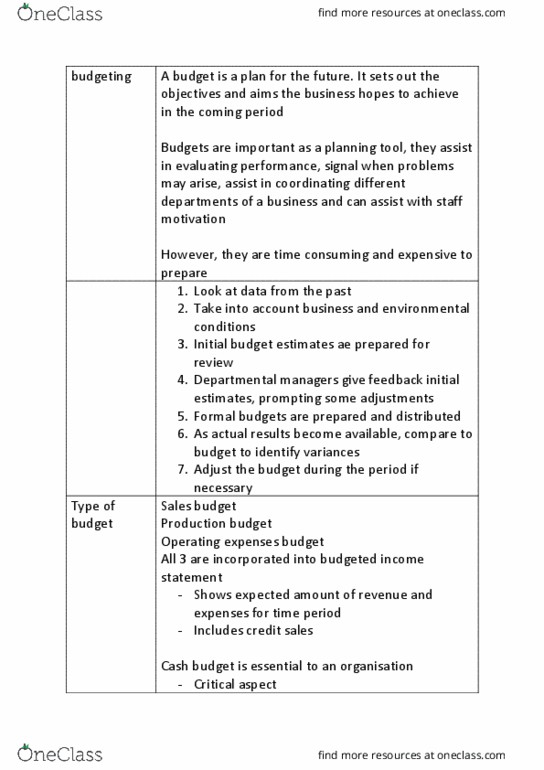

Budgets are quantitative plans, which take into account revenues and expenses for some period in the future mostly a year. The process of making budget is called budgeting and this process serves many functions in organizations. Planning tool: forces managers to look into the future and anticipate conditions and prepare for them. Control tool: once a budget is made, actual operations can be compared to the budget and any differences can be examined. Motivating tool: budgets set standards and if these are process involves many departments having to work together. challenging enough and people"s opinions have been taken into account, it is likely to motivate. Budgets as control tools: variance analysis: variances refer to the deviation of actual results from the budget. A favorable variance means that a business has received more revenue than budgeted or spent less money than budgeted (similarly for adverse). As can be seen that sales variance is adverse but the purchases variance if favorable.