Financial Modelling 2555A/B Chapter Notes - Chapter 1: Cash Flow, Investment, Profit Maximization

11 Oct 2016

School

Department

Professor

Document Summary

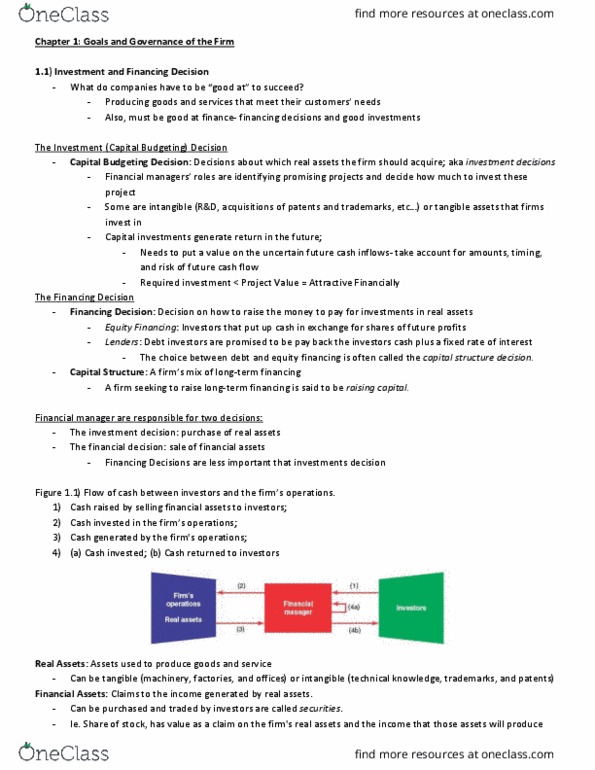

Real assets: tangible assets and intangible assets used to carry on business. Tangible assets: physical assets, such as plants, machinery, and offices. Intangible assets: nonmaterial asset such as technical expertise a trademark or a patent. Corporations pay for real assets by selling claims on them and on the cash flow they will generate. Manage and control the risks of its investments. Deciding when to shut down and dispose of assets if profits decline. Capital budgeting/ capital expenditure (capex): planned investment projects, usually prepared annually. Todays capital investments generate future cash returns. Meeting obligations to banks, bondholders, and stockholders that contributed financing in the past. Corporation can lend money from lenders or from shareholders. If it borrows, the lenders contribute the cash, and the corporation promises to pay back the debt plus a fixed rate of interest. Capital structure: mix of different securities issued by a firm. Capital structure decision refers to the choice between debt and equity financing.