BU487 Chapter Notes - Chapter 1: Broad Group, Credit Union, Accrual

Chapter 1 – Conceptual and Case Analysis Frameworks for Financial Reporting

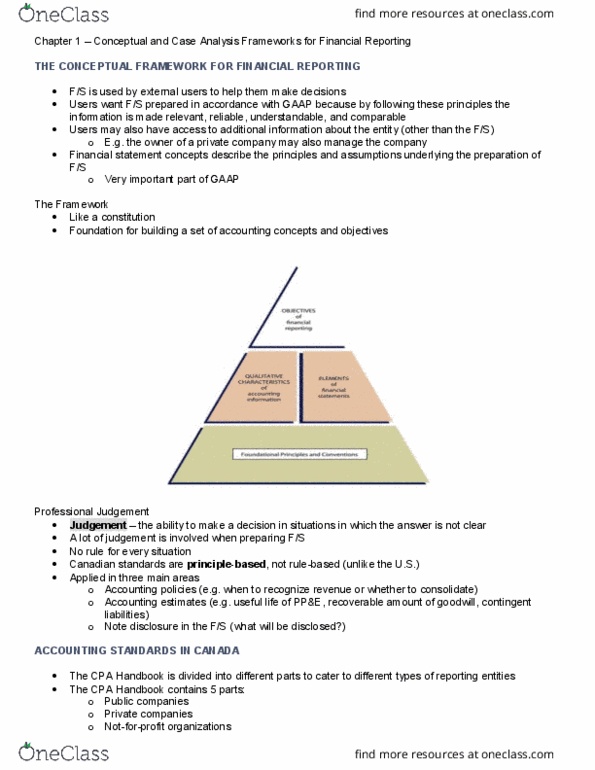

The Conceptual Framework for Financial Reporting

GAAP principles help make f/s information relevant, reliable, understandable, and comparable

Sometimes you would want non-GAAP based statements, e.g. lender may want to receive a b/s

with assets reported at FV rather than historical cost

If a new requirement is preferred by the preparer but not accepted by users, it is unlikely to

become part of GAAP

F/S should cater to the needs of the users

Financial statement concepts describes the principles and assumptions underlying the

preparation of f/s, are important parts of GAAP because they provide the framework for the

development and issuance of other financial accounting standards

oShould include:

Objective of general purpose financial reporting

Qualitative characteristics of useful financial information

Underlying assumptions

Definition, recognition, and measurement of the elements of f/s

Professional Judgement

Judgement – the ability to make a decision in situations in which the answer is not clear cut

Judgement needs to be applied in 3 main areas

o1.) accounting policies – such as when to recognize revenue, e.g. company selling to low

credit score customers, you would recognize revenue when cash is paid, but if you sell

to high credit score, then recognize revenue when goods are delivered

o2.) accounting estimates – e.g. what is the estimated useful life of property

o3.) deciding what to disclose and how – e.g. if you are being sued and thinking about if

you should show contingent liability, but you feel like the lawsuit has no merit

Accounting Standards in Canada

GAAP for Publicly Accountable Enterprise – IFRS

oPublicly accountable enterprise (PAE) – an entity other than a not for profit organization

or a government or another entity in the public section that

i.) has issued, or is the process of issuing, debt or equity instruments that are, or

will be, outstanding and traded in a public market or…

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Chapter 1 conceptual and case analysis frameworks for financial reporting. Gaap principles help make f/s information relevant, reliable, understandable, and comparable. Sometimes you would want non-gaap based statements, e. g. lender may want to receive a b/s with assets reported at fv rather than historical cost. If a new requirement is preferred by the preparer but not accepted by users, it is unlikely to become part of gaap. F/s should cater to the needs of the users. Financial statement concepts describes the principles and assumptions underlying the preparation of f/s, are important parts of gaap because they provide the framework for the development and issuance of other financial accounting standards: should include: Definition, recognition, and measurement of the elements of f/s. Judgement the ability to make a decision in situations in which the answer is not clear cut. Full differentiation would encompass two distinct sets of gaap.