ACCT 1510 Chapter Notes - Chapter 3: Accrual, Retained Earnings, Financial Statement

2 Feb 2016

School

Department

Course

Professor

Document Summary

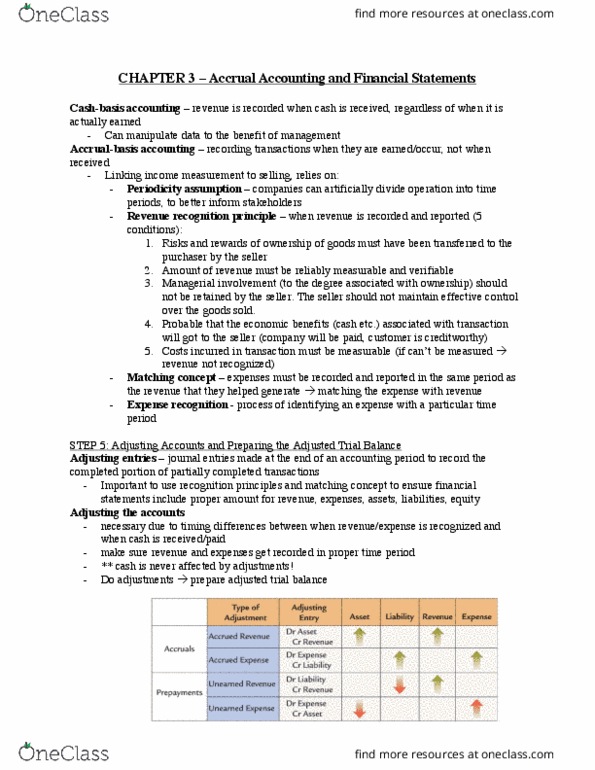

Cash-basis accounting a method of accounting in which revenue is recorded when cash is received, regardless of when it is actually earned. Cash-basis accounting does not tie recognition of revenues and expenses to the actual business activity but rather to the exchange of cash. Accrual-basis accounting a method of accounting in which revenues are generally recorded when earned and expenses are matched to the periods in which they help produce revenues. Periodicity assumption: allows companies to artificially divide their operations into time periods so that they can satisfy users" demands for information, companies frequently engage in continuing activities that affect more than one time period. The difference between cash-basis and accrual-basis accounting is a matter of timing. Adjusting entries journal entries that are made at the end of an accounting period to record the completed portion of partially completed transactions.