Business Administration 2257 Chapter Notes - Chapter 2: Deferral, Accounts Payable, Promissory Note

21 Sep 2016

School

Department

Professor

Document Summary

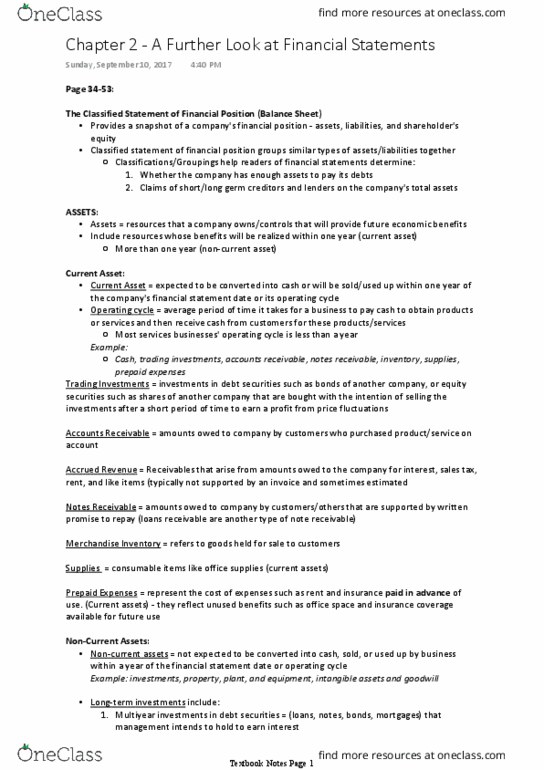

Chapter 2: a further look at financial statement. Assets that are expected to be converted into cash or will be sold or used up within one year of the company"s financial statement date/operating cycle. Operating cycle the average point of time it takes for a business to pay cash to obtain products or services and then receive cash from customers for these products or services: usually less than a year. Examples include cash, trading investments, accounts receivable, notes receivable, merchandise inventory, supplies, and prepaid expenses. Cash includes cash on hand or cash in bank/other financial institutions. Trading investments are investments in debt securities (e. g. bonds) that are bought with the intention of selling the investments after a short period of time in order to earn a profit from their price fluctuations o. Accounts receivable amounts owed to the company by customers who purchased products or services on credit (on account: are normally supported with an invoice.