Management and Organizational Studies 1023A/B Chapter Notes - Chapter 2: Financial Statement, Measurement Uncertainty, Quick Ratio

1 Sep 2018

School

Department

Professor

9

MOS 1023A/B Full Course Notes

Verified Note

9 documents

Document Summary

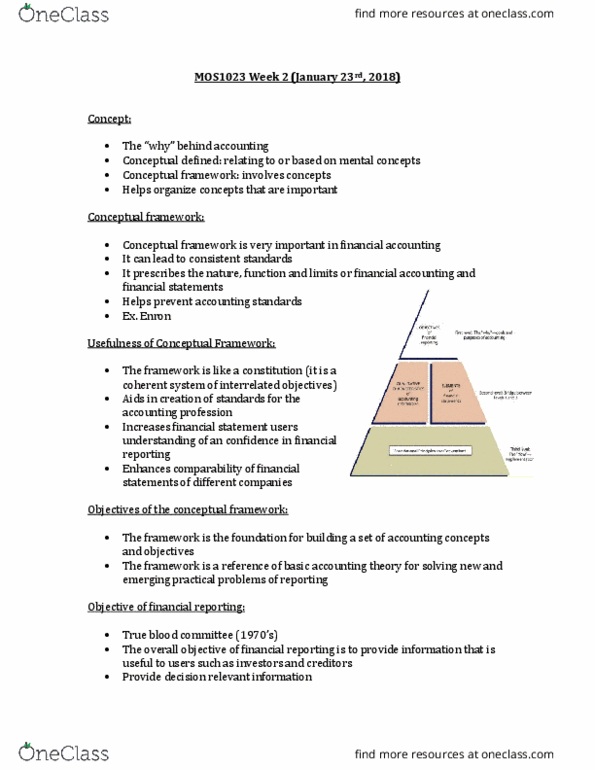

Objectives of financial reporting: first level: the (cid:494)why(cid:495) goals and purposes of accounting level. Adverse selection/moral hazard: problems may arise when certain stakeholders such as accountants and bankers have expert knowledge that the rest of the capital marketplace does. Equity: residual interest in an entity that remains after deducting its liabilities from it assets revenues: increases in economic resources resulting from ordinary activities. Expenses: decreases in economic resources resulting from ordinary revenue-generating activities. Foundational principles foundational principles help explain which, when, and how financial elements and events should be recognized/derecognized, measured, and presented/disclosed by the accounting system recognition/derecognition: Elements must be measurable to be recognized: therefore, we must, determine the level of uncertainty that is acceptable for recognition, use appropriate measurement tools, disclose sufficient information to indicate/describe the uncertainty artificial time periods reasonably possible amount. Measurement uncertainty: when there is a variance between the recognized amount and another.