RSM219H1 Chapter Notes - Chapter 4: Revenue Recognition, Cash Flow, Standard Accounting Practice

7

RSM219H1 Full Course Notes

Verified Note

7 documents

Document Summary

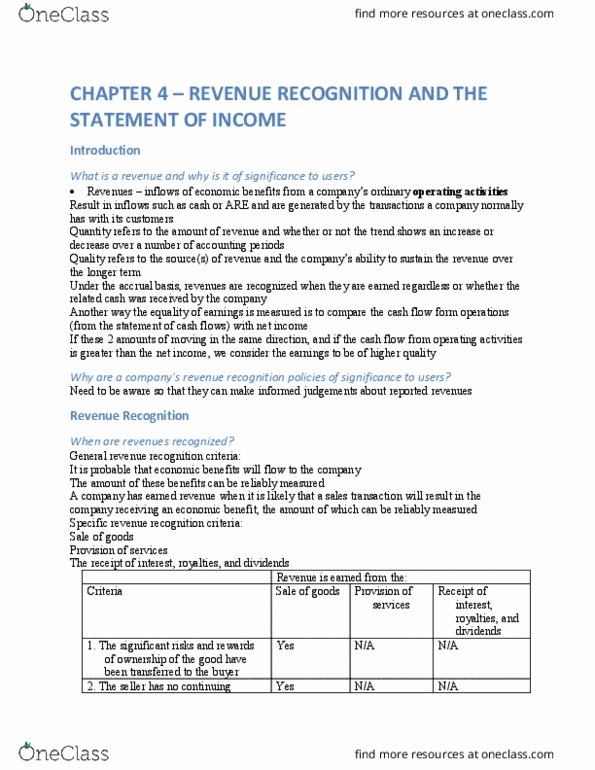

Chapter 4: revenue recognition and the statement of income. Inflow of economic benefits from a company ordinary operating activities. Inflow such as cash or accounts receivable by a transaction of a good or service. Economic benefit: the benefit will end up being cash or ar, the sale and the receipt of cash do not have to occur at the same time. Good = when revenues are higher than expenses. Bad = when expenses are higher than revenues. Assessing revenues, requires two factors: quantity: the amount of revenue, whether or not it increases or decreases over time, quality: sou(cid:396)(cid:272)es of (cid:396)e(cid:448)e(cid:374)ue a(cid:374)d the (cid:272)o(cid:373)pa(cid:374)y"s a(cid:271)ility to sustai(cid:374) the (cid:396)e(cid:448)e(cid:374)ue o(cid:448)e(cid:396) a lo(cid:374)g pe(cid:396)iod of time. Alternative method of measuring the quality of earnings: Comparing the cash flow from operating expenses and net income. Good = cash flow and net income go up together. Bad = (cid:272)ash flo(cid:449) goes do(cid:449)(cid:374) a(cid:374)d (cid:374)et i(cid:374)(cid:272)o(cid:373)e is goi(cid:374)g up, does(cid:374)"t (cid:373)ake se(cid:374)se.