Business Administration 1220E Chapter Notes - Chapter 2: Gross Income, Net Income, Income Statement

25 Dec 2016

School

Department

Professor

40

Business Administration 1220E Full Course Notes

Verified Note

40 documents

Document Summary

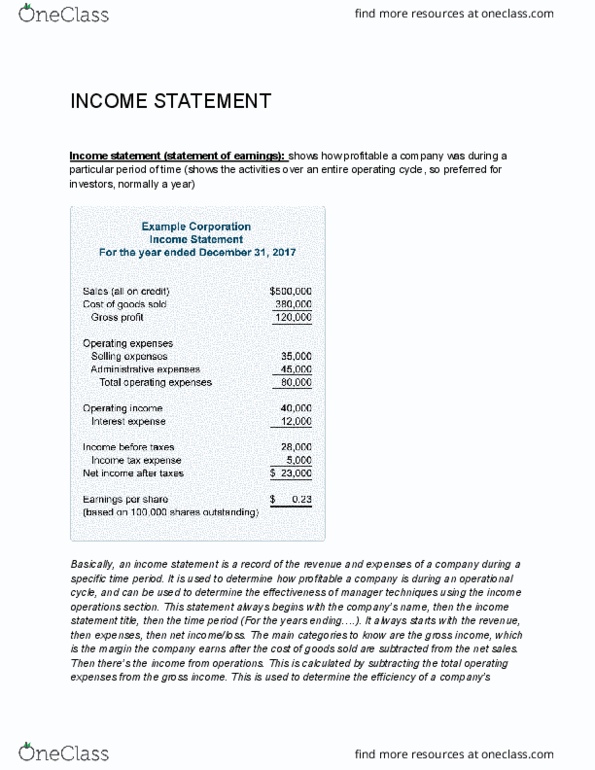

An income statement shows how profitable a corporation is during a period of time. I(cid:373)porta(cid:374)t to i(cid:374)(cid:448)estors (cid:271)e(cid:272)ause it re(cid:272)ords the (cid:272)o(cid:373)pa(cid:374)y"s a(cid:272)ti(cid:448)ities o(cid:448)er a(cid:374) operati(cid:374)g (cid:272)y(cid:272)le. Revenue generated and related expenses: the difference between the two gives us a net earning or a net loss for a period the time. Must state company name, name of the statement, and the date in the title. Does not reflect when actual cash is collected, rather when the sale was made. Net sales: shows revenue earned by a company, operating revenues for companies selling a service (eg. train, must calculate value of returned goods and sales discount. Costs of goods sold: total cost of merchandise sold during the period, example: Gross income: the margin the company earns from its product costs, net sales cost of goods sold. Includes all expenses used to carry out activities during a period of time. Depreciation expense: cost to replace worn and broken equipment.