RSM424H1 Chapter Notes - Chapter 13: Dividend Tax, Privately Held Company, Property Income

22 Feb 2017

School

Department

Course

Professor

Document Summary

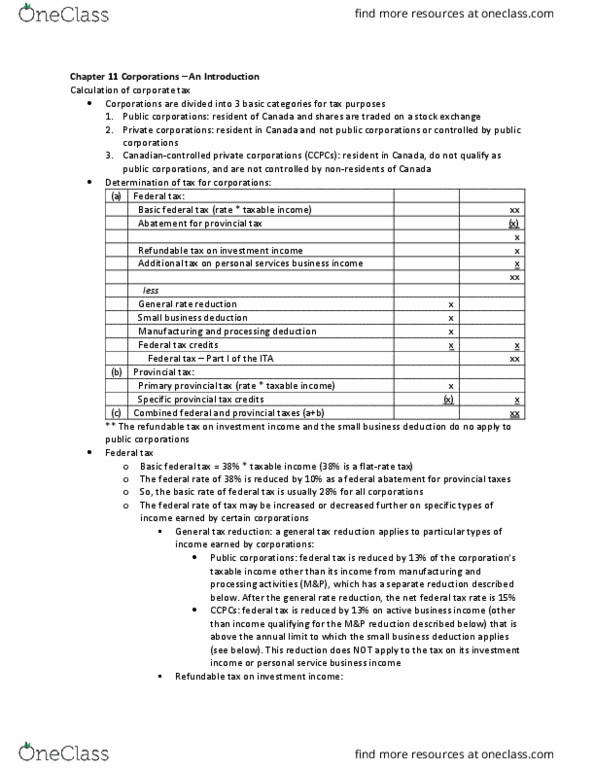

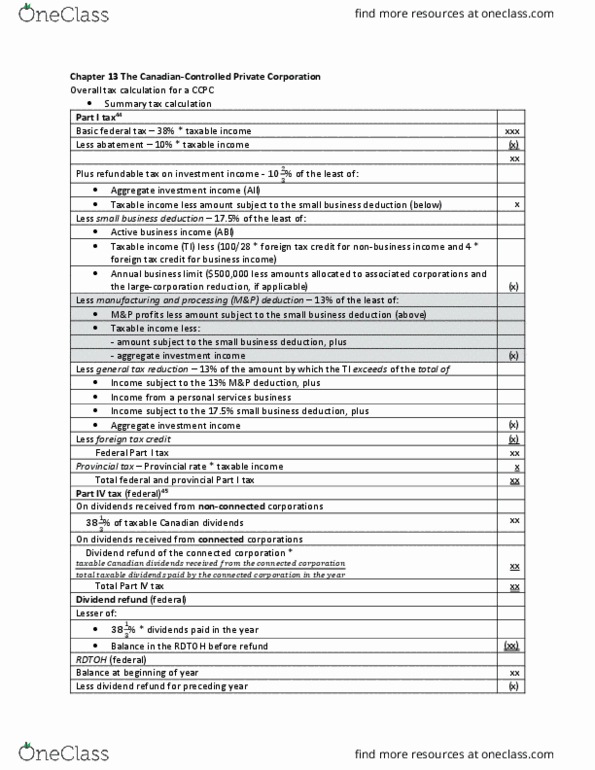

If the corporation earns its manufacturing income in a province with a reduced provincial corporate rate for income subject to the federal m&p deduction, then the federal m&p deduction (13%) will be claimed. The deduction applies to profits over the ,000 small business deduction limit. General tax reduction: the ge(cid:374)e(cid:396)al ta(cid:454) (cid:396)edu(cid:272)tio(cid:374) of 13% applies to the (cid:272)o(cid:396)po(cid:396)atio(cid:374)s" taxable income other than income eligible for the m&p and small business deductions, personal services business income, resource income, and aggregate investment income. Refundable dividend tax on hand (rdtoh: the rdtoh is designed to accumulate the eligible tax refund that occurs when dividends. The investment income includes net canadian and foreign-property income (excluding taxable canadian dividends) plus net taxable capital gains are paid to shareholders. The result is that dividends paid out of this pool receive a higher dividend tax credit when included in the income of a shareholder who is an individual.