BU487 Chapter 7: BU487 - Chapter 7 Textbook Notes

Document Summary

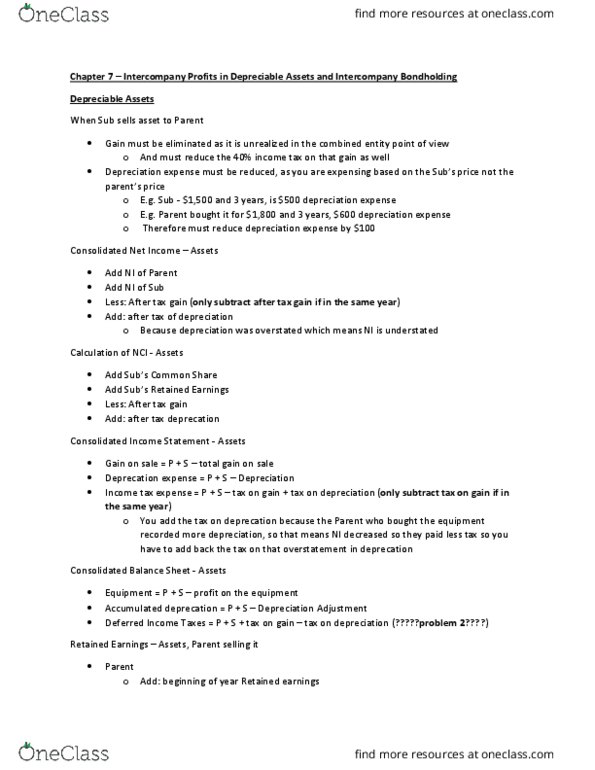

Chapter 7: (a) intercompany profits in depreciable assets (b) intercompany. This reduces before-tax income and holds back this profit. This reduces the income tax expense as well: depreciation on the gain must be eliminated; increases the before-tax income. Even though the equipment is not sold to outsiders, the products or services are sold to outsiders then no elimination. Intercompany profits on depreciable assets: gain is therefore realized over the life of the equipment; based on the consumption of the asset. Therefore, when recording the asset at fv, a gain/loss will always occur: elimination entries: Reduction of equipment removes the gain and restates the equipment to a) the historical cost to the entity. b) Note: the unrealized profit at the end of year 1 was realized in income for year 2. Intercompany sale of a used depreciable asset: sale of a used depreciable asset, that is, an asset with accumulated depreciation, example: original cost = k; carrying amt.