RSM332H1 Chapter Notes - Chapter 2: Canada Business Corporations Act, Corporate Law, Cash Flow

Document Summary

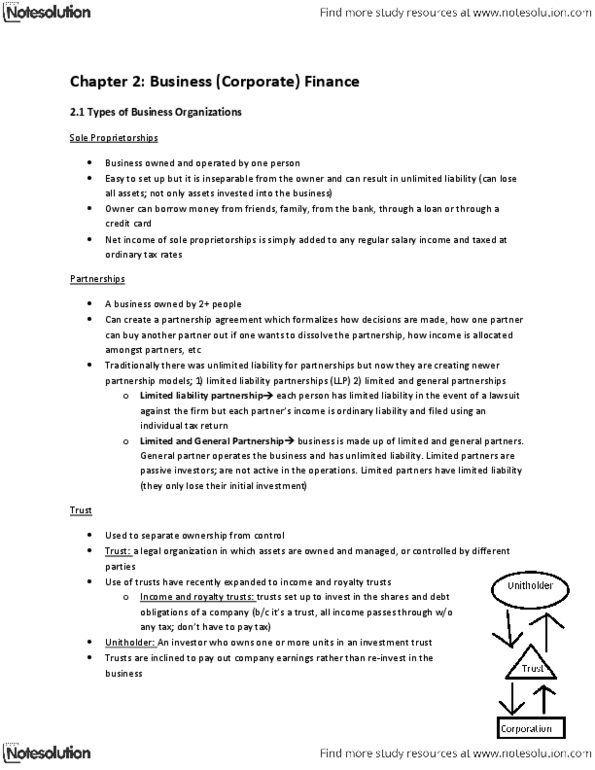

A business owned and operated by one person. Legally inseparable from the person who owns and operates the business. Reports income, both gross and net, on personal income tax returns. Net (cid:271)usi(cid:374)ess i(cid:374)(cid:272)o(cid:373)e is ta(cid:454)ed at the pe(cid:396)so(cid:374)"s (cid:373)a(cid:396)gi(cid:374)al ta(cid:454) rate. Limited to the resources of the individual owning and operating the business and their personal capacity to borrow. Business records must be maintained for reporting to canada revenue agency like any other business. Owners may wish or, depending on the type of the business and the jurisdiction, be required to register with their provincial government. If employing persons, the owner must obtain an employer number, deduct and remit income taxes as well as make employer contributions to the canada pension plan and employment insurance. Little formality, but business records must be maintained. Net income is taxed at the personal marginal tax rate. Financing is limited to the resources of the owner.