BU247 Chapter 4: BU 247 Chapter 4.3

Document Summary

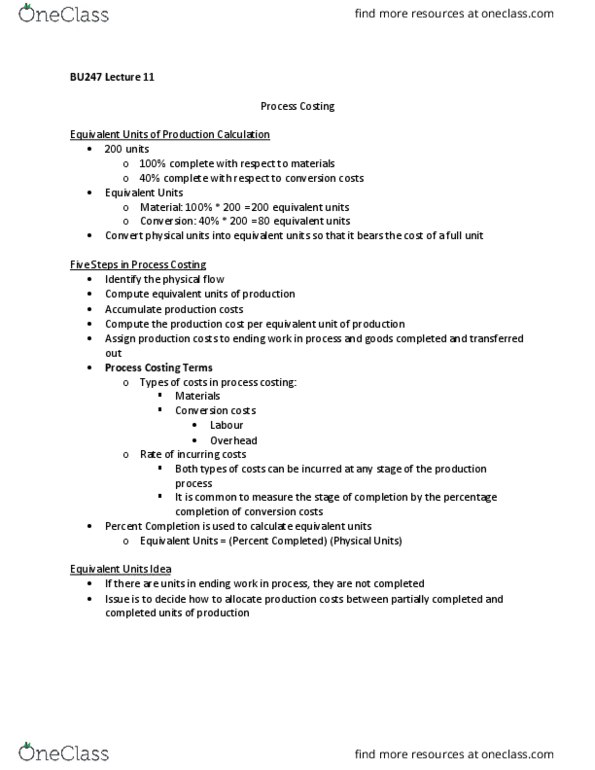

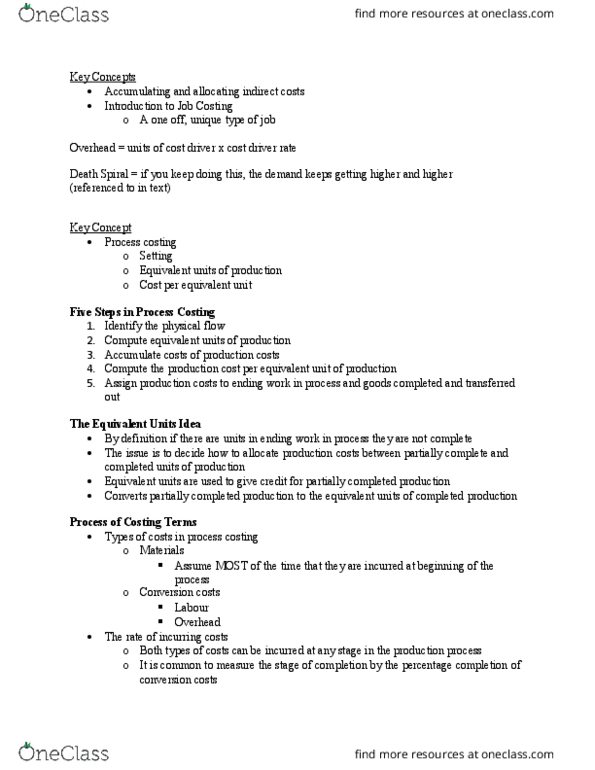

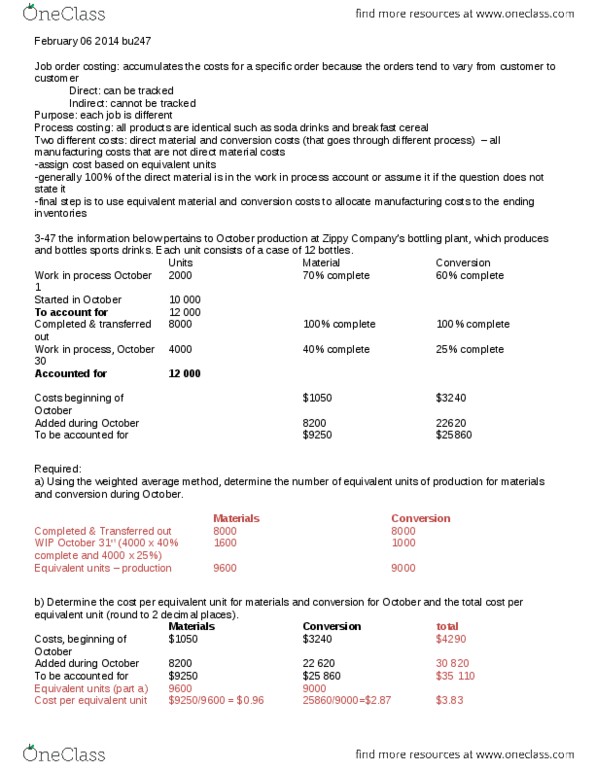

Is an approach to costing that is used when all products are identical. Found by adding up all direct and indirect costs to make the product and then dividing by the number of products made to get cost per unit. The focus is on computing the costs of the individual components of total costs. Examples are soda, cereal, and routine services such as a u shot. Focus on components of total product cost. Equivalent unit of production - in processing, calculated by multiplying the number of partially completed units by the percentage of competition. which is usually 10% Conversion costs - include all manufacturing costs that are not direct material costs. 1: compute the equivalent units of production, compute the cost per equivalent unit of production, allocate costs.