BU393 Chapter Notes - Chapter 9: Cash Flow, Discount Window, Net Present Value

Document Summary

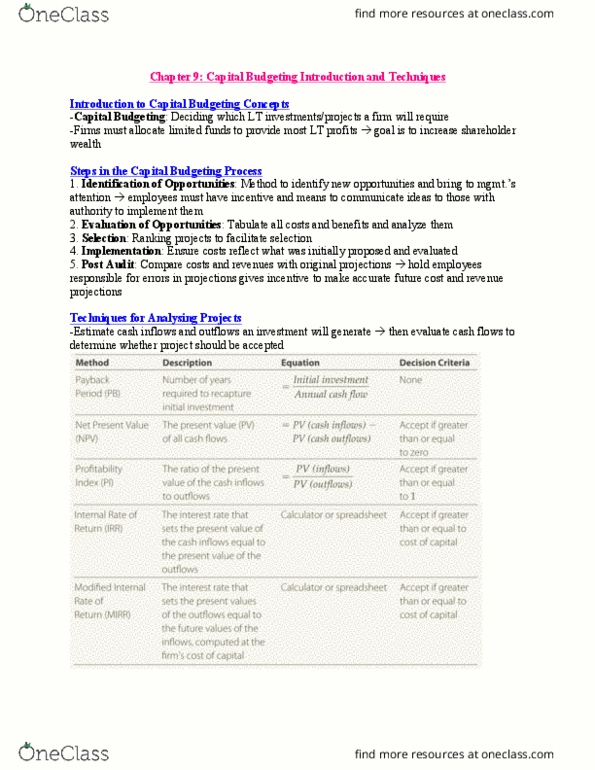

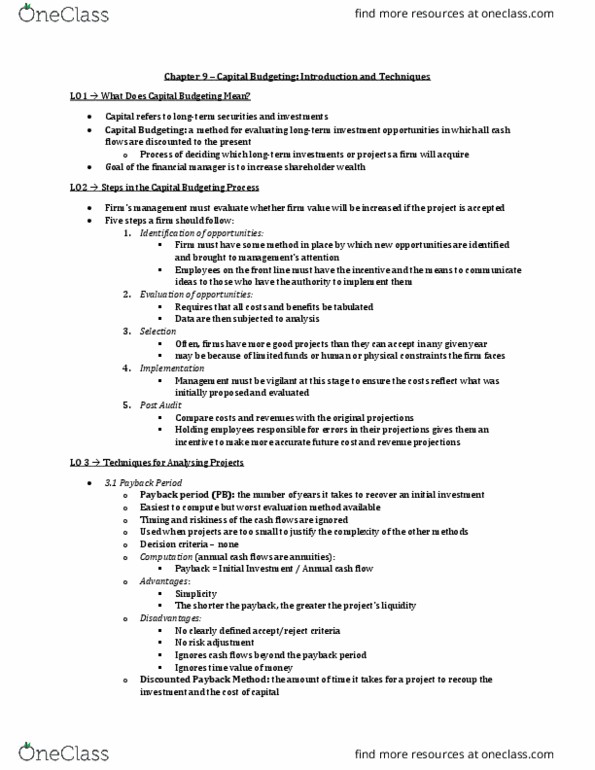

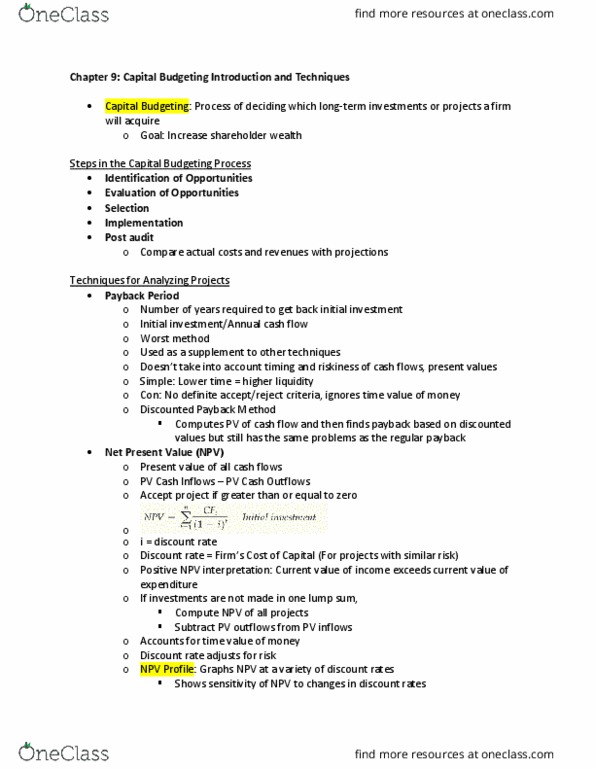

Not sure if important: capital long term securities and investments, capital budgeting: is the process of deciding which long-term investments or projects a firm will acquire. Most firms have more options than funding available. Payback period (pb): number of years it takes to recover an initial investment: worst evaluation method available. Initial investment / annual cash flow: advantage: simple. Shorter payback = higher liquidity: disadvantage, no defined accept/reject criteria, no risk adjustment, ignores cash flows beyond payback period, ignores tvm. Discounted payback method: the amount of time it takes for a project to recoup the investment (total) and the cost of capital. Net present value (npv): cash inflows - cash outflows: after conversion to present values if cash inflows>cash outflows = project is acceptable, discount rate = cost of capital, no discount for initial investment since paid at time 0. If paid over time, still needs to be discounted to 0 each period. +npv = acceptance: npv is not profit.