Business Administration 2257 Chapter Notes - Chapter 6: Write-Off, Consignor, Perpetual Inventory

13 Oct 2015

School

Department

Professor

Document Summary

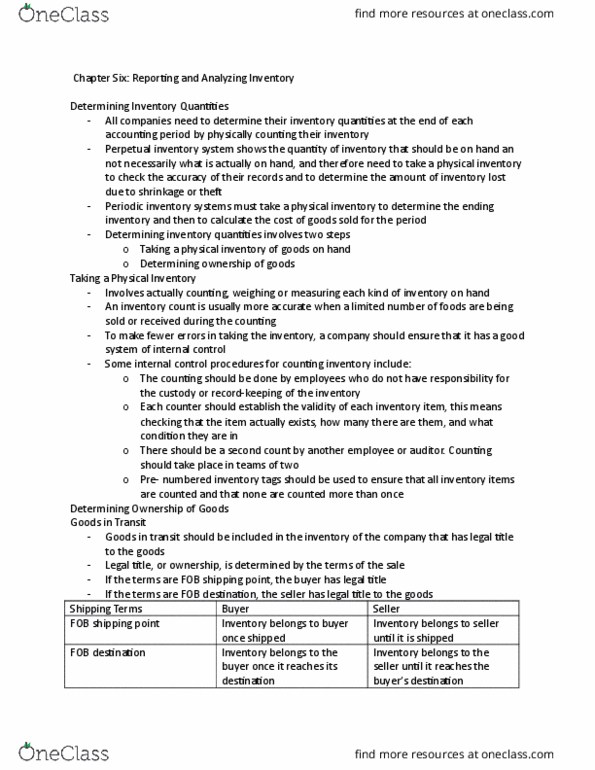

Determining inventory quantities: all companies need to determine inventory quantities @ end of accounting period by physically counting their inventory, determining inventory quantities involves 2 steps, taking physical inventory of goods on hand, determining ownership of goods. Goods in transit: should be included in inventory of company that has legal title to goods, determined by terms of sale. Inventory belongs to buyer once it reaches its destination. Inventory belongs to seller until it reaches buyer"s destination* Thursday, october 1, 2015: may allow management to manipulate profit. Presentation and analysis of inventory: presenting inventory appropriately is important b/c inventory is usually largest asset (merchandise inventory) and largest expense (cogs) on financial statements. < cost, inventory written down to net realizable value: net realizable value (nrv): selling price costs required to make goods ready for sale. If nrv < cost, adjust and report inventory at nrv rather than cost.