EC120 Chapter Notes - Chapter 13: Sunk Costs, Marginal Cost, Marginal Product

30

EC120 Full Course Notes

Verified Note

30 documents

Document Summary

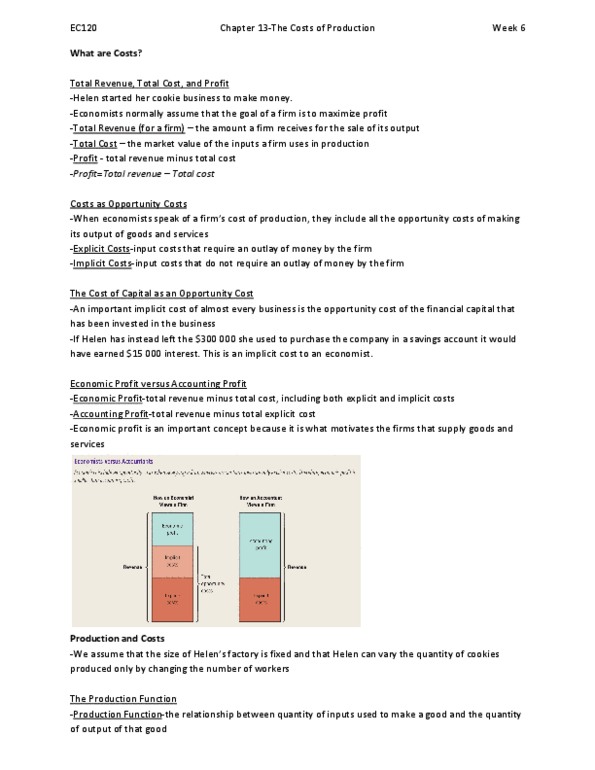

All costs can vary in the long-run. An example of explicit costs are the payments made by the firm to others. An example of implicit costs is the opportunity cost of resources owned by the firm. A firm"s economic profit is equal to the difference between its revenues and its opportunity costs. Variable cost in the short-run: a new wing on the plant (?) What best characterizes fixed costs is that they are costs that do not vary with output. Marginal cost is the increase in total cost that arises from an extra unit of production. Economies of scale explain why average cost declines in the long run. As production increases, a unit"s share of fixed costs continually decreases as output increases ( doesn"t it stay constant??) Average cost is best defined as tc / q. Marginal cost equals atc at its min. The marginal product is essentially the additional unit of output per unit of input.