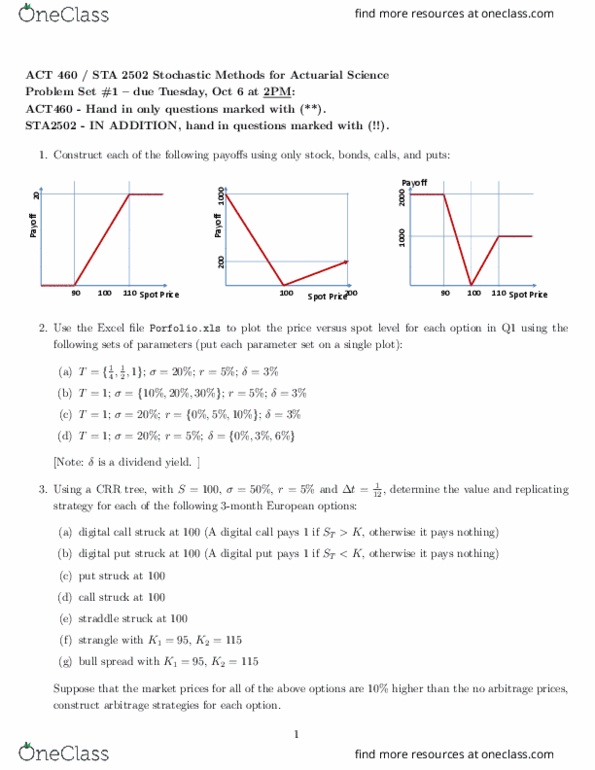

ACT460H1 Chapter Notes - Chapter 3: Bull Spread, Call Option, Actuarial Science

Document Summary

Act 460 / sta 2502 stochastic methods for actuarial science - problem set #3 due tuesday, dec 1 at 2pm. Use the portfolio. xls le to explore the sensitive of prices, deltas and gammas to t , , and r: derive the price, delta and gamma for an asset-or-nothing call option (which pays st if. St > k at maturity t , and pays 0 otherwise) using the black-scholes model. Plot the price, delta and gamma as a function of the spot price with the following parameters: s0 = 1, That is, = st i(st > su ). (c) a call option (maturing at v ) on a forward-start asset-or-nothing option. The embedded forward-start asset-or-nothing option pays the asset at t > v if the asset price at t is above a percentage of the asset price at time u (where v < u < t ).