BU487 Chapter 4: Chapter 4 – Consolidation of Non-Wholly Owned Subsidiaries

Chapter 4 – Consolidation of Non-Wholly Owned Subsidiaries

Non-controlling interest (NCI) – represents additional set of owners who have legal claim to the

subsidiary’s net asset since you only bought a portion,

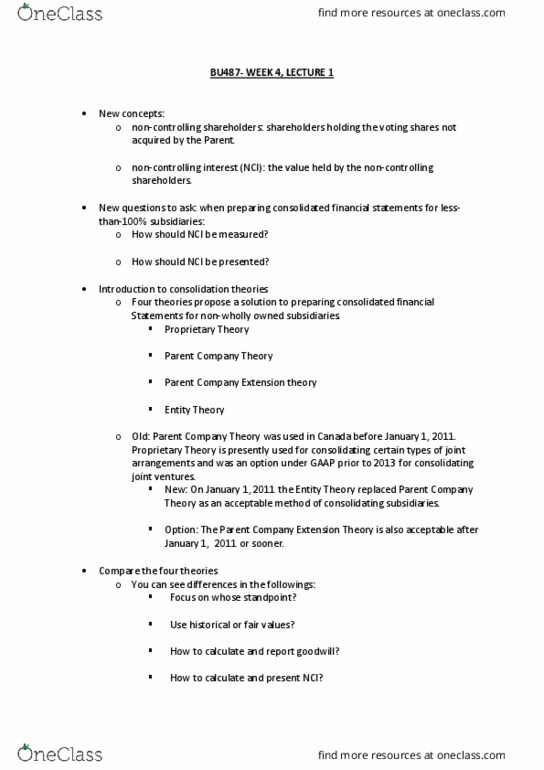

Four Theories on how to report

Proprietary Theory

Focus: the standpoint of the shareholders of the parent company

BV or FV: fair values of the parent’s portion of subsidiary’s identifiable net assets

Goodwill: parent’s portion of the full fair value of good will

NCI: No reflection

NOTES

oYou would multiple everything by the % you acquired or owned, you would not combine

everything together, just the % you owned, even for goodwill

Parent Company Theory

Focus: Both the controlling and non-controlling shareholders

BV or FV: full fair values of subsidiary’s identifiable net assets as if the parent had acquired 100%

Goodwill: Full fair value of goodwill as if the parent had acquired 100%

NCI: Reflected at the fair value based on the implied value, and reported as an equity

Parent Company Extension Theory – you only reflect on what you own

Focus: Both controlling and non-controlling shareholders

BV or FV: full fair values of subsidiary’s identifiable net assets as if the parent had acquired 100%

Goodwill: Parent’s portion of the full fair value of goodwill

oTotal goodwill * % acquired or owned

NCI: reflected at the fair value of the sub’s identifiable assets, and reported as an equity

oTotal NCI = implied value * % not acquired

oNCI under parent company extension = Total NCI * % acquired

NOTES

oYou would reflect NCI and Goodwill as the % you acquired/owned

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Chapter 4 consolidation of non-wholly owned subsidiaries. Non-controlling interest (nci) represents additional set of owners who have legal claim to the subsidiary"s net asset since you only bought a portion, Focus: the standpoint of the shareholders of the parent company. Bv or fv: fair values of the parent"s portion of subsidiary"s identifiable net assets. Goodwill: parent"s portion of the full fair value of good will. Notes: you would multiple everything by the % you acquired or owned, you would not combine everything together, just the % you owned, even for goodwill. Goodwill: full fair value of goodwill as if the parent had acquired 100% Nci: reflected at the fair value based on the implied value, and reported as an equity. Parent company extension theory you only reflect on what you own. Bv or fv: full fair values of subsidiary"s identifiable net assets as if the parent had acquired 100%