MGT223H5 Chapter 09: Budgeting Notes

Document Summary

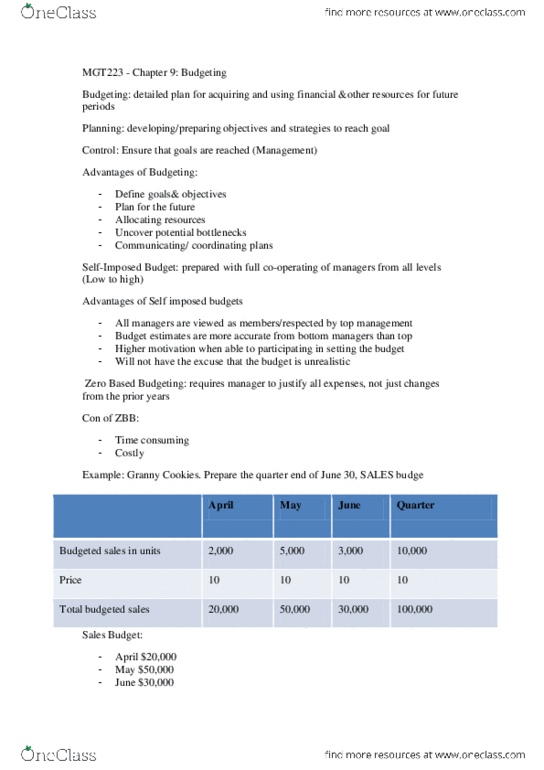

Budget: a detailed quantitative plan for acquiring and using financial and other resources over a specified forthcoming time period. Budgetary control: use of budgets to control an organization"s activity. Planning: involves developing objectives and preparing various budgets to achieve these objectives. Control: involves the steps taken by management that attempt to ensure the objectives are attained. Think about and plan for the future. A budget is prepared with full cooperation and participation of managers at all levels, a participative budget is self-imposed budget. Individuals at all levels of the organization have judgments valued by top management. Budget estimates prepared by front-line managers are often more accurate than prepared by top managers. Eliminates excuses such as a manager claiming the imposed budget to be unrealistic. Zero based budgeting: requires managers to justify all budgeted expenditures, not just changes in the budget from the prior year, very time consuming. Sales budget production budget direct labour budget cash budget.