Management and Organizational Studies 3361A/B Chapter Notes - Chapter 20: Credit Risk, Interest Rate, Finance Lease

25 Apr 2018

School

Department

Professor

Document Summary

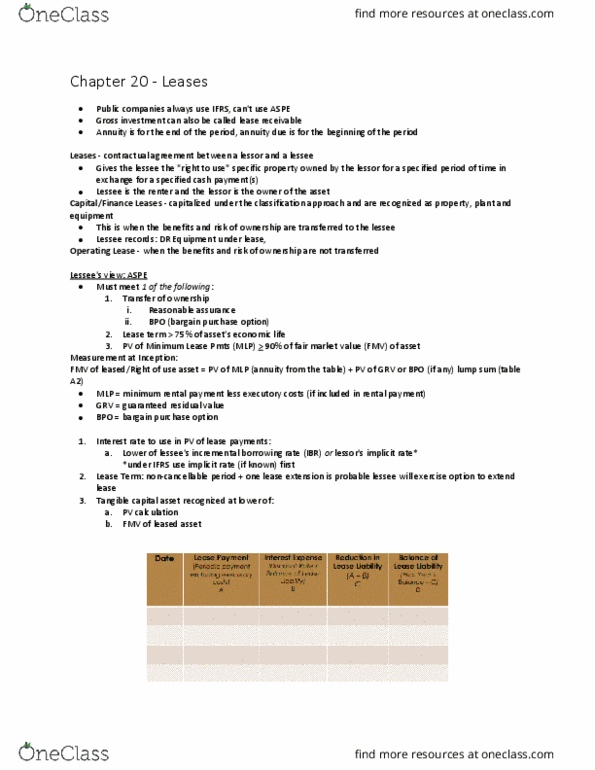

Ifrs 16: under ifrs 16, all leases are capitalized and placed on the balance sheet, exceptions are permitted only when, the lease is for a term of 12 months or less, the underlying asset is of low value. If a lease is not capitalized, the lessee recognizes the lease payments as an expense. If the criteria is not met, then the asset is not capitalized and it is classified as an operating lease. Minimum lease payments: minimum lease payment those payments that the lessee is obligated to make in connection with the leased property. If the residual value is guaranteed by the lessee, its pv is included in the leased asset and lease obligation recognized. In this instance, the leased asset is expected to be returned to the lessor so the lessee depreciates only the capitalized amount less the guaranteed residual amount of the period to the end of the lease.